For many business owners, cleanly separating personal withdrawals from business equity remains a persistent accounting headache, often leading to chaotic balance sheets and tax-season panic. Before implementing a tracking system, it is vital to position these transactions correctly: an owner's draw is not a standard salary, but a direct reduction of the business's capital. Properly structuring these transactions grants owners absolute financial transparency, safeguarding their equity valuation and keeping clean boundaries for stakeholders.

Please note that while the frameworks provided herein serve as robust tracking models, they should be adapted to your specific corporate structure and local regulations. By utilizing concrete tools such as capital account ledgers and formalized draw request statements, you establish an audit-ready paper trail. Below, we will explore the core mechanics of equity tracking, present professional statement templates, and outline best practices for seamless monthly reconciliation.

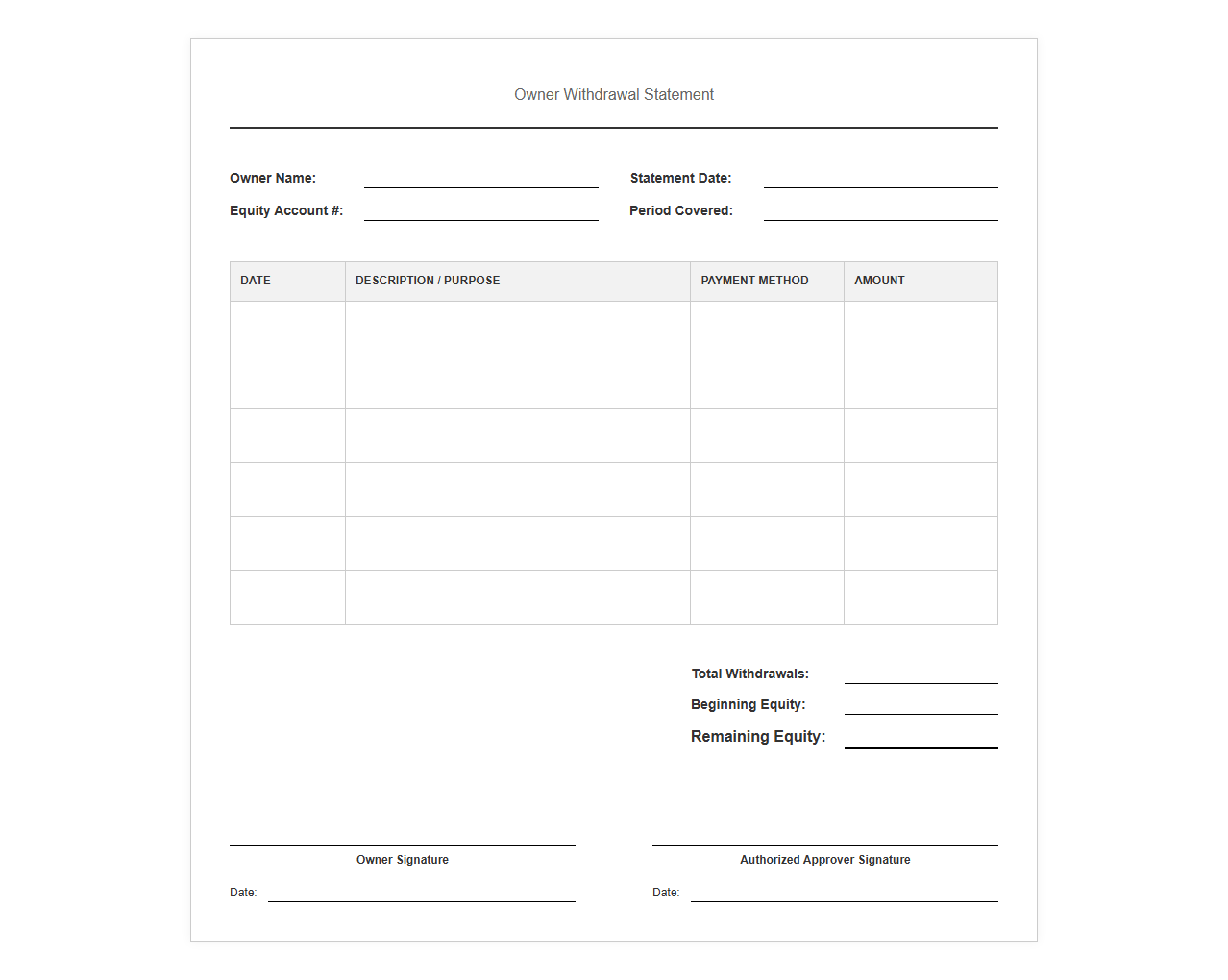

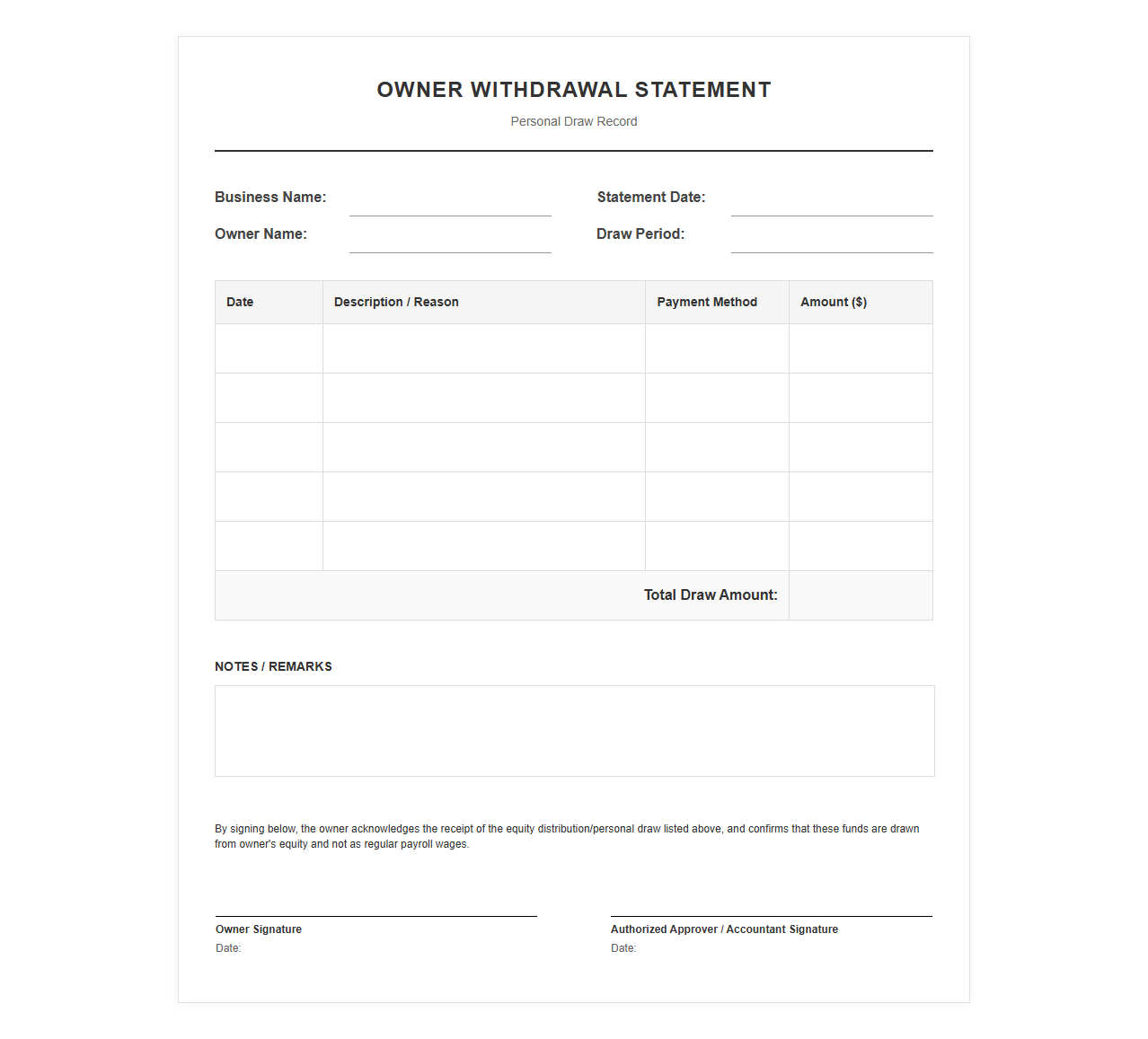

Owner Withdrawal Statement Template

Download: .PDF

Download: .PDF

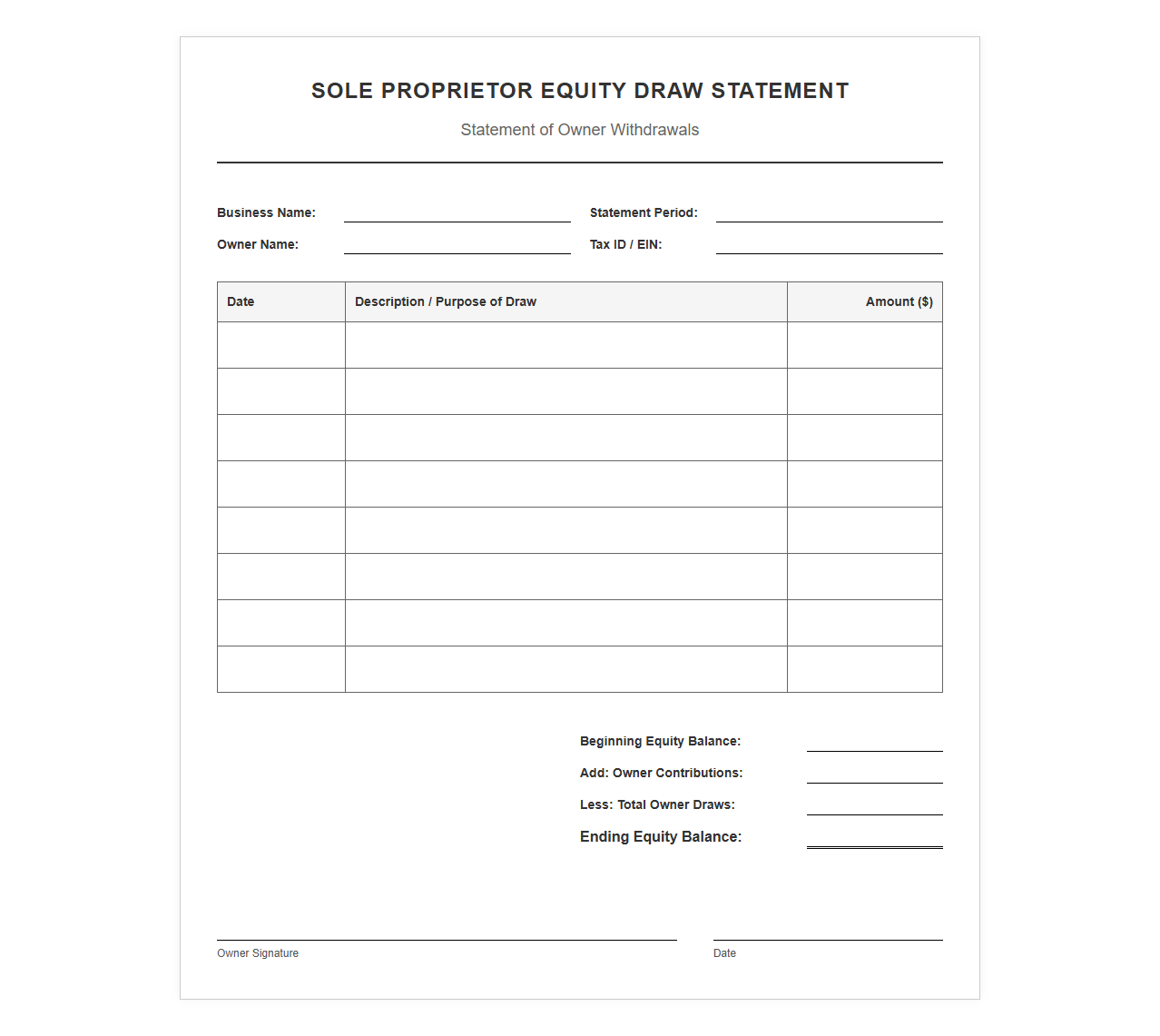

Sole Proprietor Equity Draw Statement

Download: .PDF

Download: .PDF

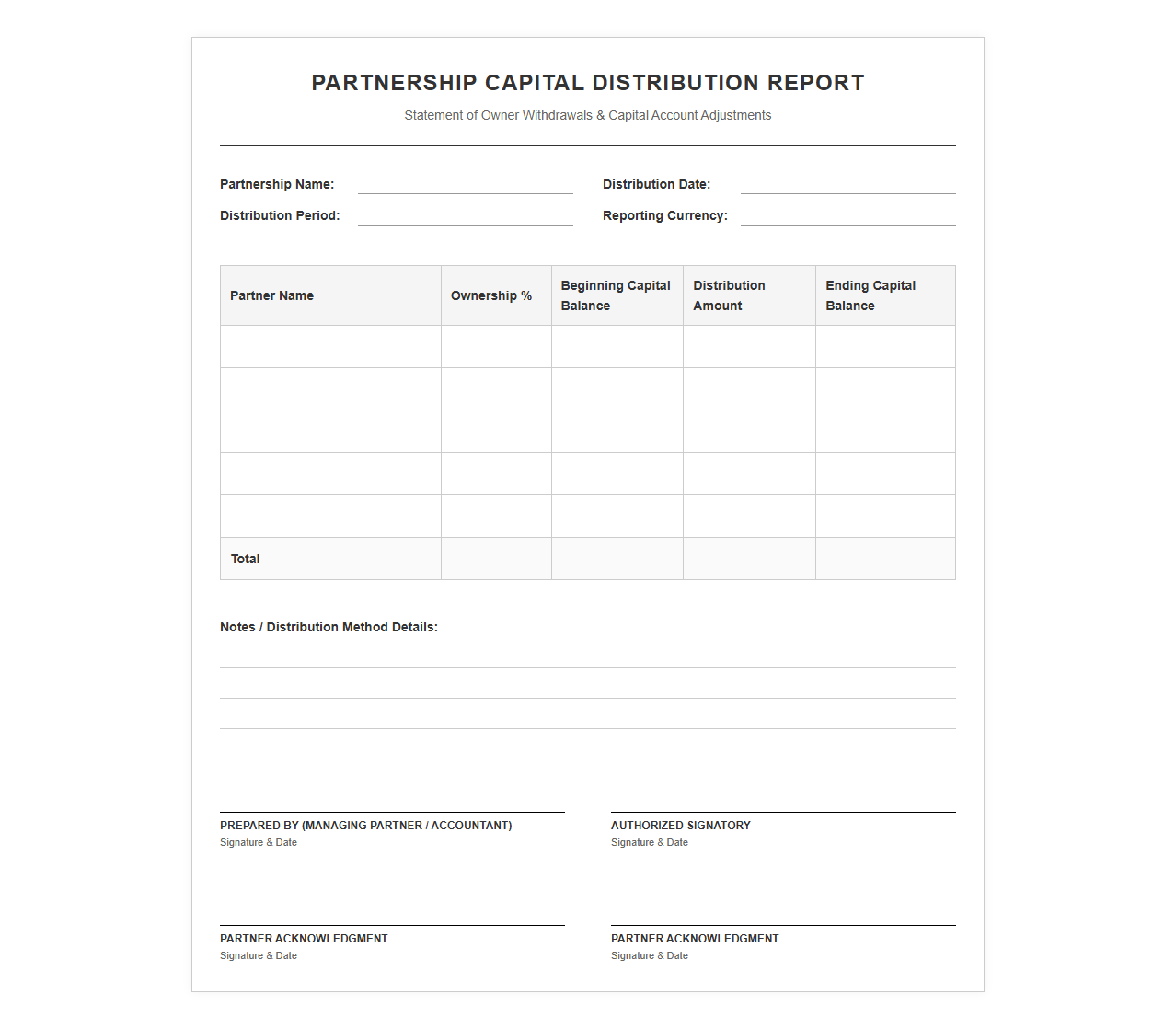

Partnership Capital Distribution Report Template

Download: .PDF

Download: .PDF

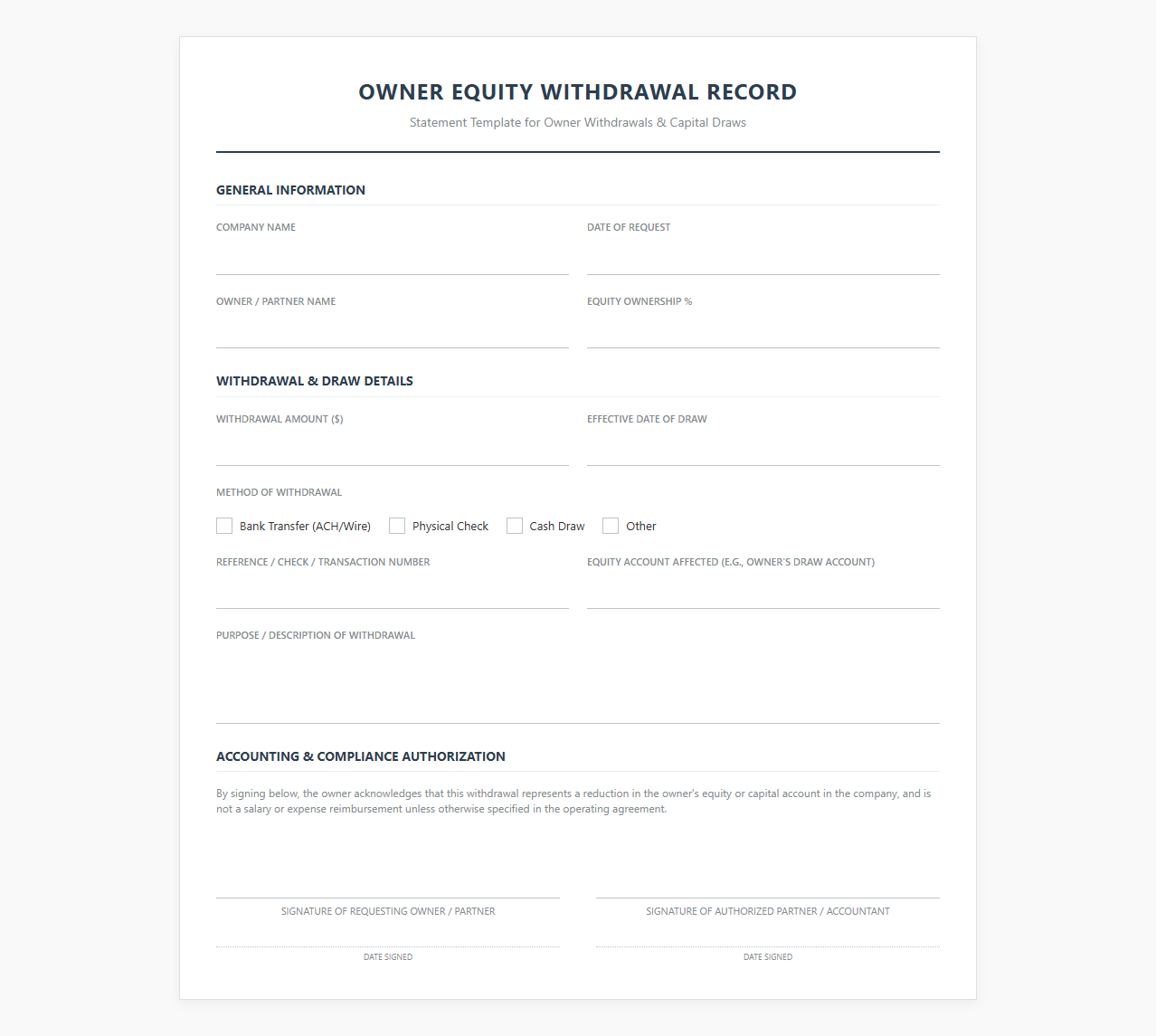

Owner Equity Withdrawal Record Form

Download: .PDF

Download: .PDF

Business Owner Personal Draw Statement

Download: .PDF

Download: .PDF

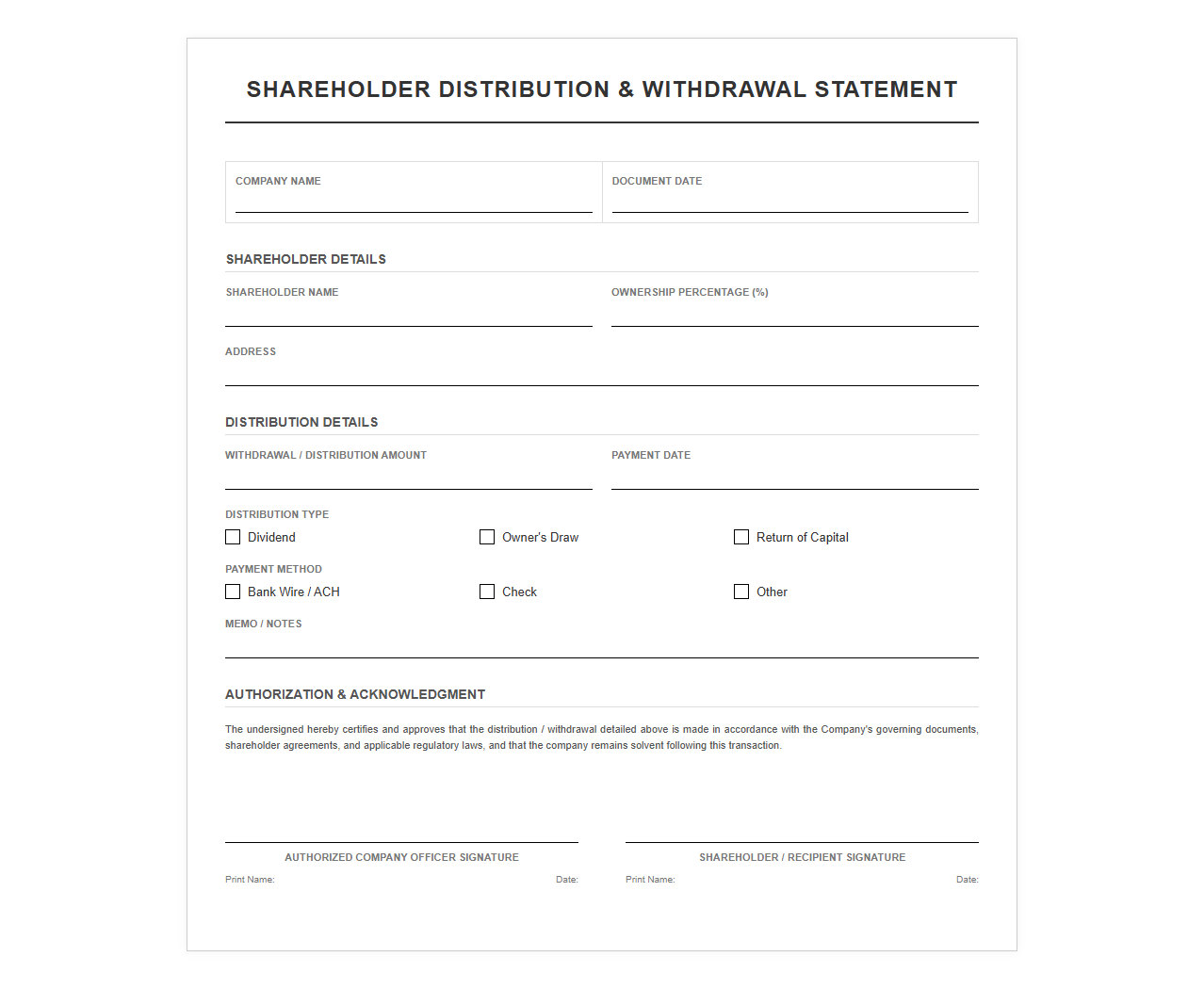

Shareholder Distribution and Withdrawal Template

Download: .PDF

Download: .PDF

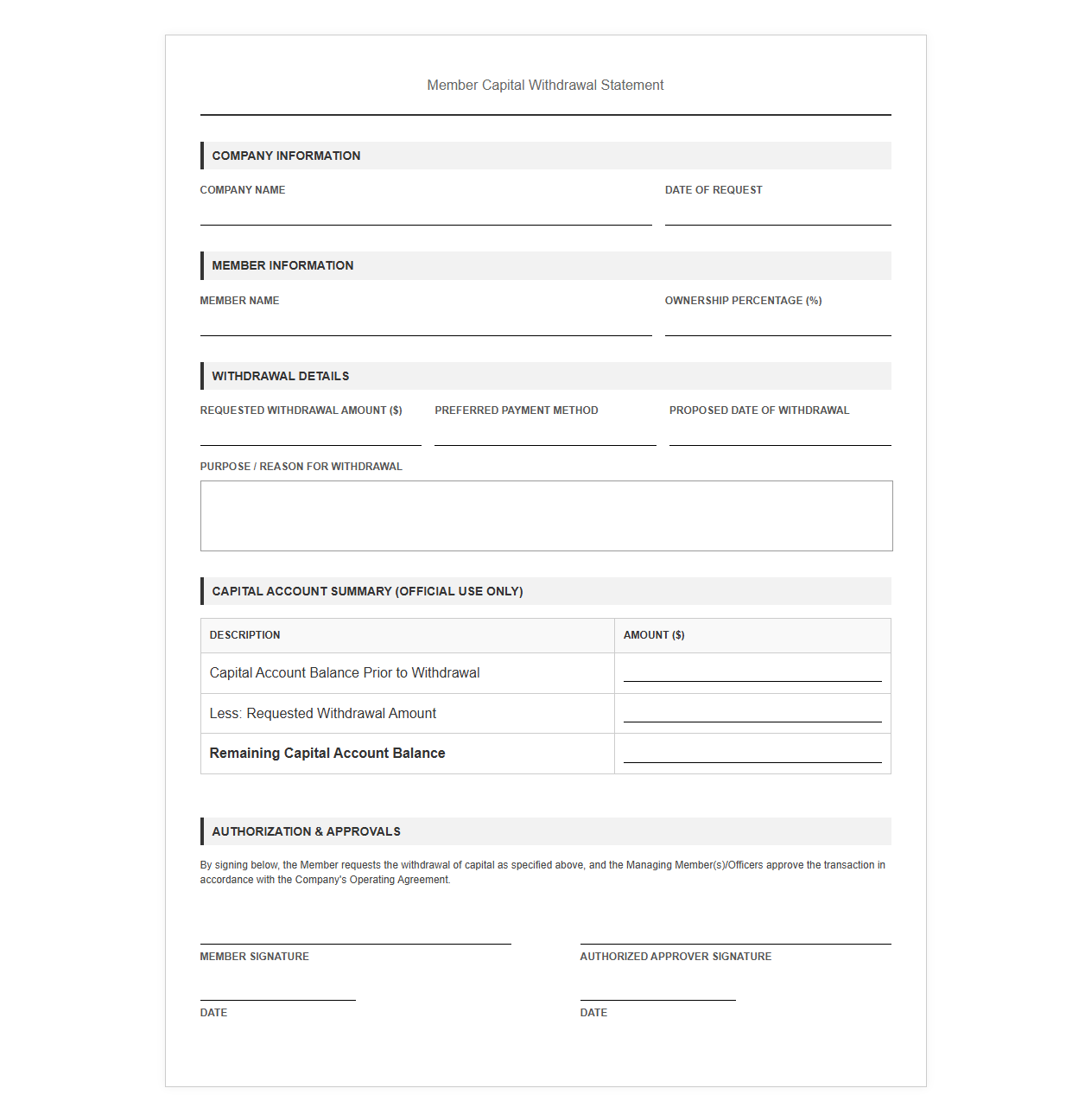

Member Capital Withdrawal Statement Form

Download: .PDF

Download: .PDF

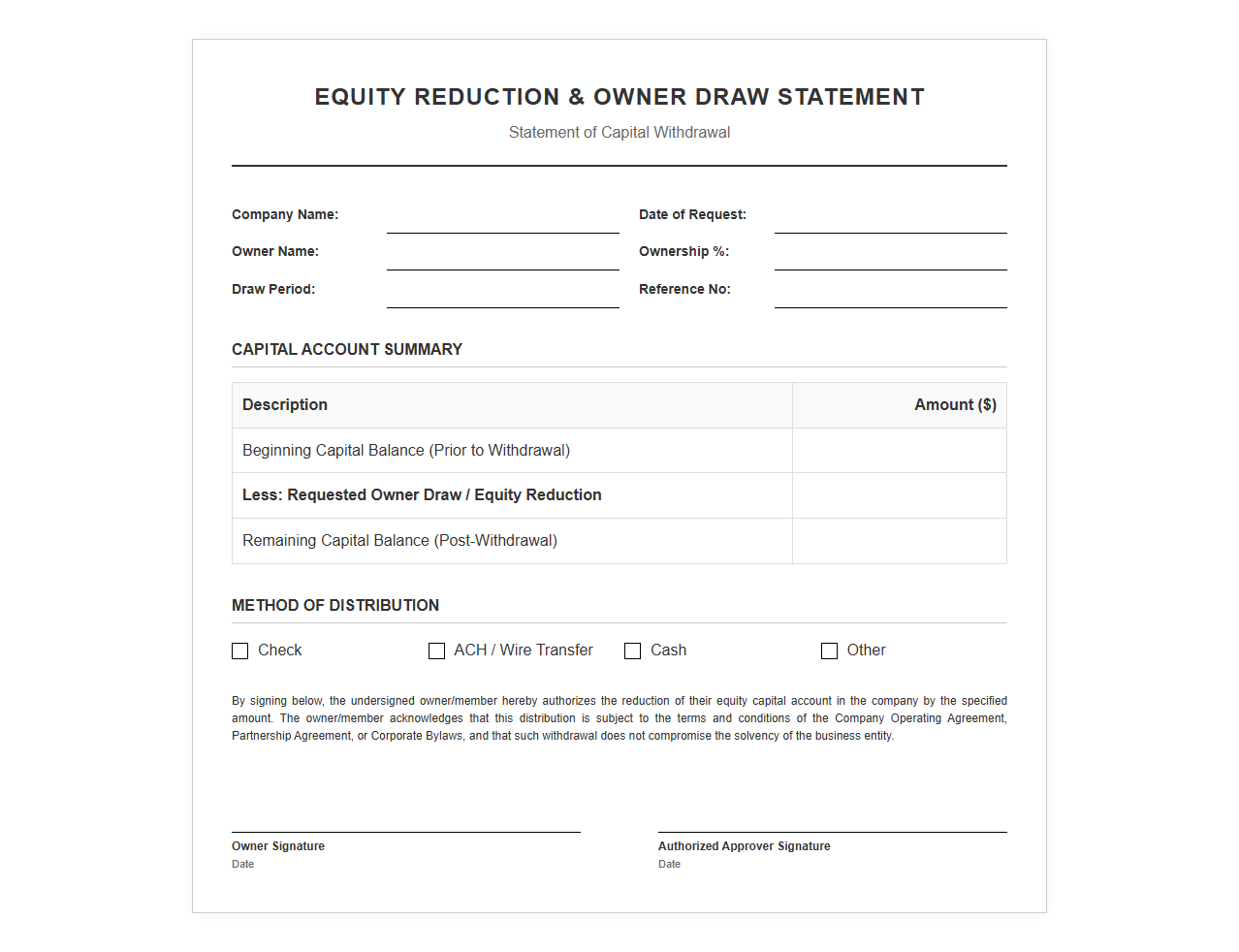

Equity Reduction and Owner Draw Template

Download: .PDF

Download: .PDF

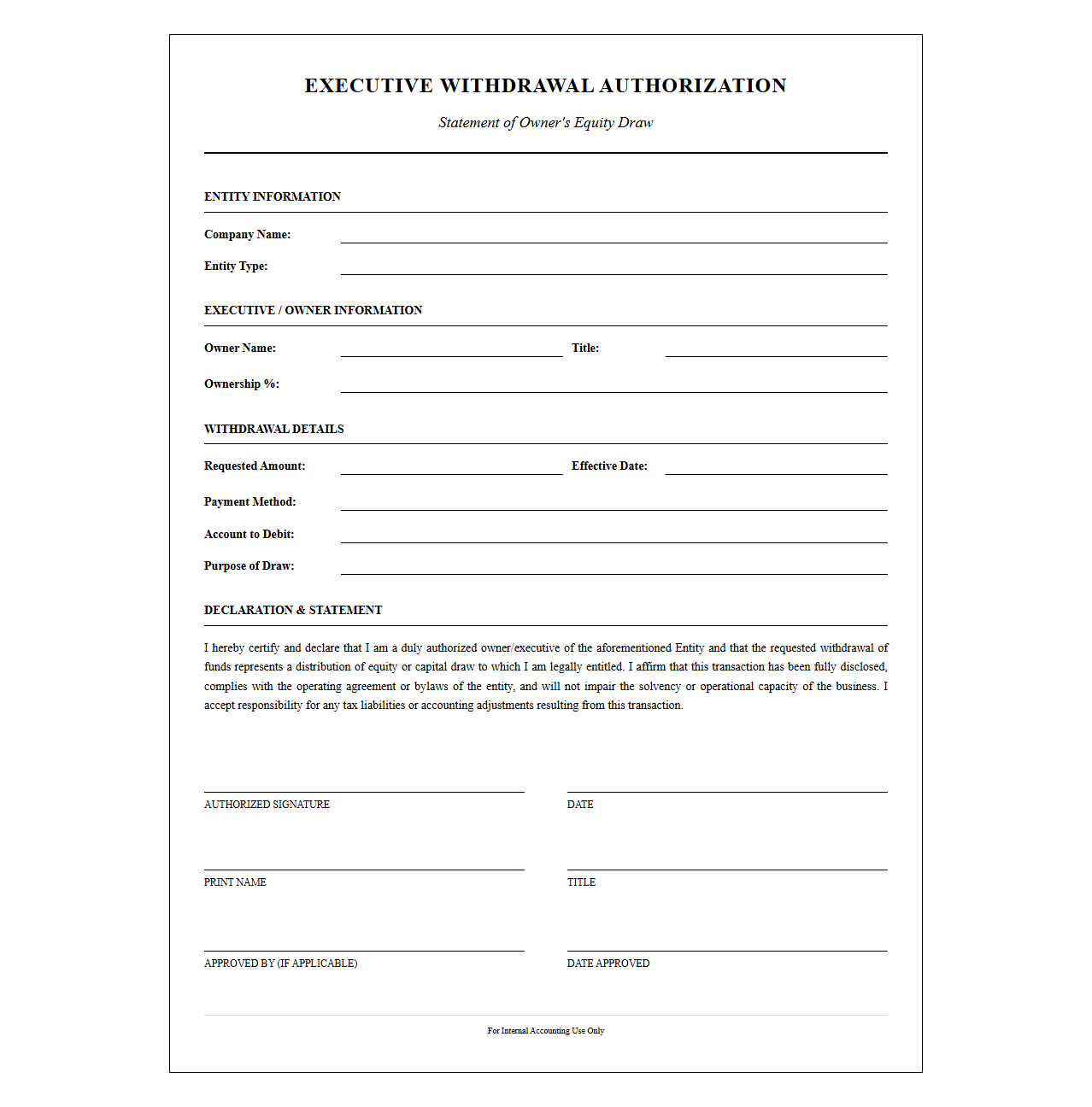

Executive Withdrawal Authorization and Statement

Download: .PDF

Download: .PDF

Understanding Owner's Draws and Equity Tracking

An owner's draw is a method by which business owners withdraw funds from their company's accumulated earnings or capital for personal use. Unlike regular payroll, which classifies owners or employees as W-2 wage earners receiving a salary with automated tax withholdings, an owner's draw directly reduces the business's overall equity. Utilizing a draw is highly common in pass-through entities where business profits flow directly to the owners' personal tax returns.

Maintaining precise tracking of these distributions is critical for long-term financial health. Accurately documenting every withdrawal ensures that the owner's equity ledger remains correct, which is vital for evaluating the company's actual valuation. Without a meticulous record of these transactions, a business risks misrepresenting its cash flow, overdrawing from its capital account, and causing imbalance in its retained earnings, which can jeopardize solvency and distort financial reporting.

Legal, Tax, and Compliance Considerations

Choosing to take an owner's draw rather than a standard W-2 salary carries significant legal and tax implications depending on your business structure. Because draws are not subject to immediate payroll tax withholding, improper classification can lead to substantial tax penalties at year-end. Furthermore, maintaining clear separation between personal withdrawals and business operations is crucial for maintaining corporate protections.

- Sole Proprietorships: The business and the owner are legally identical. All business profits are taxed as personal income, making owner's draws tax-free at the time of withdrawal, though they are subject to self-employment tax.

- Partnerships: Individual partners take draws against their share of the partnership profits. These must be recorded in individual partner capital accounts to ensure tax liabilities are distributed accurately according to the partnership agreement.

- Single-Member and Multi-Member LLCs: While taxed similarly to sole proprietorships or partnerships by default, LLC owners must document draws formally. Fumbling this separation can lead to courts "piercing the corporate veil," exposing personal assets to business liabilities.

- S-Corporations: S-Corp owners who provide services to the business must receive "reasonable compensation" via W-2 payroll before taking non-dividend distributions (draws) to avoid IRS scrutiny.

Anatomy of a Professional Draw Statement

A professional owner's draw statement must accurately reflect the flow of capital out of the business and its direct impact on equity. To maintain clear bookkeeping records, a standard statement should structure this financial data in a logical, chronological sequence.

- Beginning Equity Balance: The total starting value of the owner's capital account at the beginning of the financial period.

- Capital Contributions: Any personal funds or assets the owner invested in the business during the period.

- Transaction Dates: The exact calendar dates on which each individual draw was executed.

- Draw Amounts: The precise monetary value of cash or assets removed from the business for personal use.

- Ending Capital Balance: The calculated remaining equity in the business after accounting for contributions, net income, and total draws.

Step-by-Step Accounting Procedures for Recording Draws

To record an owner's draw accurately, bookkeepers rely on double-entry accounting. Because an owner's draw is not an expense, it does not appear on the income statement; instead, it is recorded on the balance sheet as a temporary equity account that reduces total equity.

Step 1: Record the cash withdrawal. When cash is removed from the business bank account, credit the Cash asset account to reflect the outflow of funds.

Credit: Cash (Asset)

Step 2: Record the reduction in equity. Debit the Owner's Draw account (an equity account) to offset the cash reduction.

Debit: Owner's Draw (Equity)

Step 3: Close the draw account at year-end. At the end of the fiscal year, close the temporary Owner's Draw account balance directly into the permanent Owner's Capital account.

Debit: Owner's Capital | Credit: Owner's Draw

Sole Proprietorship Draw Tracking

Statement Template for Sole Proprietors and Single-Member LLCs

Sole proprietors can use this simple text-based template to log their personal draws periodically. Keeping this file updated in your digital records provides a clear audit trail for your accountant.

=========================================

OWNER'S DRAW RECORD TEMPLATE

=========================================

Business Name: _______________________

Owner Name: _______________________

Reporting Period: [Month/Quarter, Year]

1. Beginning Capital Balance: $ _________

2. (+) New Owner Investments: $ _________

3. (+) Share of Net Income: $ _________

-----------------------------------------

Subtotal Equity: $ _________

4. (-) Owner's Draws:

- Date: [MM/DD/YYYY] Amt: $ _________

- Date: [MM/DD/YYYY] Amt: $ _________

- Date: [MM/DD/YYYY] Amt: $ _________

Total Draws for Period: ($ ________)

-----------------------------------------

5. Ending Capital Balance: $ _________

Owner Signature: _______________________ Date: _________

Multi-Member Partnership Tracking

Multi-Member Partnership Capital Account Template

For businesses with multiple partners, tracking equity requires side-by-side transparency. This table structure allows partnerships to monitor individual capital contributions, draws, and final equity allocations proportionally.

| Partner Name | Beginning Capital | Contributions | Allocated Net Income | Draws (YTD) | Ending Capital Balance |

|---|---|---|---|---|---|

| Partner A | $50,000 | $5,000 | $15,000 | ($10,000) | $60,000 |

| Partner B | $75,000 | $2,000 | $15,000 | ($20,000) | $72,000 |

| Partner C | $100,000 | $10,000 | $30,000 | ($15,000) | $125,000 |

Best Practices for Long-Term Equity Ledger Management

To keep your business financially sound and simplify your tax filing processes, reconcile your equity ledger at the end of every month. Regular reconciliation ensures that your bank accounts align perfectly with your internal books, preventing costly errors. When presenting your financial statements to a CPA during tax season, clean ledger logs save time and reduce accounting fees by eliminating the need for forensic bookkeeping.

Critical Warning: Never mix personal expenses directly with business checking accounts. Always transfer your calculated draw amount to your personal bank account first, then spend it from there. Commingling funds destroys legal liability protections and invites IRS audits.

Leave a comment