Financial analysts and CFOs frequently grapple with inconsistent legacy data and rigid spreadsheet formatting when reconstructing historical cash flow statements. These structural discrepancies often lead to reconciliation errors and obscure genuine liquidity trends.

Before deploying a standardized template, it is critical to first map how legacy accounting systems categorized operational transactions over time. Standardizing these historical formats grants finance teams rapid, auditable insights into long-term cash generation, stripping away hours of manual data manipulation.

To leverage this effectively, one vital stipulation must be kept in mind: a template is only as reliable as its underlying classification rules. For example, failing to properly isolate non-cash items, such as depreciation adjustments under the indirect method, can severely distort operating cash flow calculations.

This article provides a blueprint for resolving these analysis challenges by examining optimal template structures, identifying common integration pitfalls, and offering practical strategies to streamline your historical financial reporting.

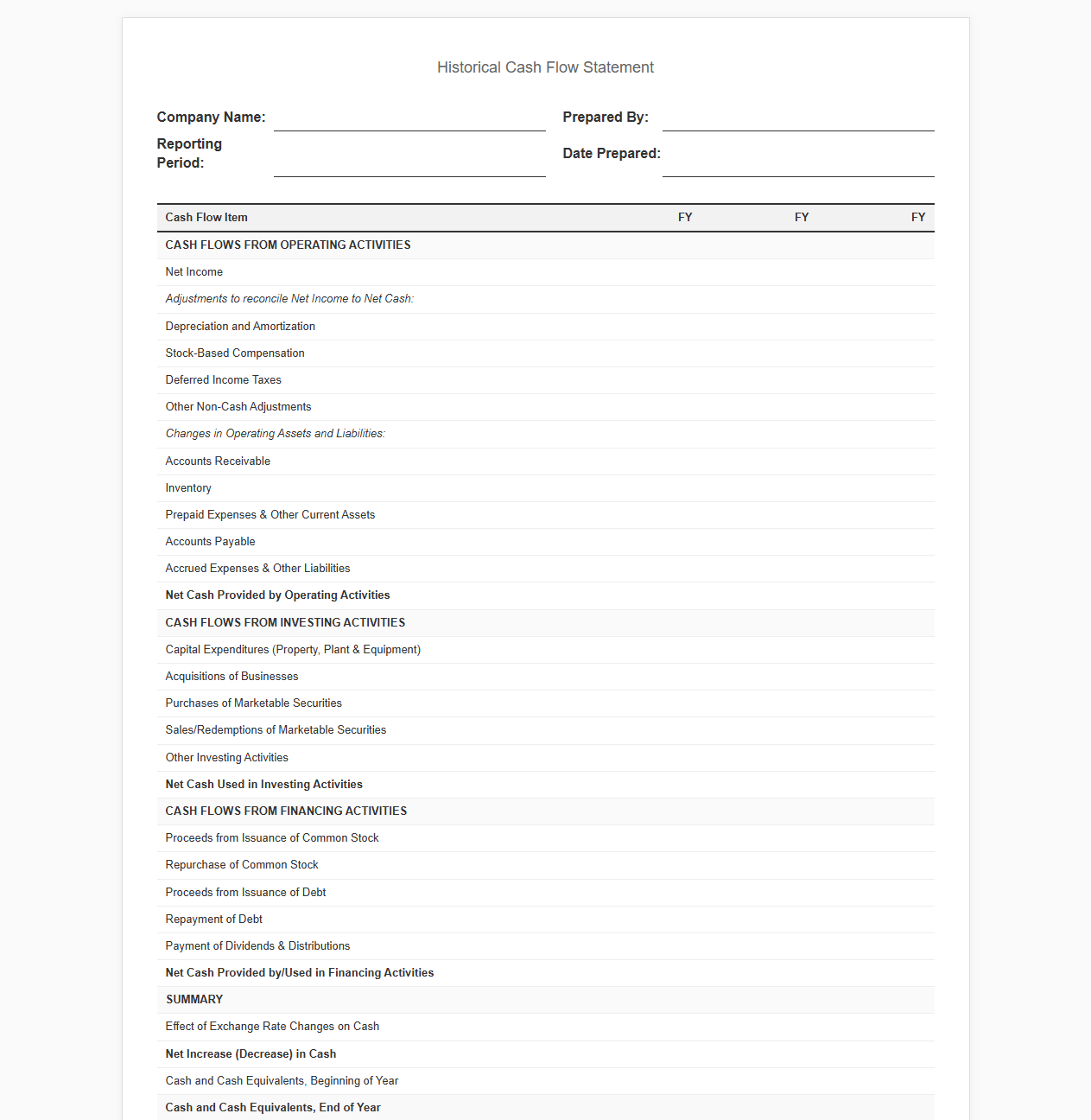

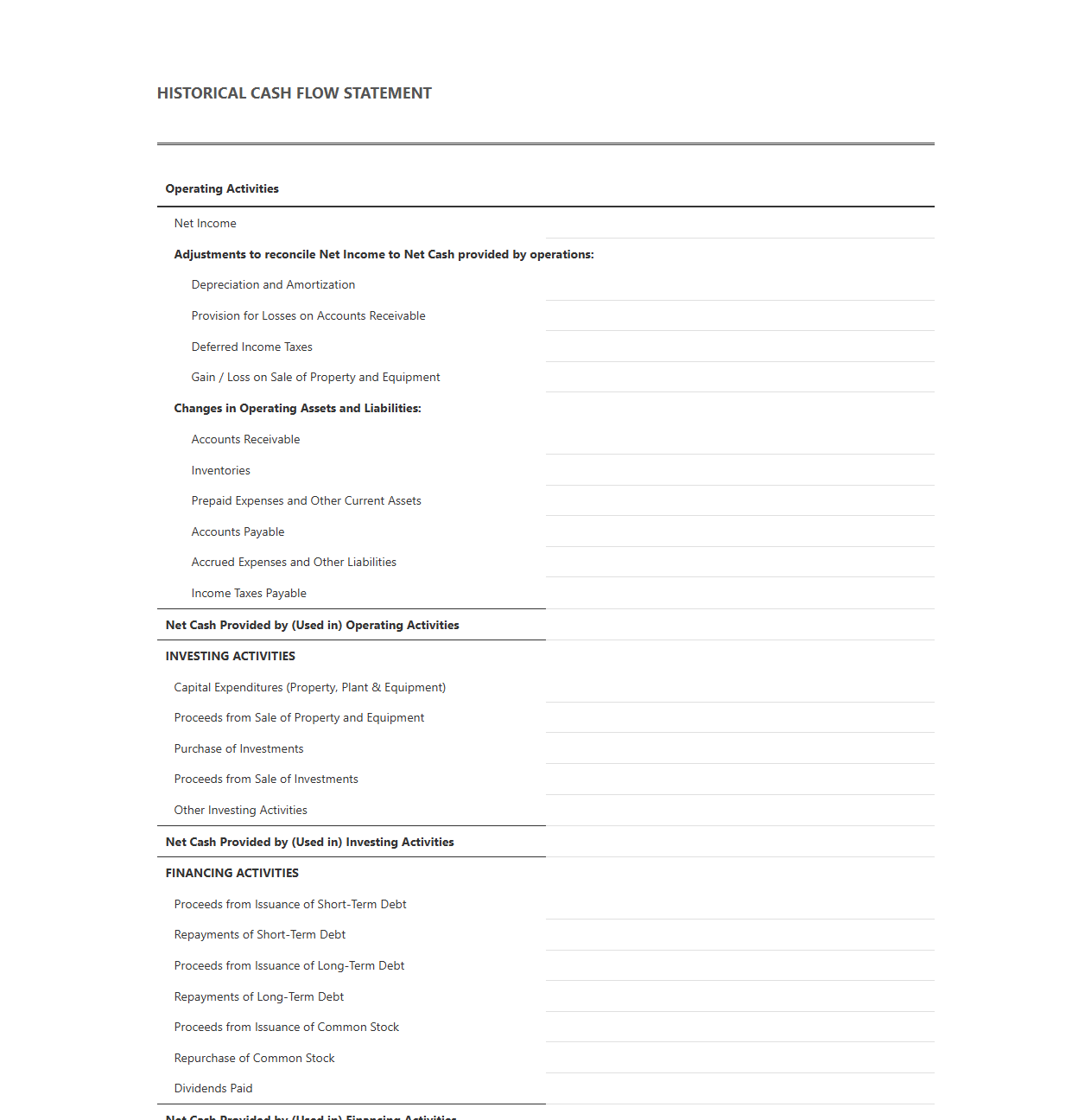

Historical Cash Flow Statement Template

Download: .PDF

Download: .PDF

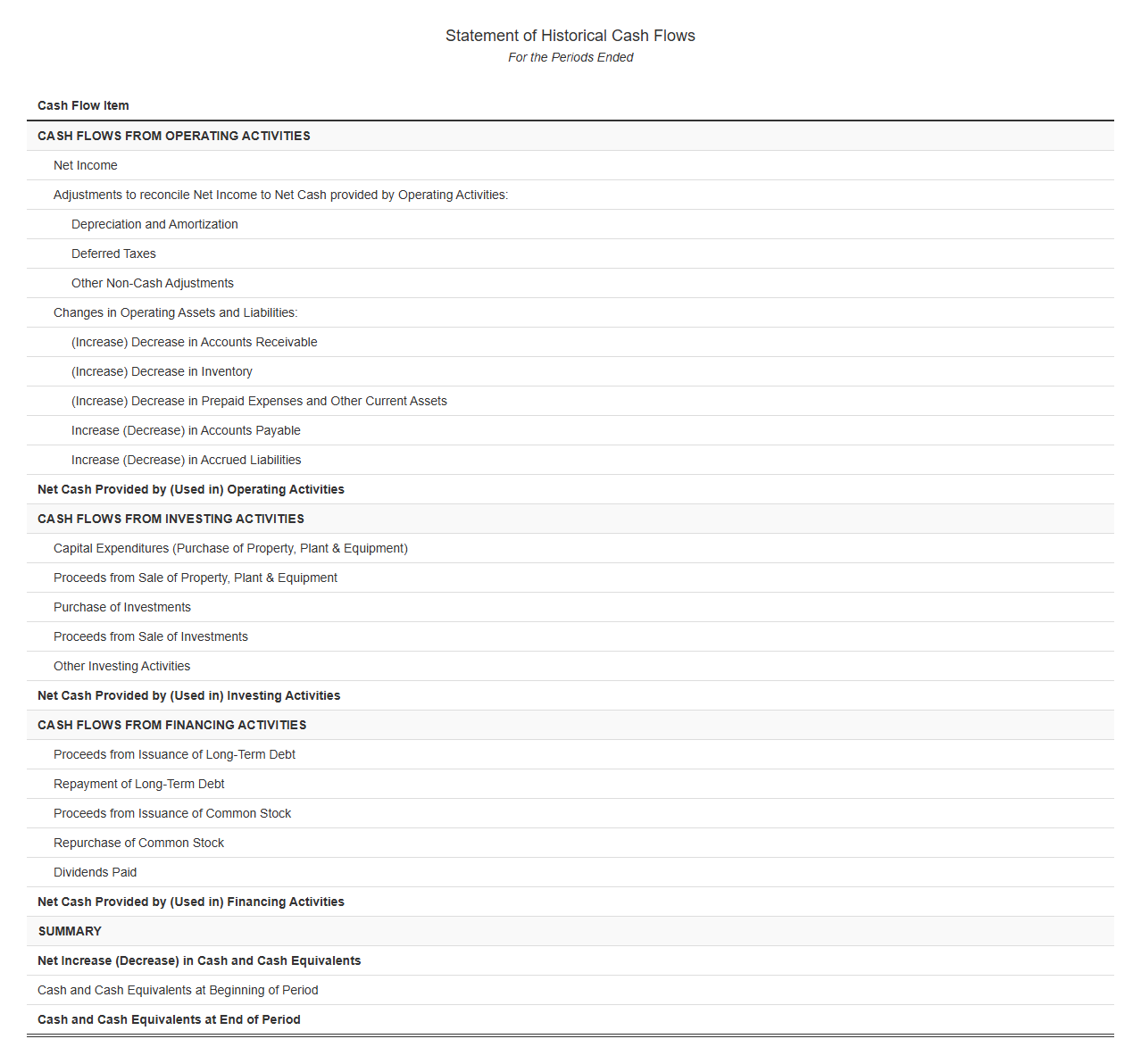

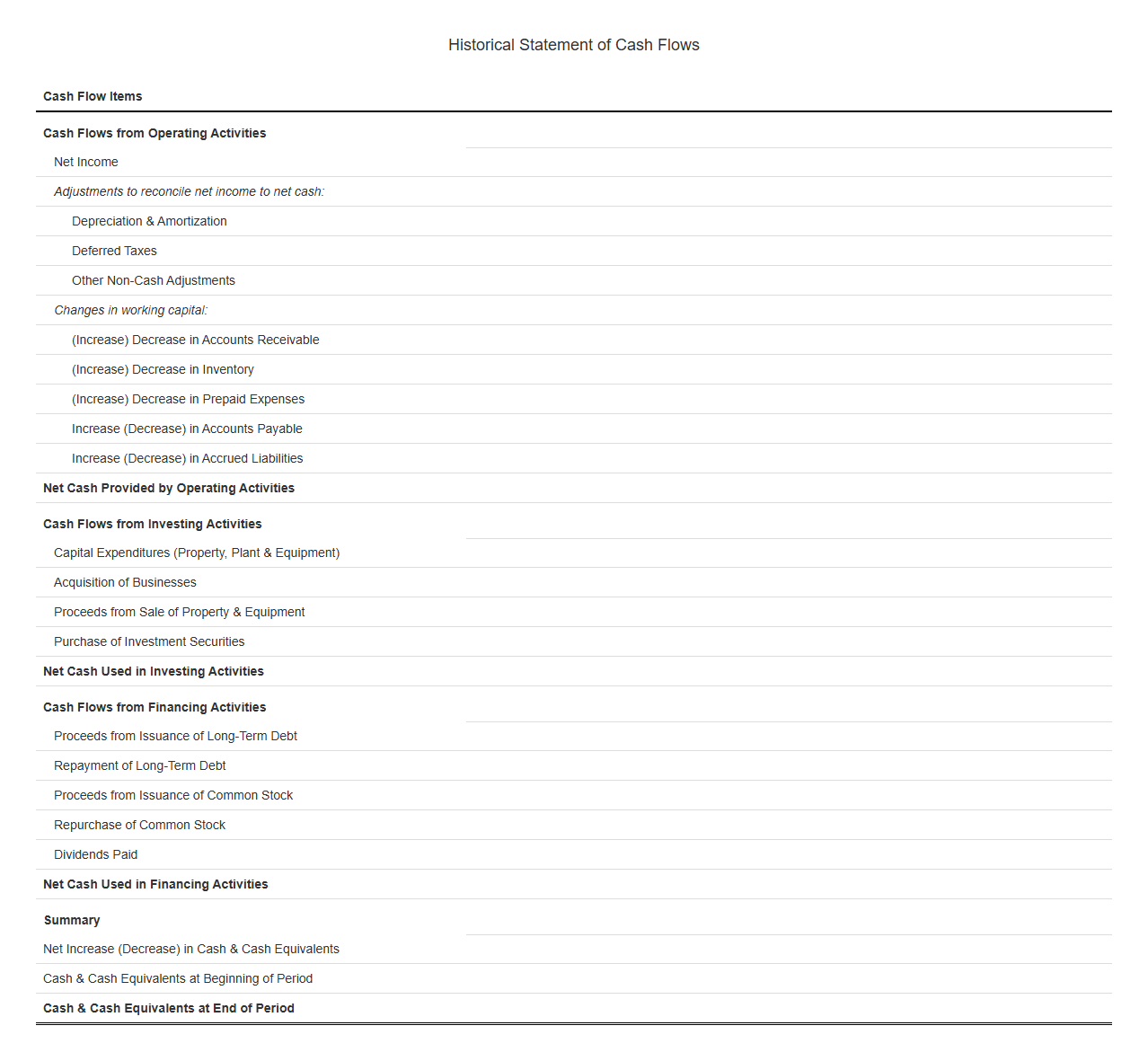

Statement of Historical Cash Flows Template

Download: .PDF

Download: .PDF

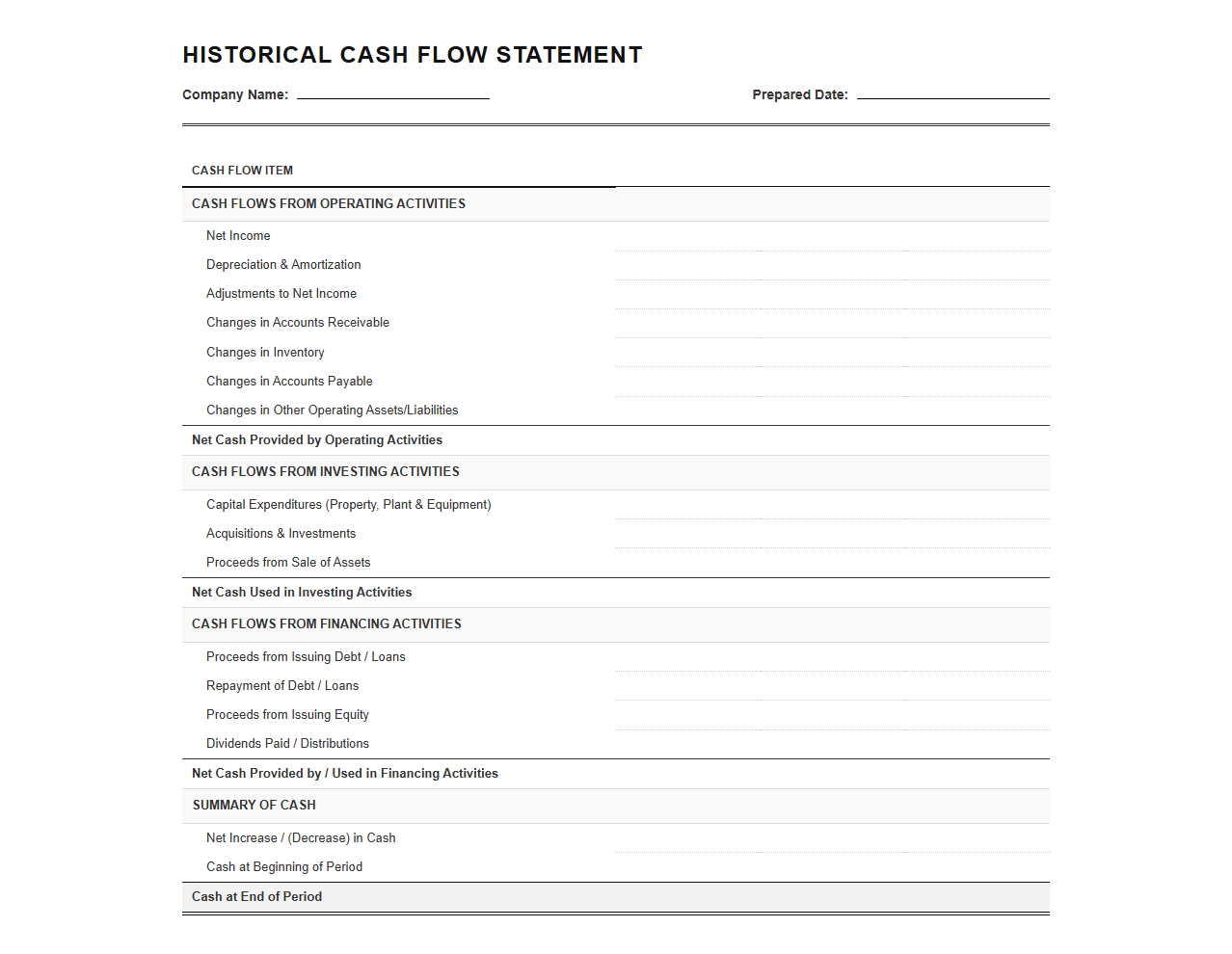

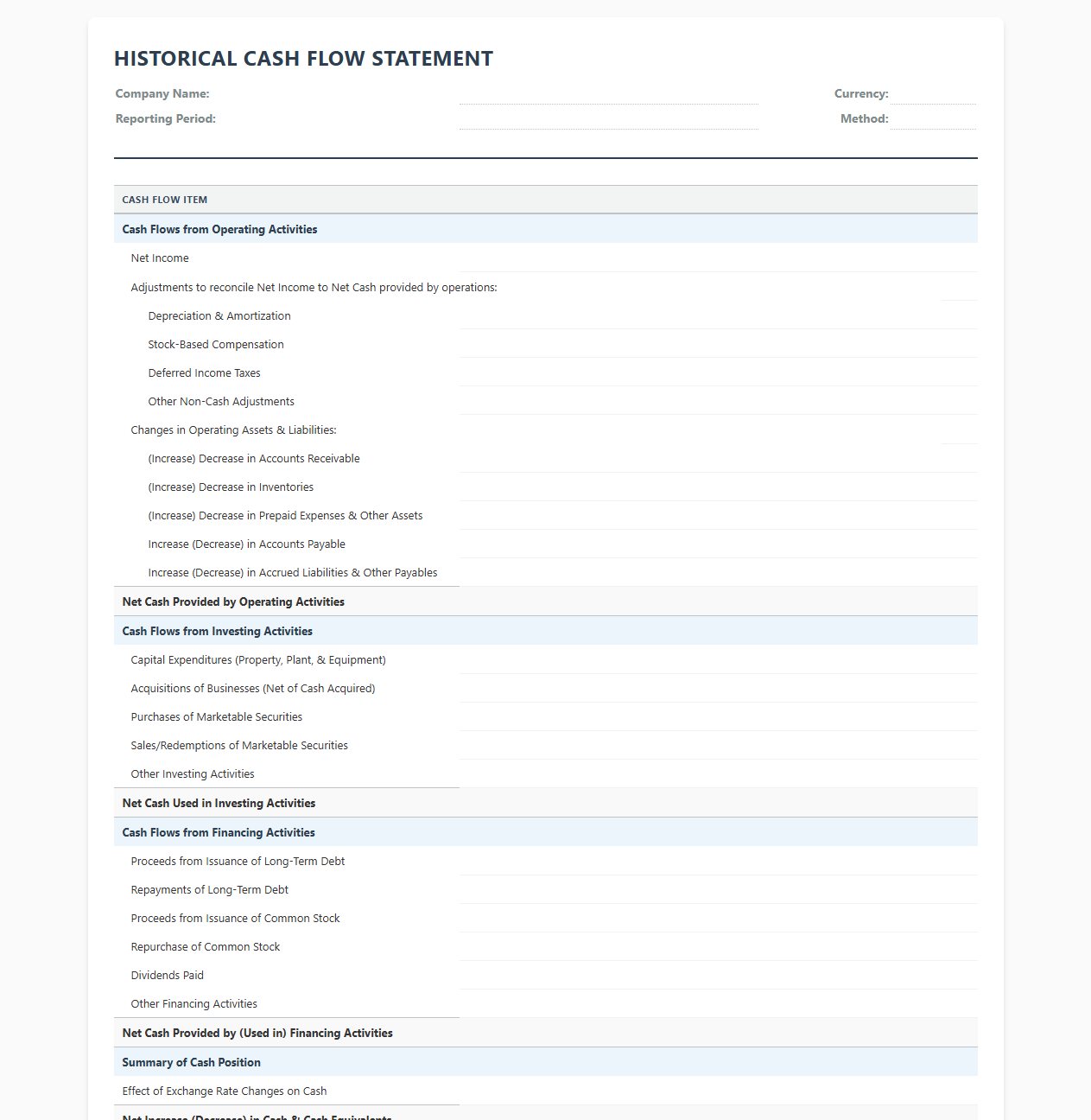

Historical Cash Flow Report Template

Download: .PDF

Download: .PDF

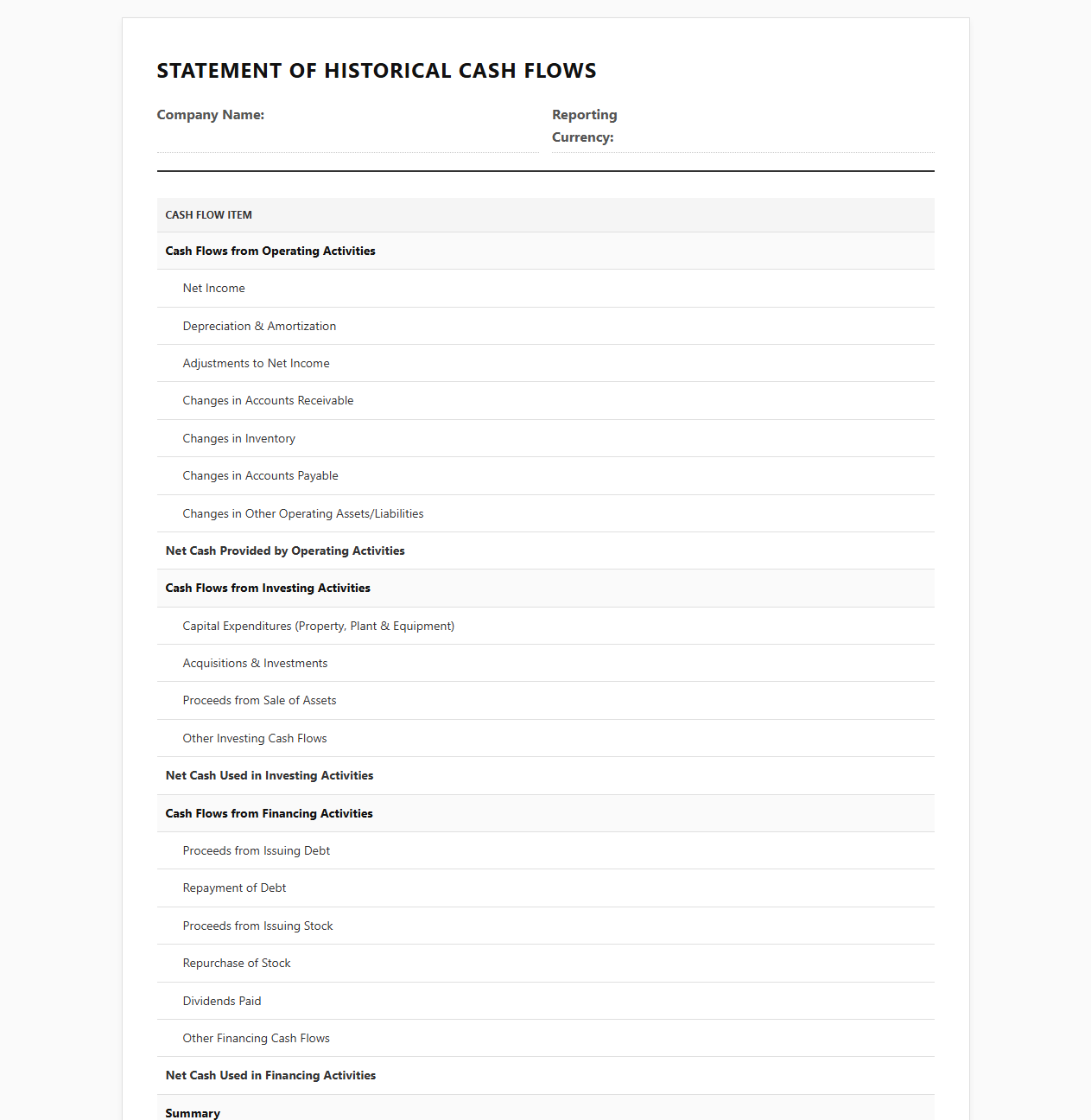

Past Financial Years Cash Flow Template

Download: .PDF

Download: .PDF

Retroactive Cash Flow Statement Template

Download: .PDF

Download: .PDF

Historical Statement of Cash Flows Format

Download: .PDF

Download: .PDF

Multi Year Historical Cash Flow Statement

Download: .PDF

Download: .PDF

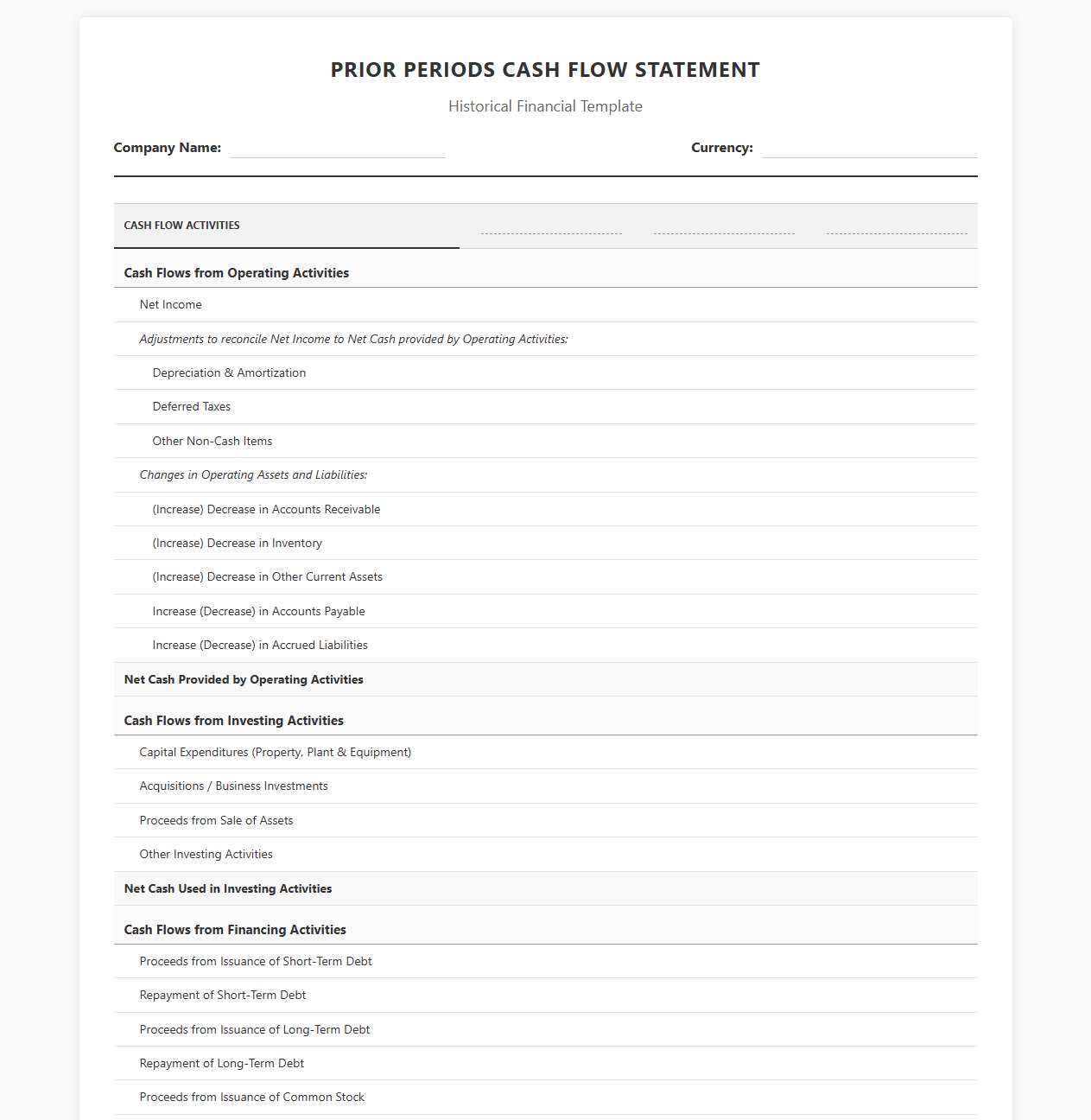

Prior Periods Cash Flow Statement Template

Download: .PDF

Download: .PDF

Demystifying Historical Cash Flow Statements

Historical cash flow statements are the bedrock of fundamental financial analysis. While income statements show accounting profits, the cash flow statement reveals the actual liquidity moving through an enterprise. Understanding these historical patterns is crucial for assessing a company's financial health, debt servicing capacity, and valuation. However, financial analysts frequently face major challenges when dealing with inconsistent formatting across different reporting periods and systems.

The Pitfalls of Inconsistent Template Formats

When historical financial data is pulled from multiple legacy systems or different accounting teams, template formats rarely align. This inconsistency introduces significant risk and inefficiency into the valuation process.

- Mismatched line items that force manual reconciliation.

- Varying spreadsheet structures that break automated financial models.

- Inconsistent naming conventions for identical cash transactions.

Standardizing Cash Flow from Operating Activities

Reconciliation Mechanics

The operating activities section requires careful alignment because companies often use different starting points for the indirect method. To resolve formatting discrepancies, analysts must systematically reconcile net income to net cash provided by operating activities by isolating non-cash adjustments.

Operating Cash Flow = Net Income + Non-Cash Expenses + Changes in Working Capital

Tracking Capital Expenditures in Investing Activities

Structuring Capital Outlays

Investing activities must be uniformly structured to separate routine maintenance capital expenditures from growth-oriented acquisitions. Ensuring that cash inflows from asset sales and outflows for property, plant, and equipment (PP&E) are formatted consistently is vital for accurate free cash flow calculations.

"Consistency in classifying capital expenditures is the key to unlocking reliable multi-year trend analyses and forecasting capital efficiency."

Streamlining Financing Activities Reporting

Capital Structure Movements

The financing activities section tracks how an organization funds its operations. Formatting this section requires a clear separation of equity transactions, debt movements, and shareholder returns to prevent distortion of the net cash position.

- Debt issuance and repayment schedules.

- Dividend distributions and share buyback programs.

- Principal payments on finance leases.

Leveraging Automation for Template Reconciliation

Manual data entry is highly prone to human error, which is why modern analysts use automated mapping tools to bridge formatting gaps across historical statements.

- Map disparate source items to a standardized master ledger chart.

- Use dynamic lookup formulas to aggregate rows automatically.

- Deploy validation checks to ensure the ending cash balances tie out to the balance sheet.

Establishing a Unified Cash Flow Template for Future Analysis

Creating a master historical cash flow template is the most effective way to eliminate formatting errors permanently. By locking the structural design and establishing clear data-entry protocols, teams can accelerate their valuation workflows. A standardized framework ensures that future analyses remain accurate, comparable, and rapid.

Leave a comment