Discovering a discrepancy in your quarterly payroll tax filings is a stressful experience that can disrupt your accounting workflow and trigger unwanted regulatory scrutiny. Navigating the complex reconciliation process for Social Security and Medicare taxes requires a precise understanding of IRS adjustment mechanisms, particularly during high-stakes audit seasons.

Utilizing standardized templates grants your finance team the exact structure needed to expedite corrections confidently, ensuring you recover overpayments and resolve underpayments without administrative delays. Please note, however, that while these templates streamline the preparation process, they function as administrative aids rather than a substitute for certified CPA review.

This guide highlights essential adjustment templates, including Form 941-X for quarterly corrections and Form 843 for refund claims. Below, we will break down how to deploy these tools effectively, outline step-by-step instructions for calculating variances, and establish best practices for filing timely amendments.

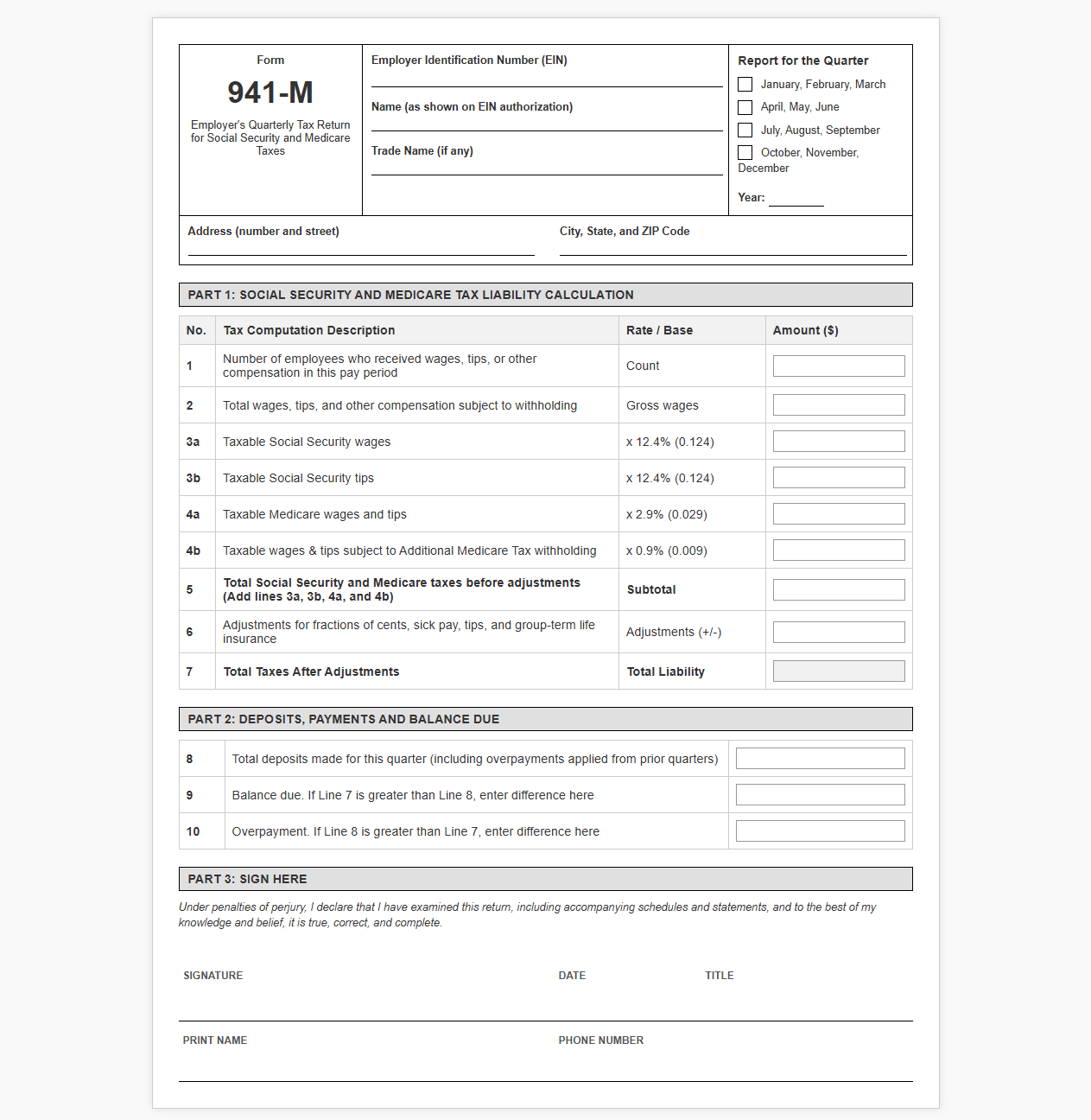

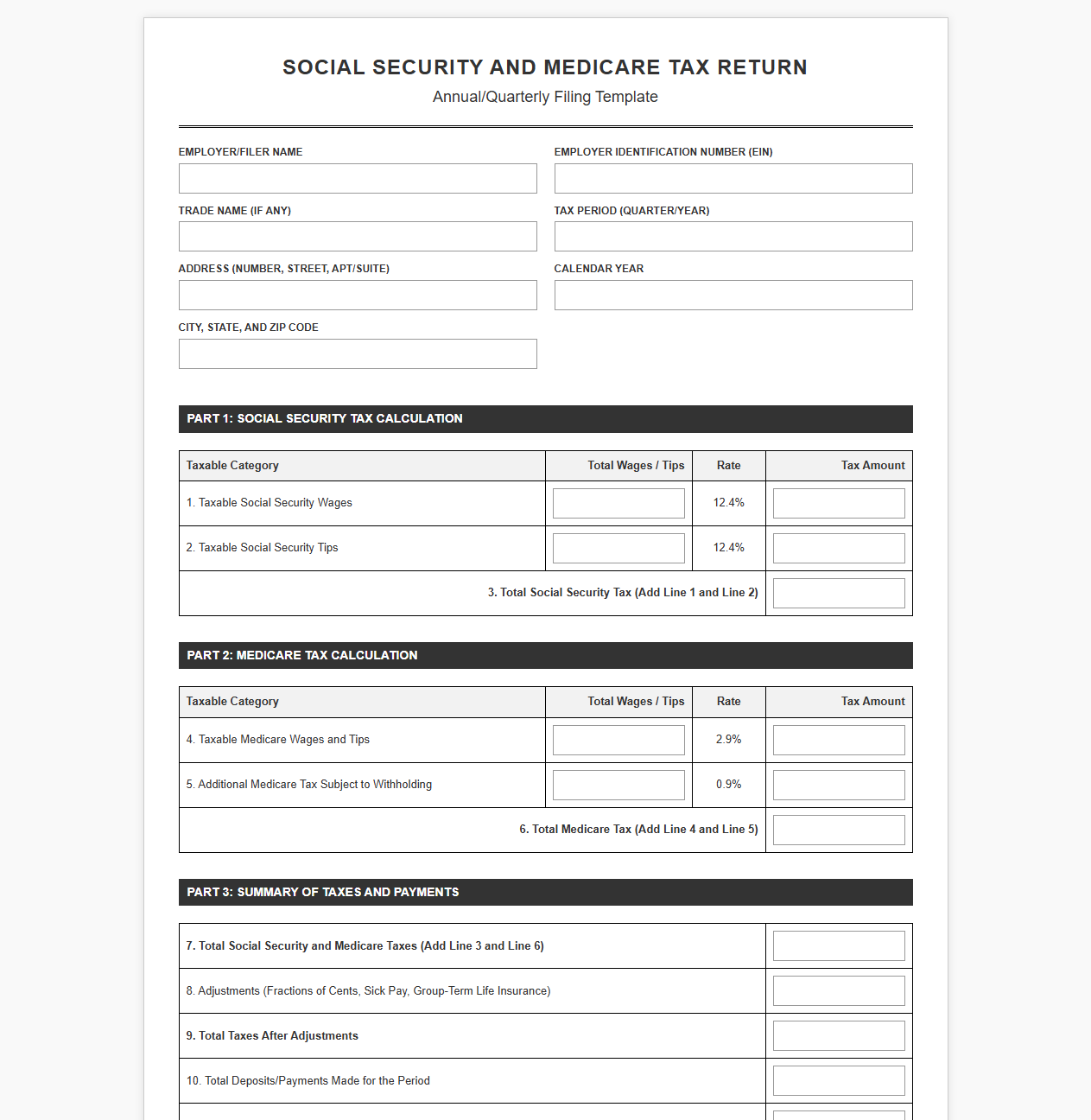

Social Security and Medicare Tax Return Template

Download: .PDF

Download: .PDF

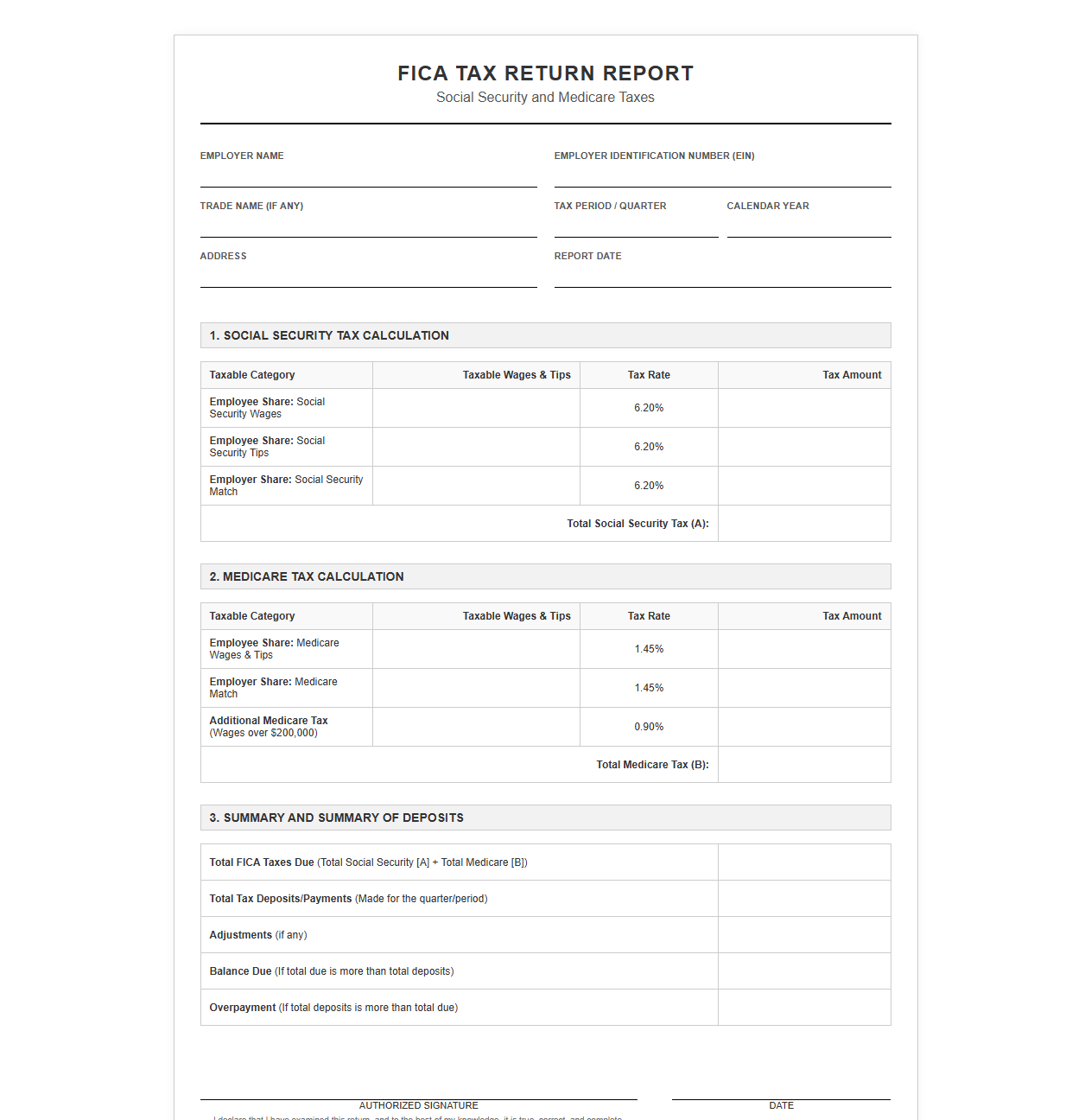

FICA Tax Return Report Template

Download: .PDF

Download: .PDF

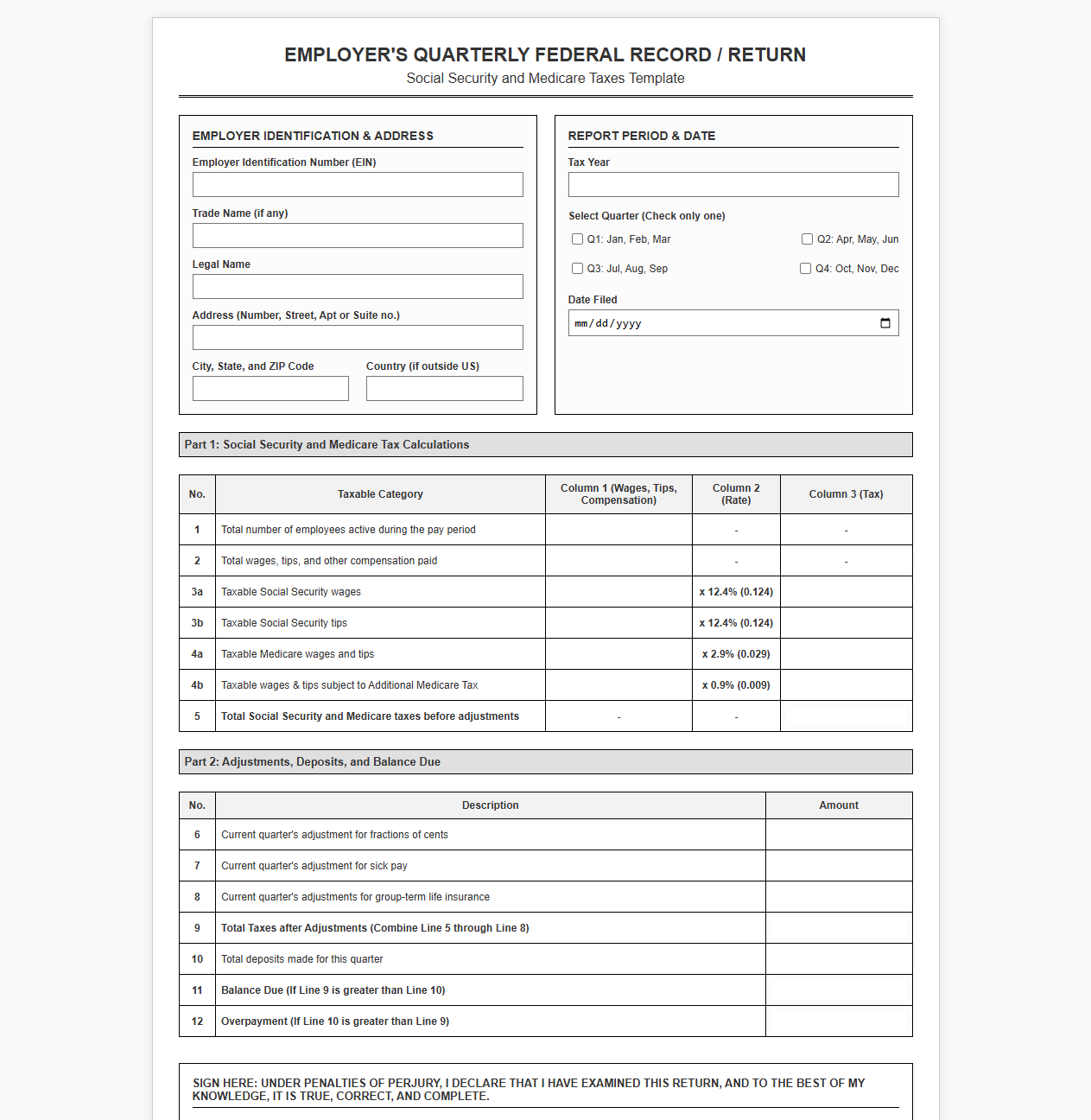

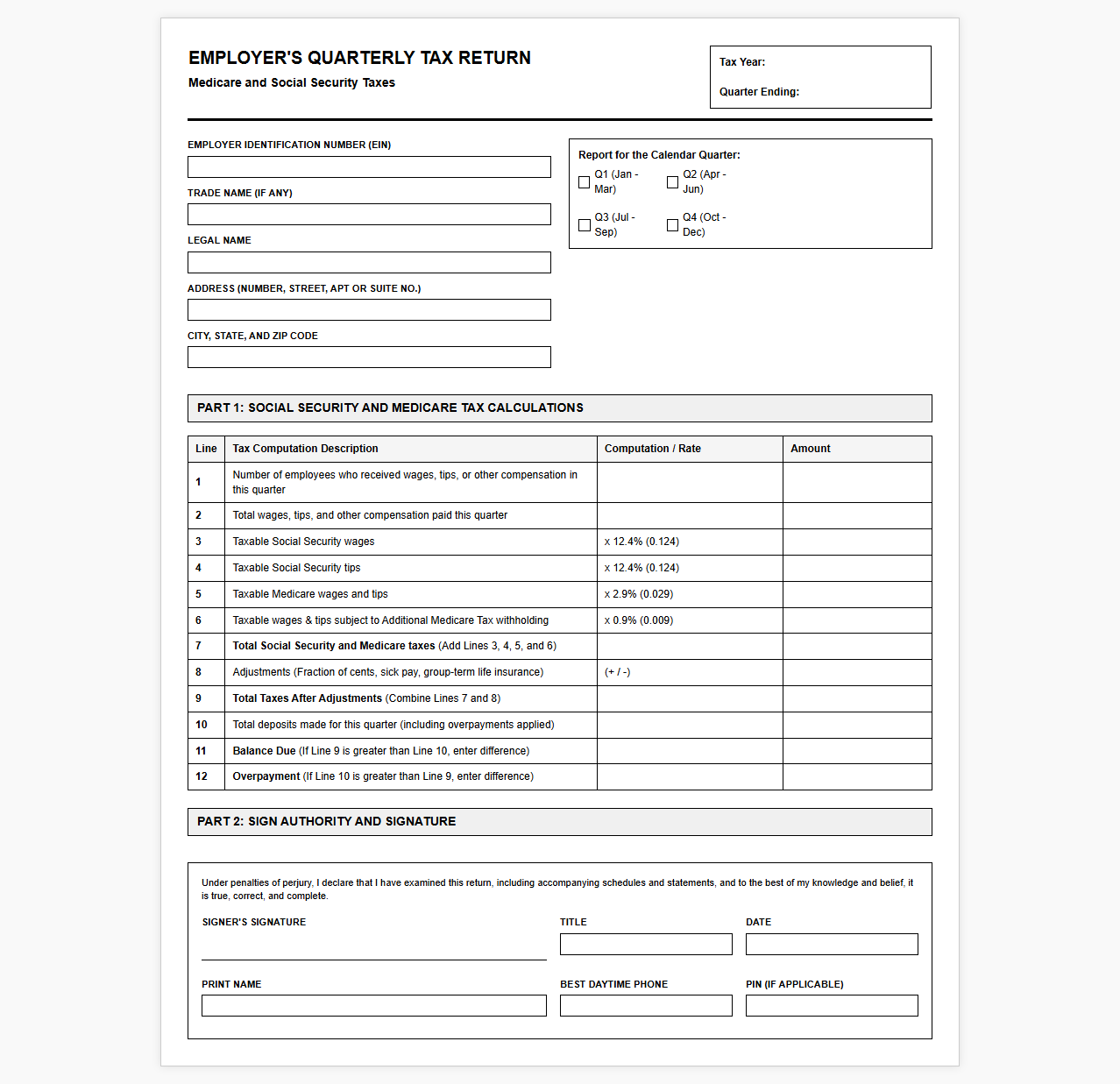

Payroll Tax Return Template for Social Security and Medicare

Download: .PDF

Download: .PDF

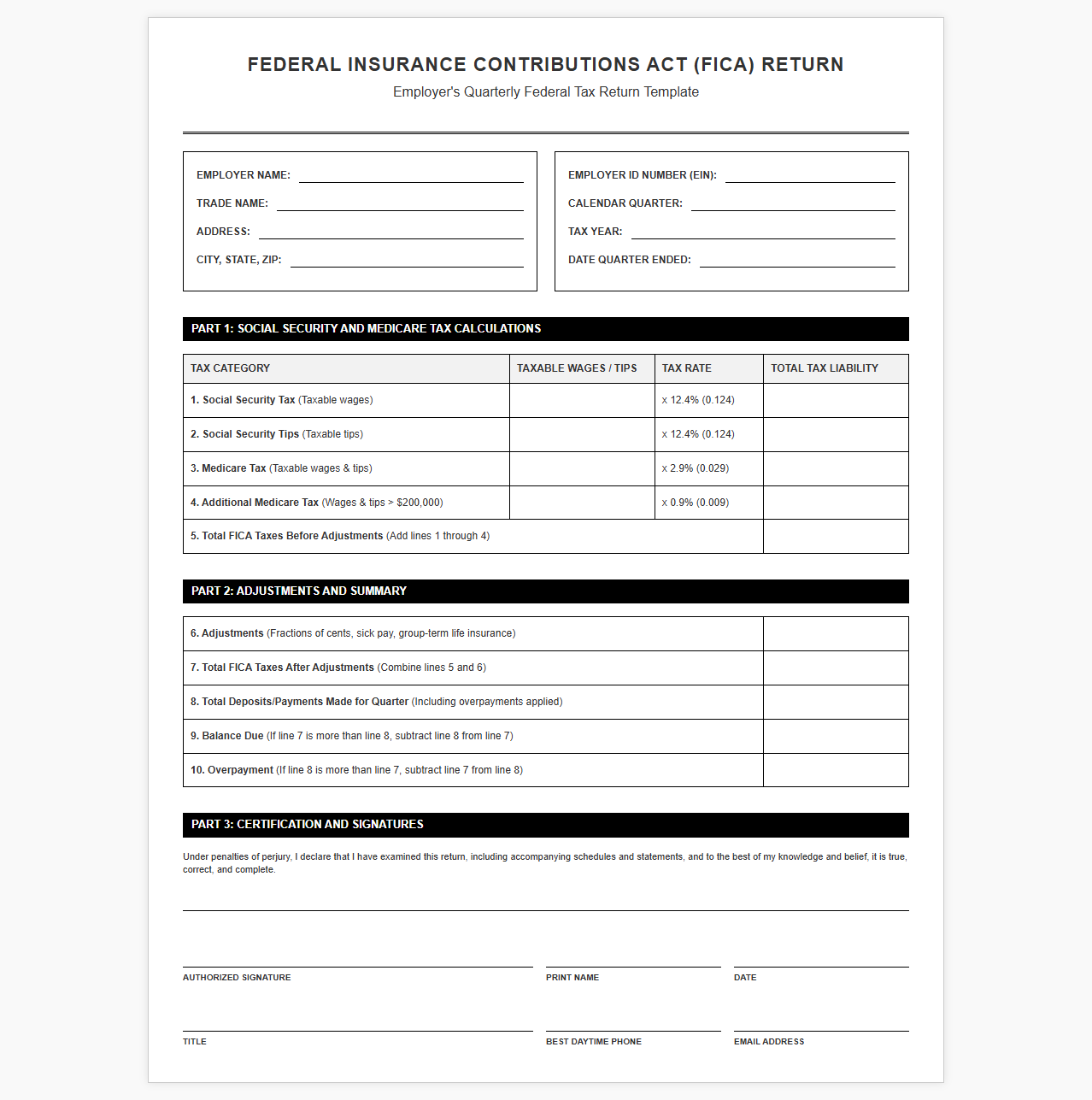

Federal Insurance Contributions Act Return Template

Download: .PDF

Download: .PDF

Social Security and Medicare Tax Filing Template

Download: .PDF

Download: .PDF

Quarterly Social Security and Medicare Tax Return Form

Download: .PDF

Download: .PDF

Employer Medicare and Social Security Tax Return Template

Download: .PDF

Download: .PDF

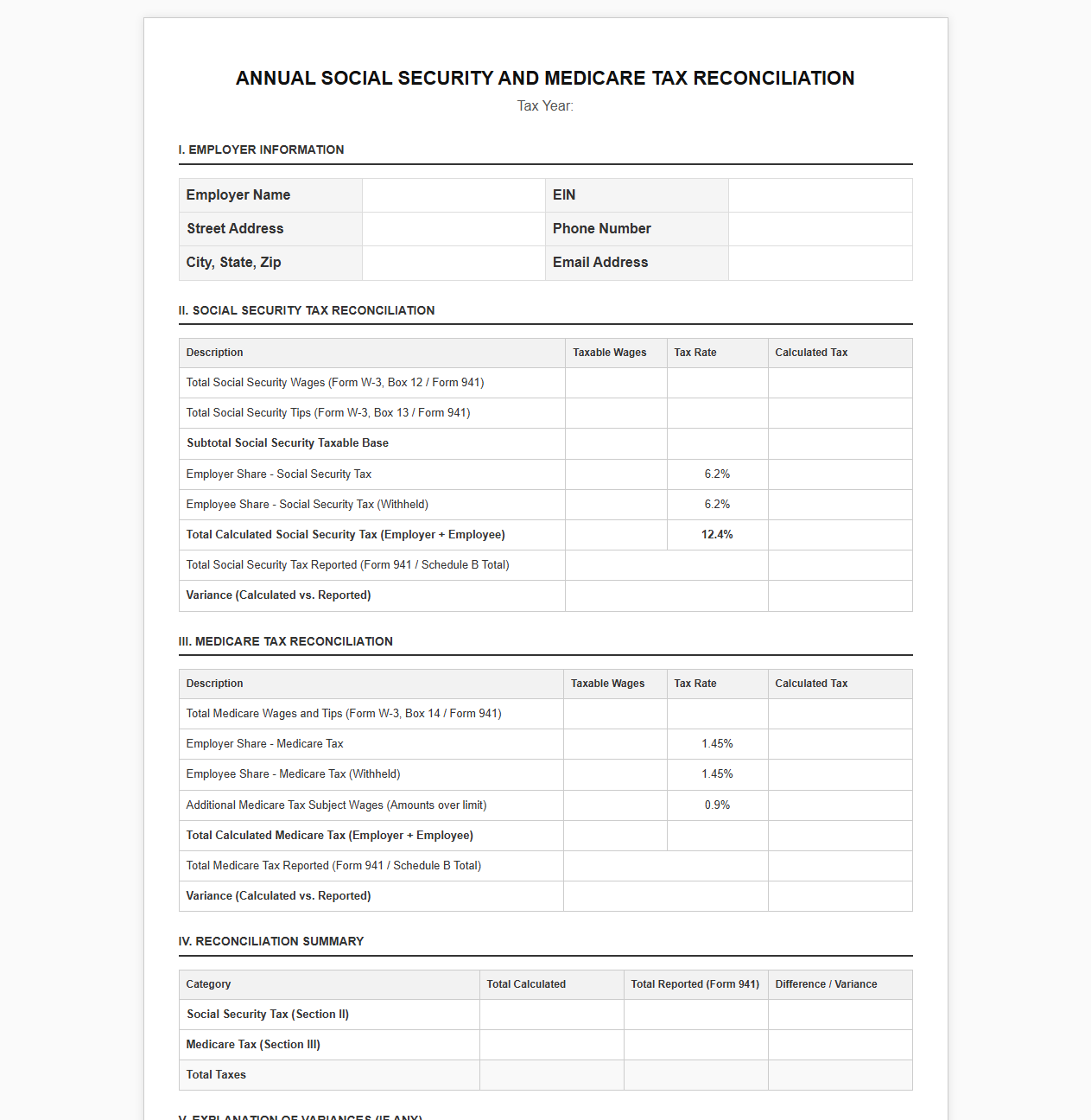

Annual Social Security and Medicare Tax Reconciliation Template

Download: .PDF

Download: .PDF

Understanding Social Security and Medicare Tax Discrepancies

Managing payroll involves balancing complex tax regulations, making Federal Insurance Contributions Act (FICA) withholding errors a frequent challenge for businesses of all sizes. Discrepancies in Social Security and Medicare taxes typically surface when the calculated tax liability does not align with the actual amounts withheld from employee paychecks or reported on federal tax returns. Because FICA taxes directly fund federal social insurance programs, even minor rounding errors or miscalculations can compound over multiple pay cycles, resulting in significant reporting imbalances.

Resolving these discrepancies swiftly is vital for maintaining business compliance and avoiding costly consequences. Failing to identify and correct payroll variances in a timely manner can trigger audits, lead to severe IRS penalties, and generate unexpected financial liabilities for the employer. Proactive detection ensures that both the employer and employee contributions are perfectly aligned, preserving the integrity of individual earnings records with the Social Security Administration.

Common Triggers of Payroll Underpayments and Overpayments

- System Configuration Errors: Misconfigured payroll software parameters, incorrect tax tables, or failing to update tax rates at the start of the fiscal year.

- Pre-Tax Deduction Miscalculations: Applying pre-tax deductions to benefits that are not exempt from FICA, such as certain retirement contributions, or failing to exempt qualified Section 125 cafeteria plans.

- Employee Status Changes: Misclassifying workers between independent contractors and statutory employees, or delaying system updates when an employee transitions from part-time to full-time status.

- Social Security Wage Base Overshoots: Failing to halt the 6.2% Social Security withholding once an employee's year-to-date earnings exceed the annual statutory wage limit.

- Additional Medicare Tax Oversight: Omitting the mandatory 0.9% Additional Medicare Tax withholding once an employee's compensation crosses the threshold based on their filing status.

Key Tax Correction Templates: Form 941-X and Form 944-X

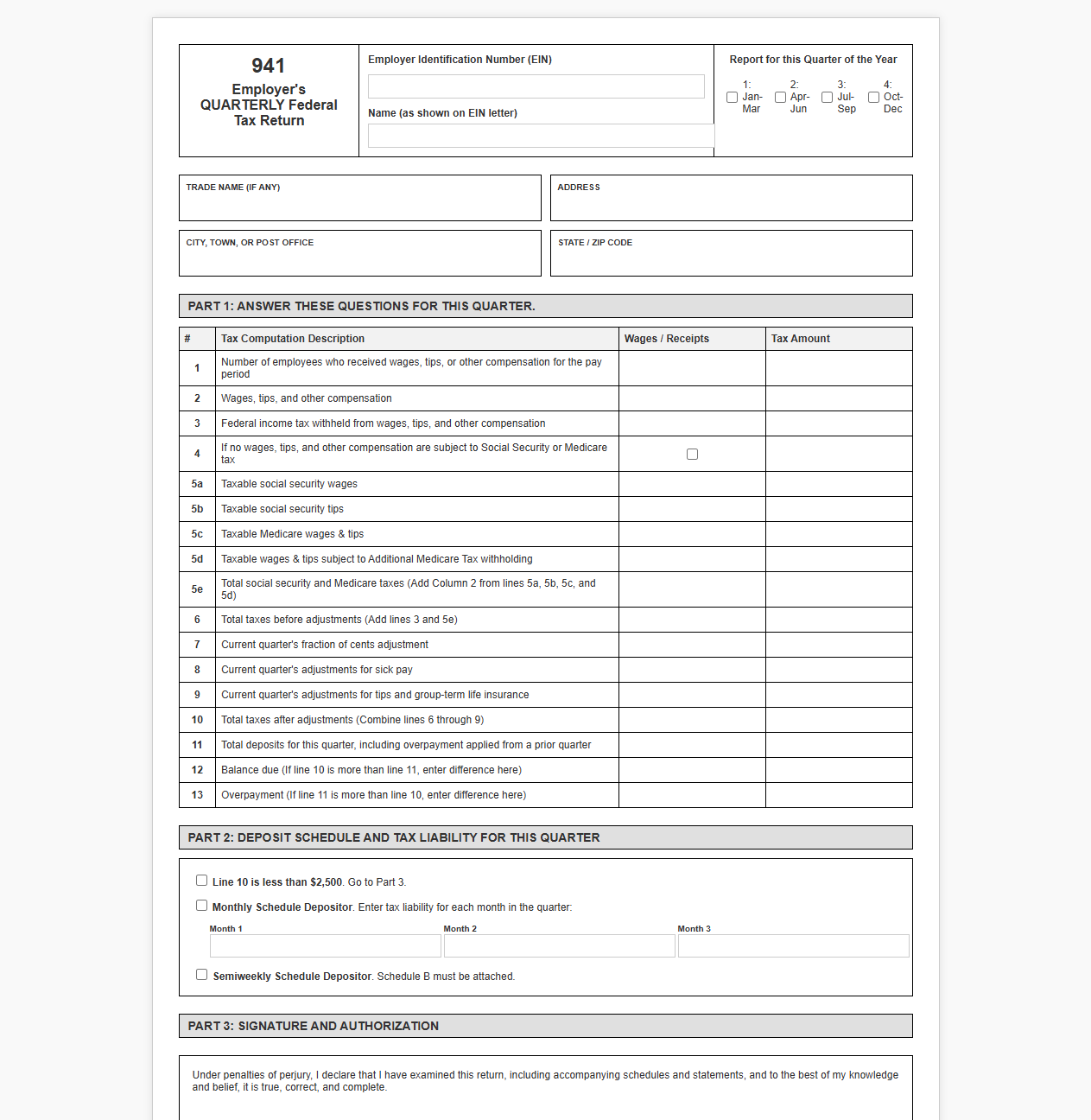

To resolve FICA withholding discrepancies, the IRS requires employers to file specific adjustive tax returns rather than simply altering future payroll cycles. The primary mechanism for correcting quarterly filings is Form 941-X (Adjusted Employer's QUARTERLY Federal Tax Return or Claim for Refund). This form is utilized to rectify errors originally reported on Form 941, allowing employers to correct overreported or underreported Social Security tax, Medicare tax, and Additional Medicare Tax for specific quarters.

Conversely, small employers who file their taxes annually rather than quarterly must use Form 944-X (Adjusted Employer's ANNUAL Federal Tax Return or Claim for Refund). This form corresponds directly to corrections for Form 944. Selecting the correct template depends entirely on your business's original filing frequency; using the wrong adjustment template can delay processing times and complicate your account status with the IRS.

Step-by-Step Guide to Reconciling FICA Variances

- Identify the discrepancy by comparing your general ledger payroll reports against your filed quarterly or annual tax returns.

- Calculate the exact variance for both the employer and employee portions of Social Security and Medicare taxes.

- Determine whether the error resulted in an overpayment (entitling you to a refund or adjustment) or an underpayment (requiring an additional tax payment).

- Select the appropriate adjustment template, ensuring you use the correct form version corresponding to the calendar year being corrected.

- Complete the specific lines on the adjustment form, inputting the corrected values, the originally reported values, and the calculated difference.

- Write a detailed explanation of the error on the designated section of the correction form, outlining how the mistake occurred and how it was discovered.

- File the adjustment form independently of your regular tax filings and securely archive all supporting worksheets, payroll registers, and amended returns for at least four years.

Navigating Penalties, Interest, and Refund Claims

When correcting FICA discrepancies, timing is everything. Under the rules of the Internal Revenue Code, employers can make interest-free adjustments for underreported taxes if they file the correction form and pay the tax due by the due date of the return for the period in which the error was discovered. Filing the adjustment before receiving an official IRS notice of underpayment is essential to avoiding costly failure-to-pay penalties and accrued interest charges.

For overreported FICA taxes, employers have two primary paths: the adjustment process or the claim process. The adjustment process applies the overpayment as a credit toward your next tax return, whereas the claim process requests a direct refund of the overpaid taxes. Employers must secure written consent from employees, or make a reasonable effort to refund the employee's share of FICA, before filing a claim for the employee's portion of the overwithheld tax.

Establishing Proactive Payroll Reconciliation Audits

Rather than waiting for year-end reporting to uncover discrepancies, businesses should adopt routine internal auditing practices. Conducting monthly or quarterly reconciliations allows payroll teams to compare internal payroll registers against bank statements and preliminary tax liabilities. This frequency ensures that errors are corrected within the same tax quarter, avoiding the need to file complex federal adjustment forms altogether.

"Continuous monitoring of payroll registers against statutory limits is the single most effective defense against FICA withholding compliance failures."

During these internal audits, verify that payroll software configurations are updated to match annual regulatory changes, including adjustments to the Social Security wage cap and Medicare thresholds. Ensuring a separation of duties between the payroll entry team and the reconciliation team adds another layer of security, minimizing the risk of systemic errors going unnoticed.

The Ultimate FICA Adjustment Compliance Checklist

- Verify that the correction form (Form 941-X or Form 944-X) matches the exact tax year and quarter of the error.

- Confirm that the Social Security wage base limit has not been exceeded for any individual employee adjustment.

- Ensure the Additional Medicare Tax (0.9%) is calculated only on wages exceeding the individual threshold.

- Obtain signed employee consent forms for any overwithheld FICA tax claims prior to submitting a refund request.

- Attach a clear, concise written narrative explaining the cause of the variance on the adjustment form.

- Cross-reference all adjusted calculations to confirm the math is accurate before signing the return.

- Archive copies of the adjustment forms, employee consents, and payroll ledgers in a secure compliance file.

Leave a comment