For financial controllers and billing managers, reconciling unbilled revenue at month-end is a notoriously tedious process that frequently leads to reporting discrepancies and audit anxiety. Before investing in complex automated software, organizations must first establish a solid baseline by standardizing their underlying manual accounting documentation.

Mastering these structured accrued income statement formats grants finance teams absolute visibility into unrecognized earnings, ensuring seamless compliance with ASC 606 standards. However, a key stipulation for success is that these frameworks must be meticulously aligned with your specific contract terms, rather than treated as one-size-fits-all templates.

Utilizing concrete formats, such as structured work-in-progress (WIP) ledger templates or milestone-based billing schedules, provides immediate proof of performance delivery. In this guide, we will examine the essential document formats required to streamline your unbilled revenue tracking, mitigate compliance risks, and accelerate your monthly close cycle.

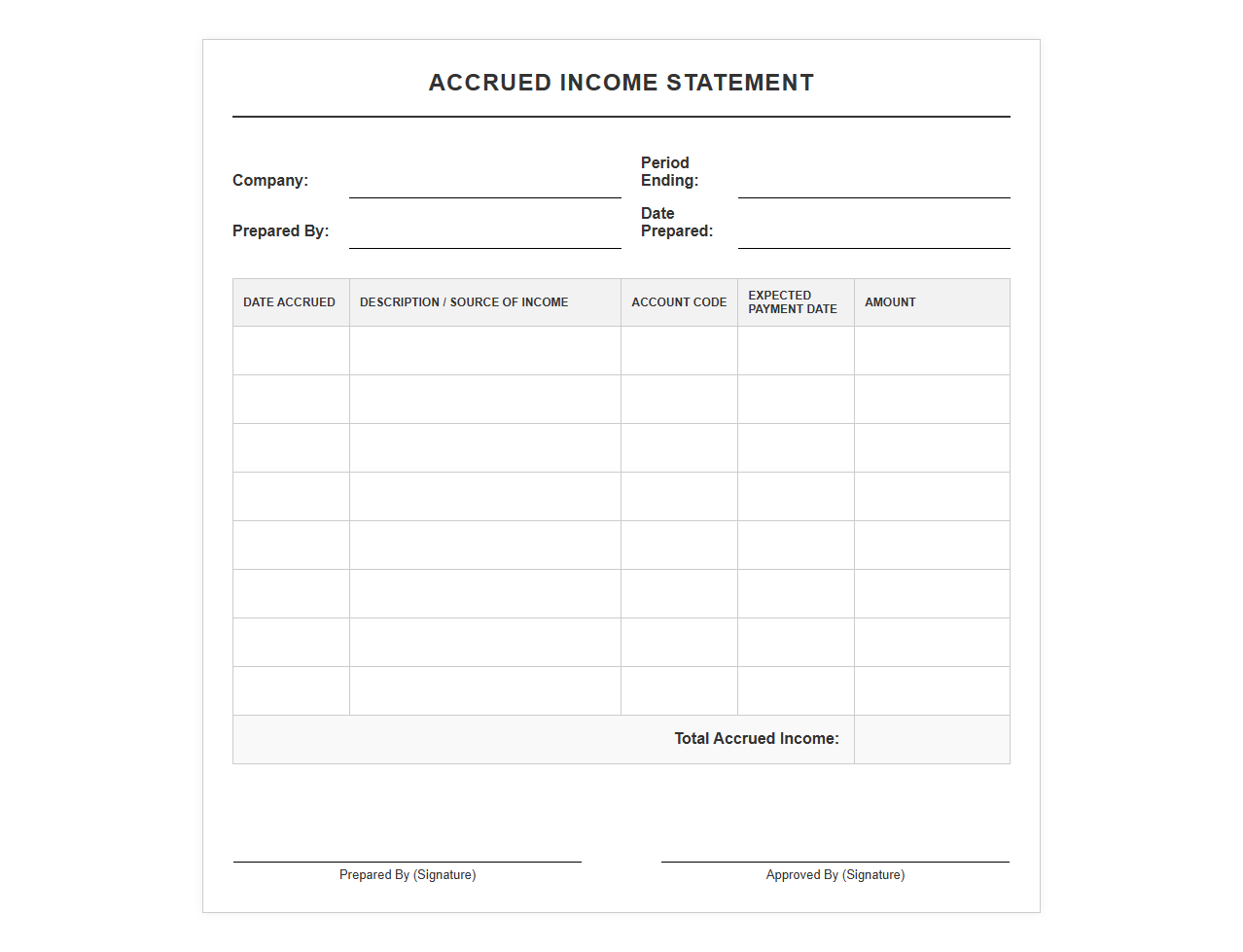

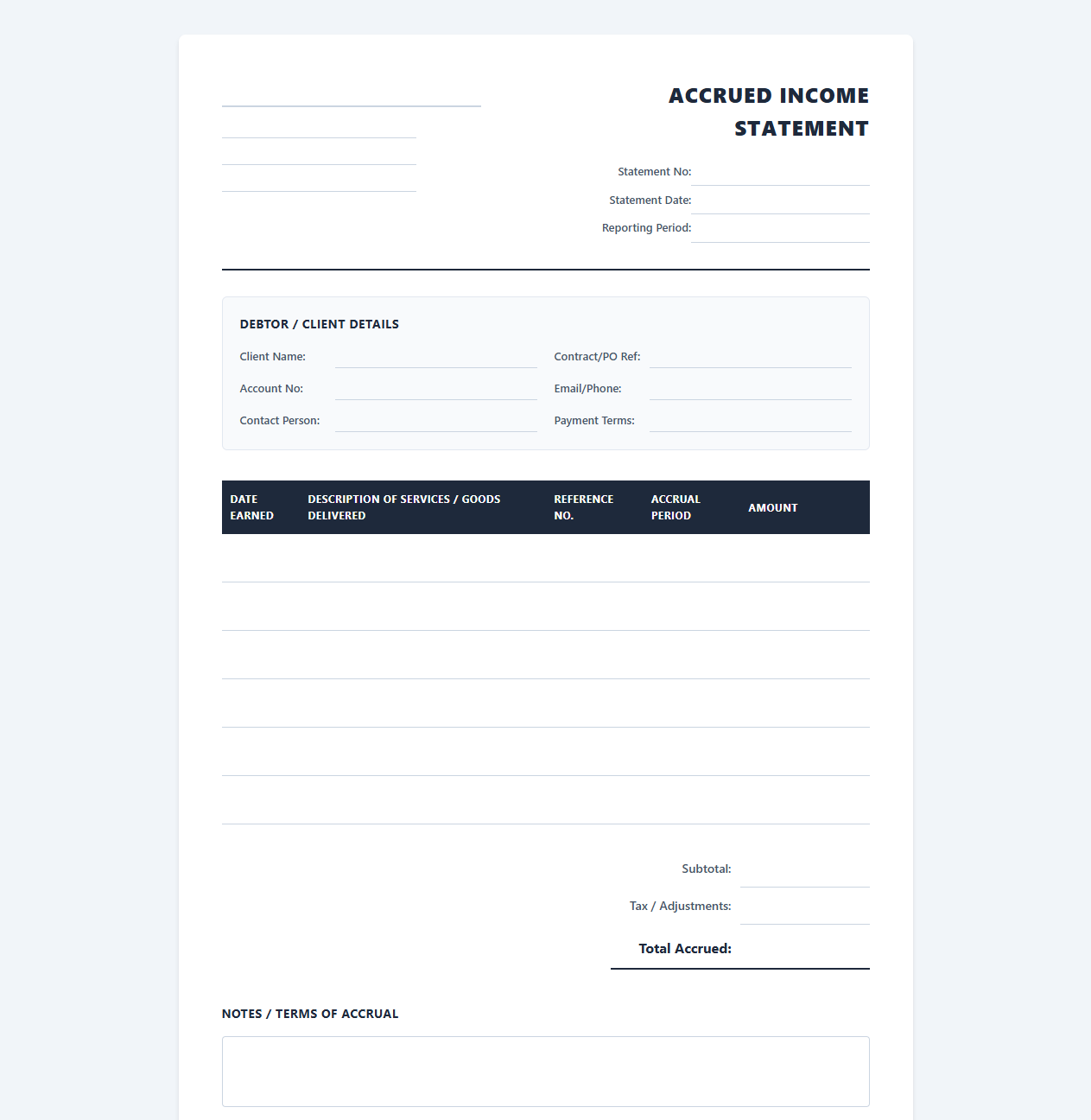

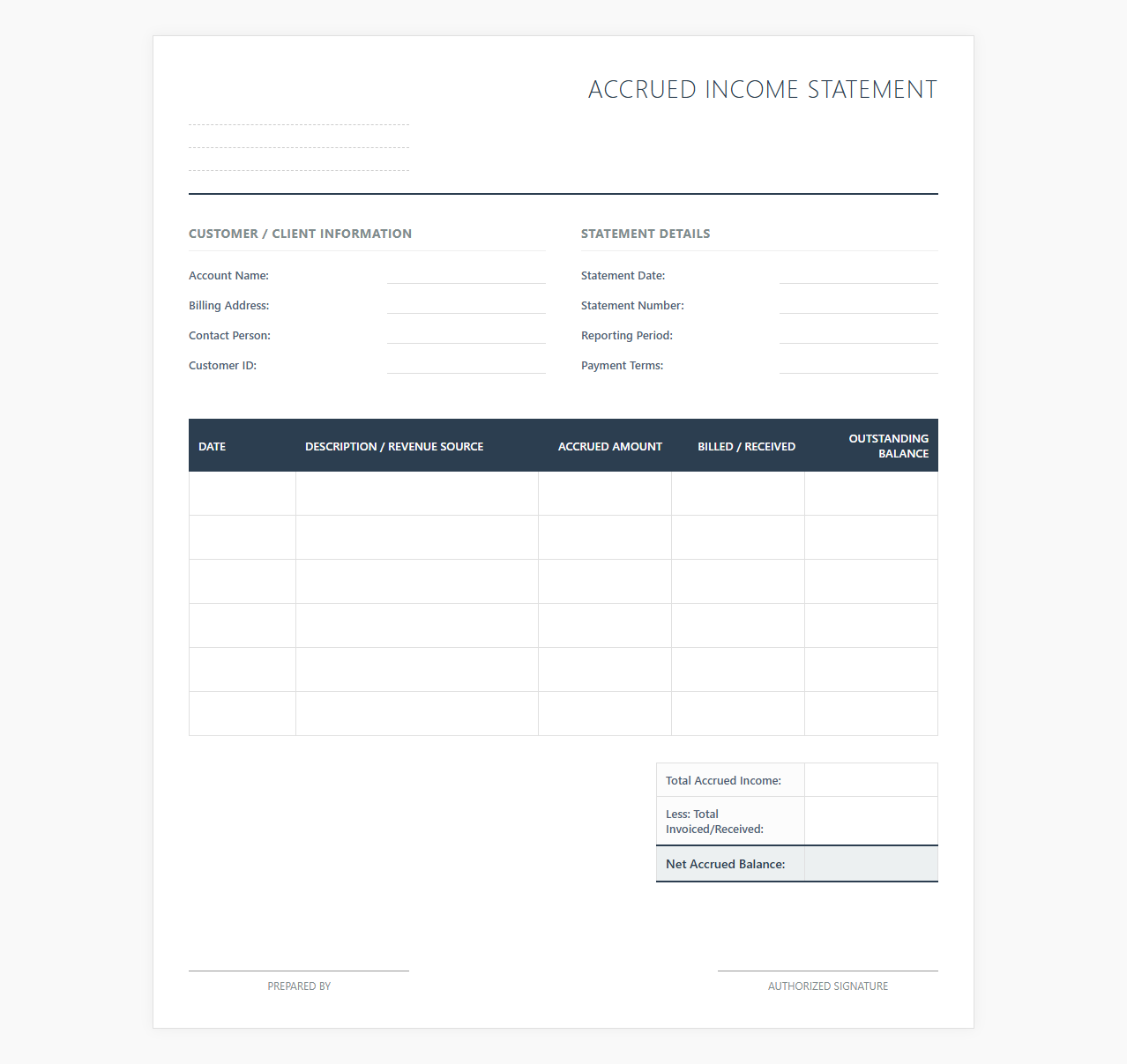

Accrued Income Statement Template

Download: .PDF

Download: .PDF

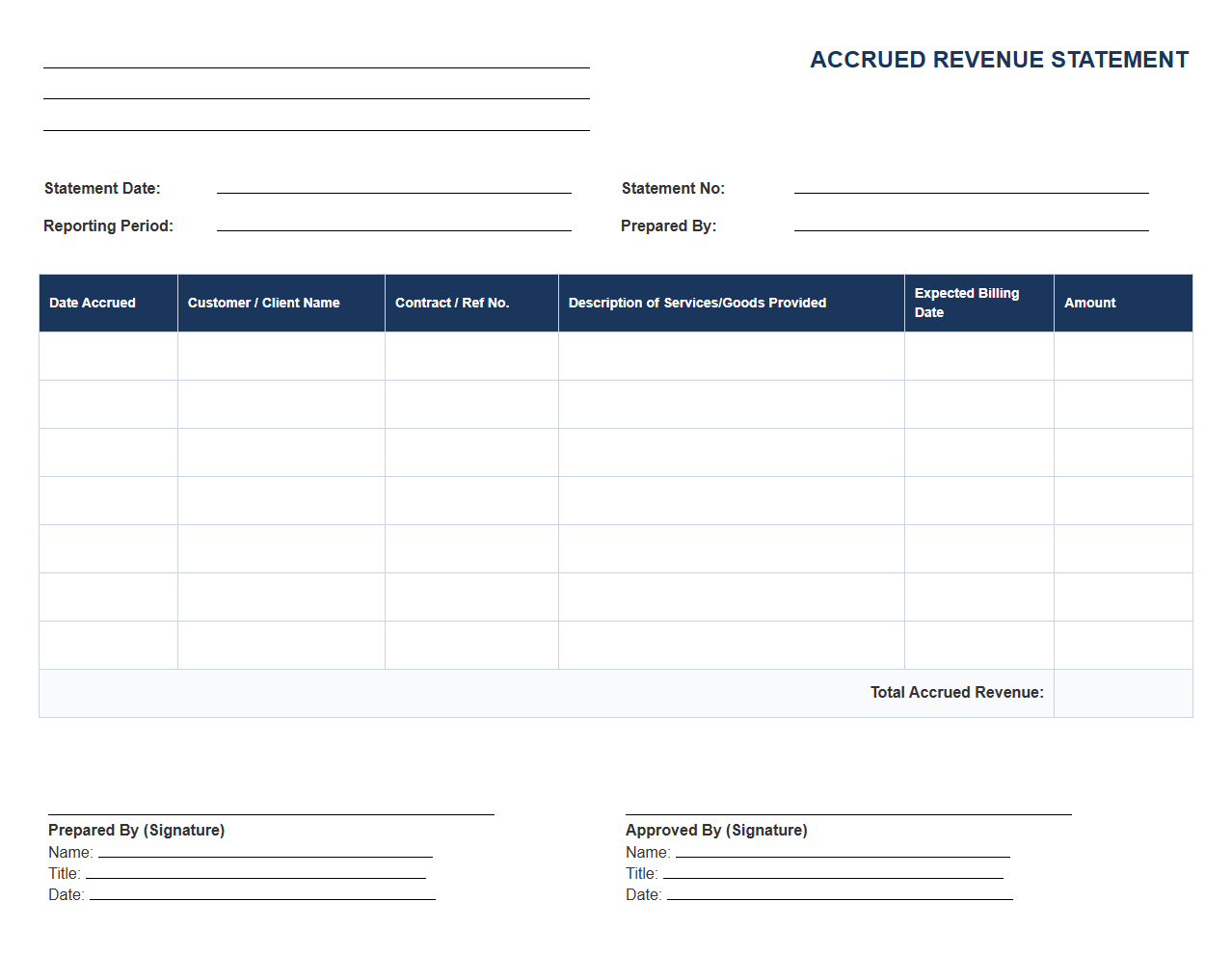

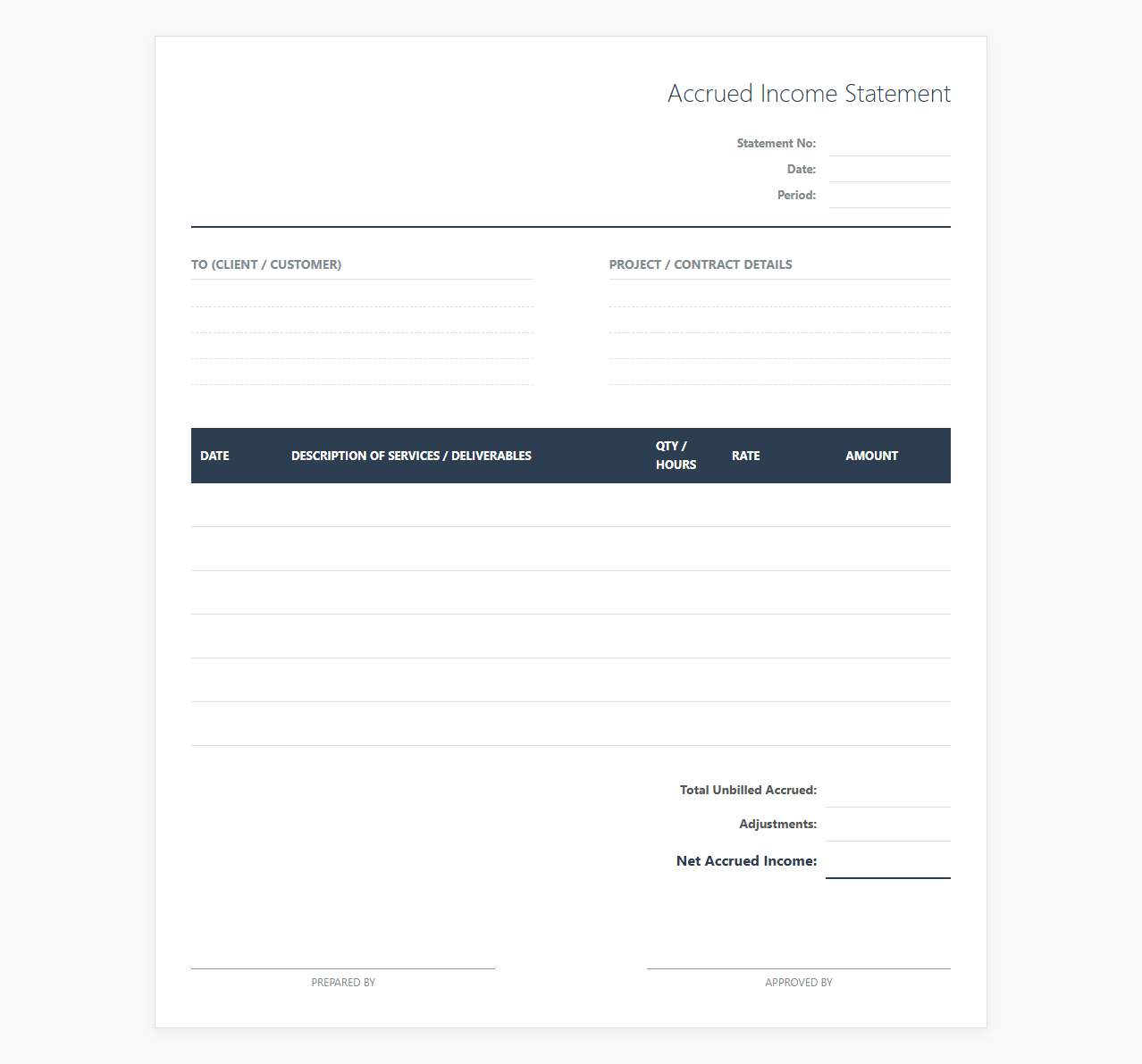

Accrued Revenue Statement Format

Download: .PDF

Download: .PDF

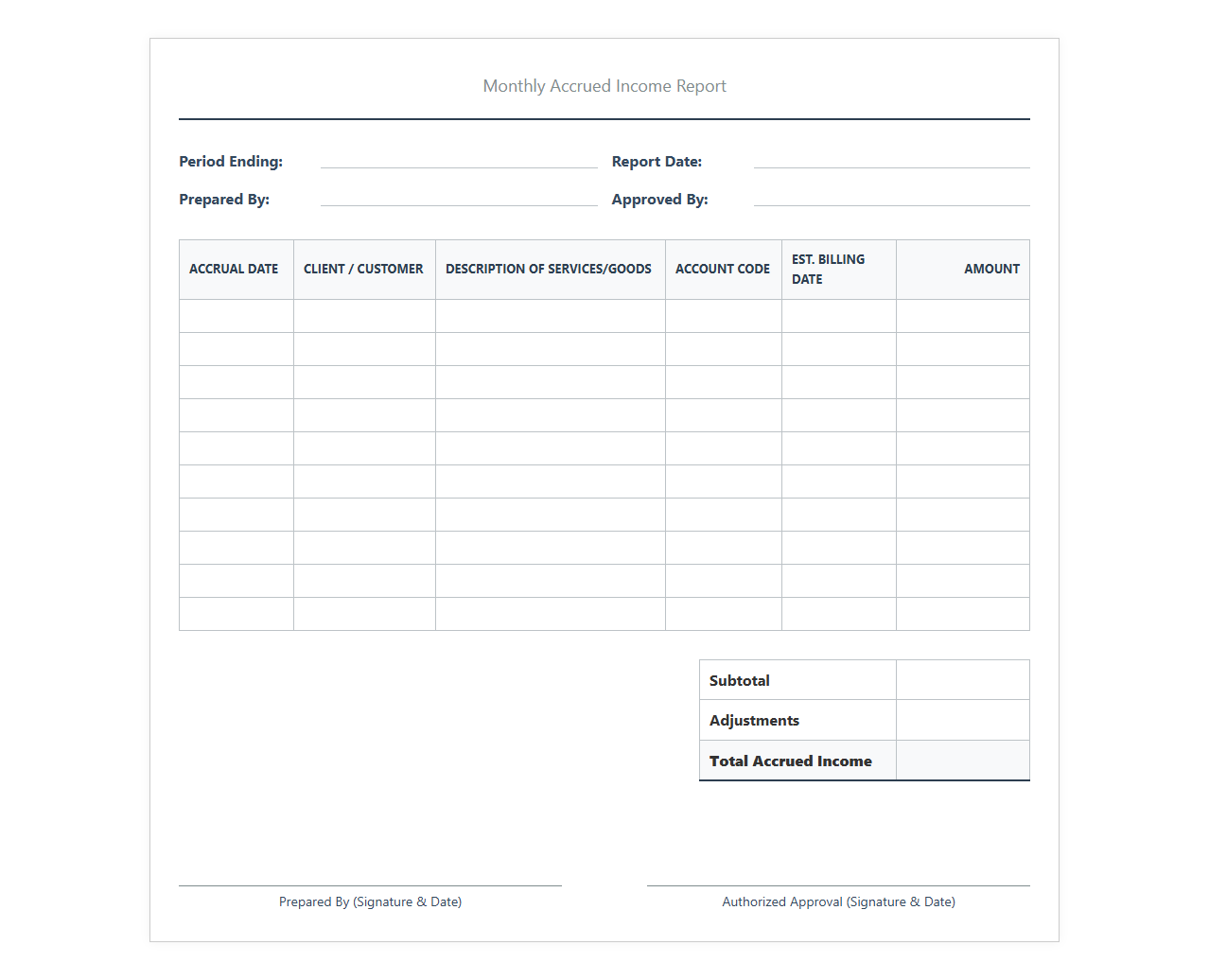

Monthly Accrued Income Report Template

Download: .PDF

Download: .PDF

Outstanding Earned Revenue Statement Template

Download: .PDF

Download: .PDF

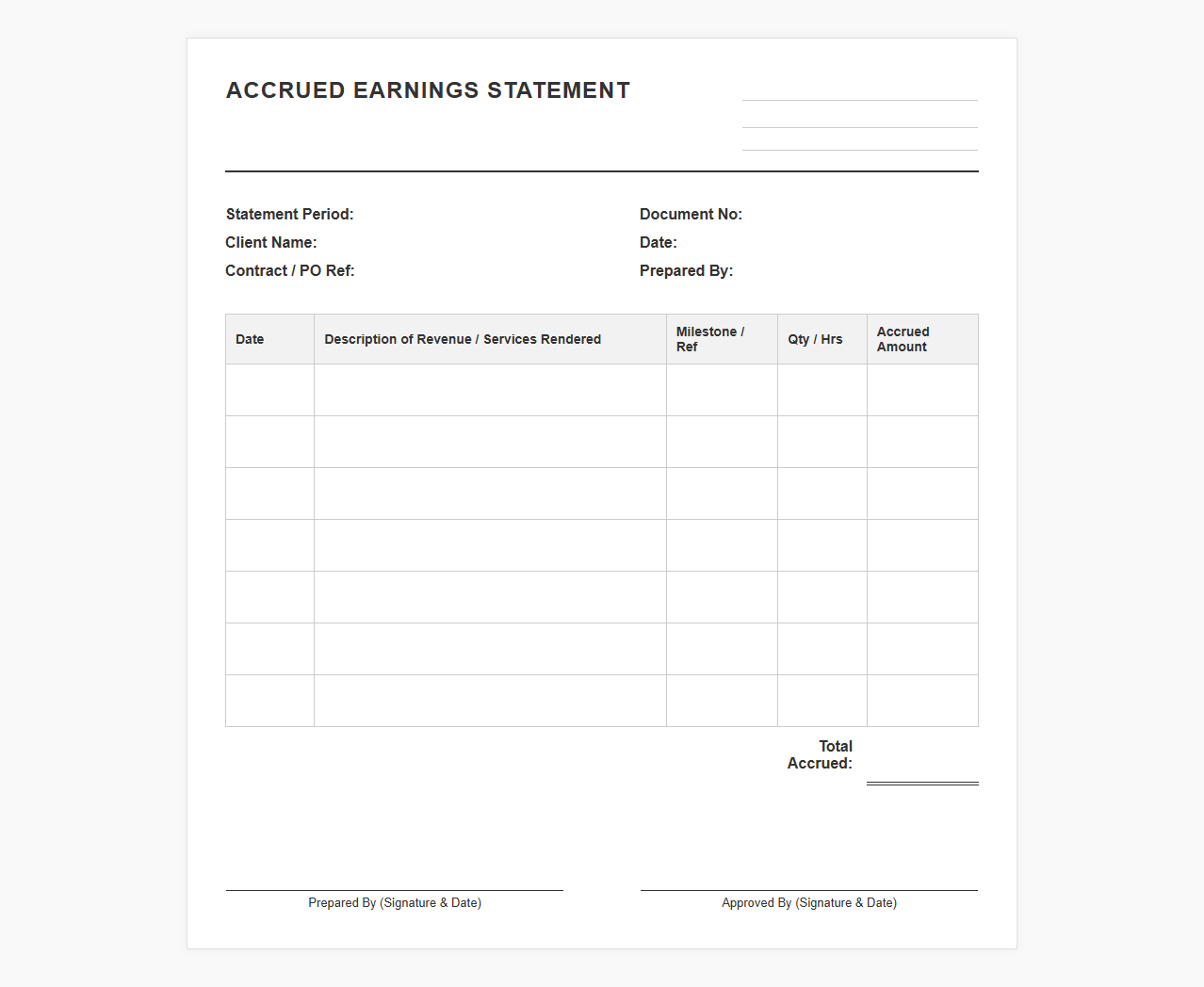

Accrued Earnings Statement Sheet

Download: .PDF

Download: .PDF

Unbilled Revenue Statement Template

Download: .PDF

Download: .PDF

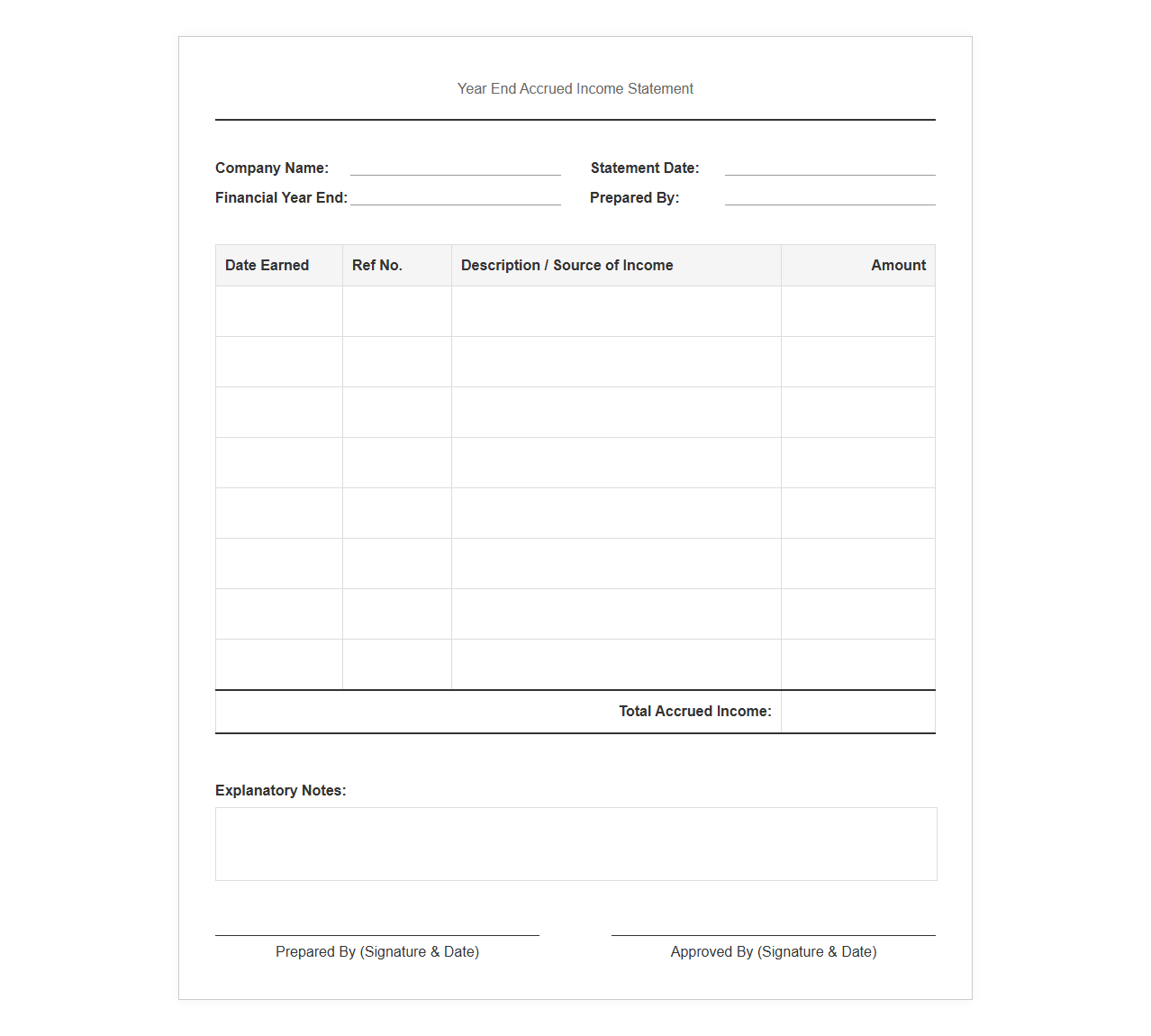

Year End Accrued Income Statement

Download: .PDF

Download: .PDF

Accrued Income Ledger Statement Template

Download: .PDF

Download: .PDF

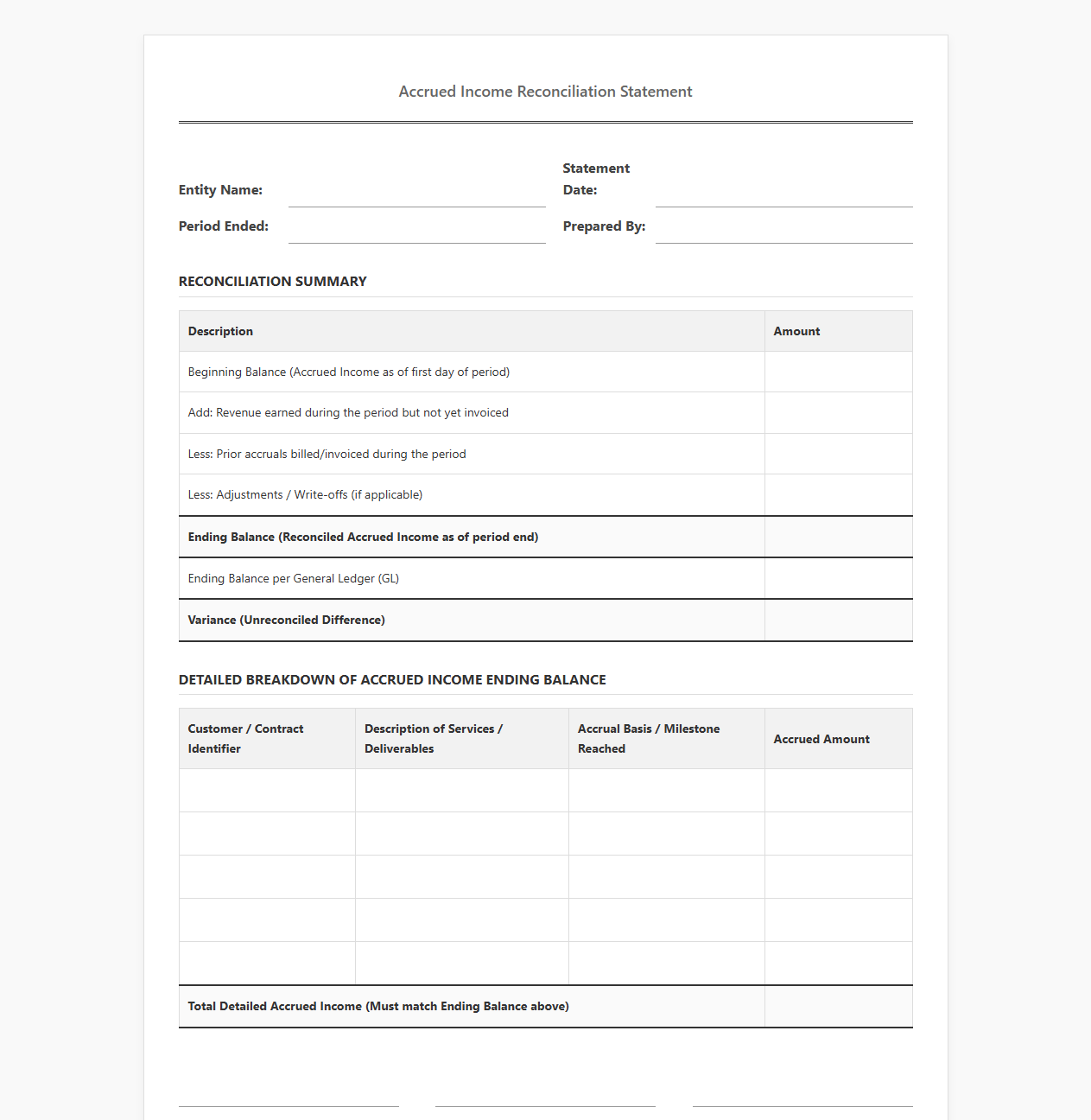

Accrued Income Reconciliation Statement

Download: .PDF

Download: .PDF

The Challenge of Tracking Unbilled Revenue

Many businesses struggle with tracking unbilled revenue due to the disconnect between project delivery and billing cycles. When services are performed or products are delivered before an invoice is generated, finance teams must manually track these earnings to ensure accurate reporting. Without a unified system, companies frequently face timing mismatches and data silos.

The financial risks of poor accrued income management are severe. Inaccurate tracking leads to revenue leakage, bloated balance sheets, and distorted profitability metrics. Organizations risk misstating their financial health, which can lead to compliance audits, loss of investor trust, and critical cash flow bottlenecks.

Anatomy of an Accrued Income Statement

An accrued income statement acts as a vital financial bridge, aligning completed operational work with pending financial recognition. It ensures that revenue is recognized in the period it is earned, regardless of when the cash is received or when the invoice is processed.

The essential components of this statement include the client identifiers, performance obligation statuses, and calculated contract values. By documenting these elements, the statement provides clear visibility into earned but unbilled assets, making it easy for finance teams to justify revenue figures before formal billing occurs.

Standard Document Formats for Revenue Recognition

To standardize the tracking of accrued income, organizations rely on specific document formats that ensure consistency across departments. These structures make it easier to audit and transition unbilled amounts into active invoices.

- Structured Spreadsheets: Highly customizable templates used by growing businesses to log milestones, contract rates, and calculated accruals.

- System-Generated Ledgers: Automated sub-ledgers created within ERP systems that dynamically link operational project hours to financial periods.

- Unbilled Receivables Registers: Specialized reports focusing exclusively on revenue that has been recognized but cannot yet be billed due to contract terms.

Crucial Data Fields for Precise Tracking

Every unbilled revenue template must contain specific data fields to prevent errors and ensure auditability. These fields provide the context necessary for auditors to verify the legitimacy of recognized revenue.

- Project Milestones

- The specific deliverables or progress percentages that trigger revenue recognition under the contract terms.

- Contractual Billing Terms

- The agreed-upon schedule or conditions that dictate when an official invoice can legally be issued to the client.

- Accrual Date

- The exact accounting period or date when the work was performed and the revenue was officially recognized on the ledger.

Leveraging Automation to Reduce Accounting Errors

Manual data entry is the primary cause of errors in unbilled receivable tracking. Modern accounting software eliminates these human errors by automatically capturing operational data and translating it into financial entries based on pre-configured rules.

"By automating the flow of data from project management tools directly to the general ledger, finance departments can significantly accelerate their month-end close while reducing reconciliation discrepancies."

Automated systems monitor contract milestones in real-time. When a milestone is reached, the software automatically creates the appropriate journal entry, ensuring that the financial statements reflect reality without requiring manual intervention from the accounting team.

Auditing and Reconciling Your Accrual Statements

Internal auditors must regularly reconcile unbilled revenue logs against actual billed invoices to prevent financial leakage and ensure reporting accuracy. This structured reconciliation process identifies discrepancies before they impact the annual financial statements.

- Match the unbilled revenue balances from the prior month against the actual invoices issued during the current billing cycle.

- Identify any remaining unbilled balances and verify that the underlying projects are still active and meeting performance obligations.

- Investigate any variances between the accrued revenue estimates and the final invoiced amounts to adjust future recognition formulas.

- Document all reconciliation adjustments in a clear audit trail to satisfy internal control requirements and external auditor reviews.

Best Practices for Compliant Financial Reporting

Maintaining compliance with GAAP and IFRS requires strict adherence to revenue recognition standards, specifically ASC 606 and IFRS 15. Companies must consistently apply these rules to ensure that unbilled revenue reported on the balance sheet reflects genuine contractual progress.

To remain compliant, companies should establish clear written policies for estimating completion percentages, perform regular reviews of unbilled aging reports, and ensure that contracts clearly outline when the right to payment becomes unconditional.

Leave a comment