Managing revenue distribution among business partners often introduces complex administrative friction, especially when attempting to align fluctuating cash flows with diverse ownership agreements. Before executing payouts, partners must first reconcile their operational figures against rigid tax regulations and legal agreements. Utilizing structured income statement templates grants partnerships the ultimate benefit of financial clarity, automating calculations to prevent costly internal disputes.

While these templates streamline reporting, they are designed as foundational frameworks rather than direct substitutes for certified legal or accounting counsel. A robust template must accurately capture specific variables, including individual capital accounts, preferred returns, and tiered profit-sharing ratios. In this article, we will examine the essential templates required for accurate partnership reporting, demonstrate how to customize them for your business structure, and outline best practices for maintaining transparent financial records.

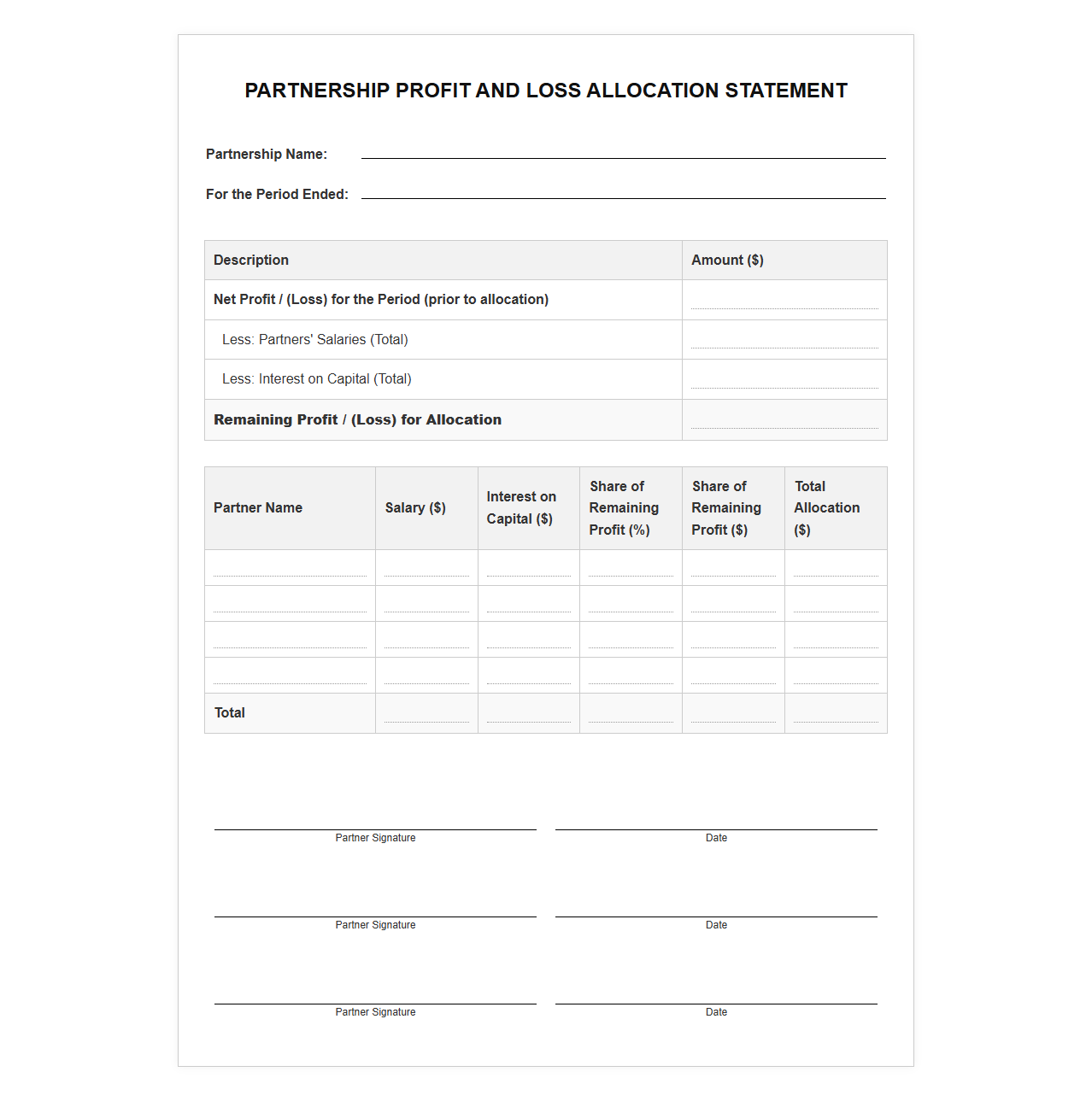

Partnership Profit and Loss Allocation Statement

Download: .PDF

Download: .PDF

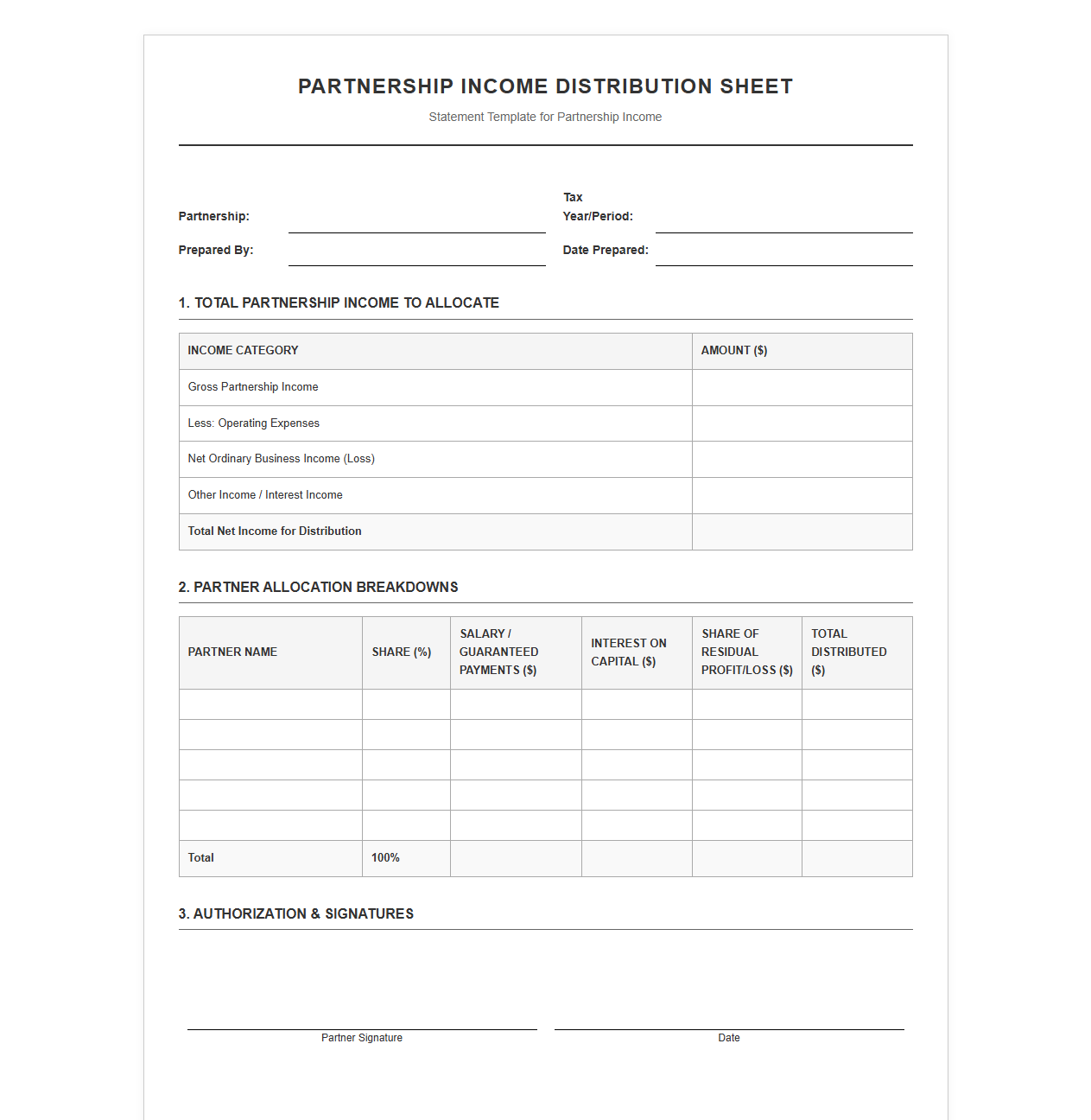

Partnership Income Distribution Sheet

Download: .PDF

Download: .PDF

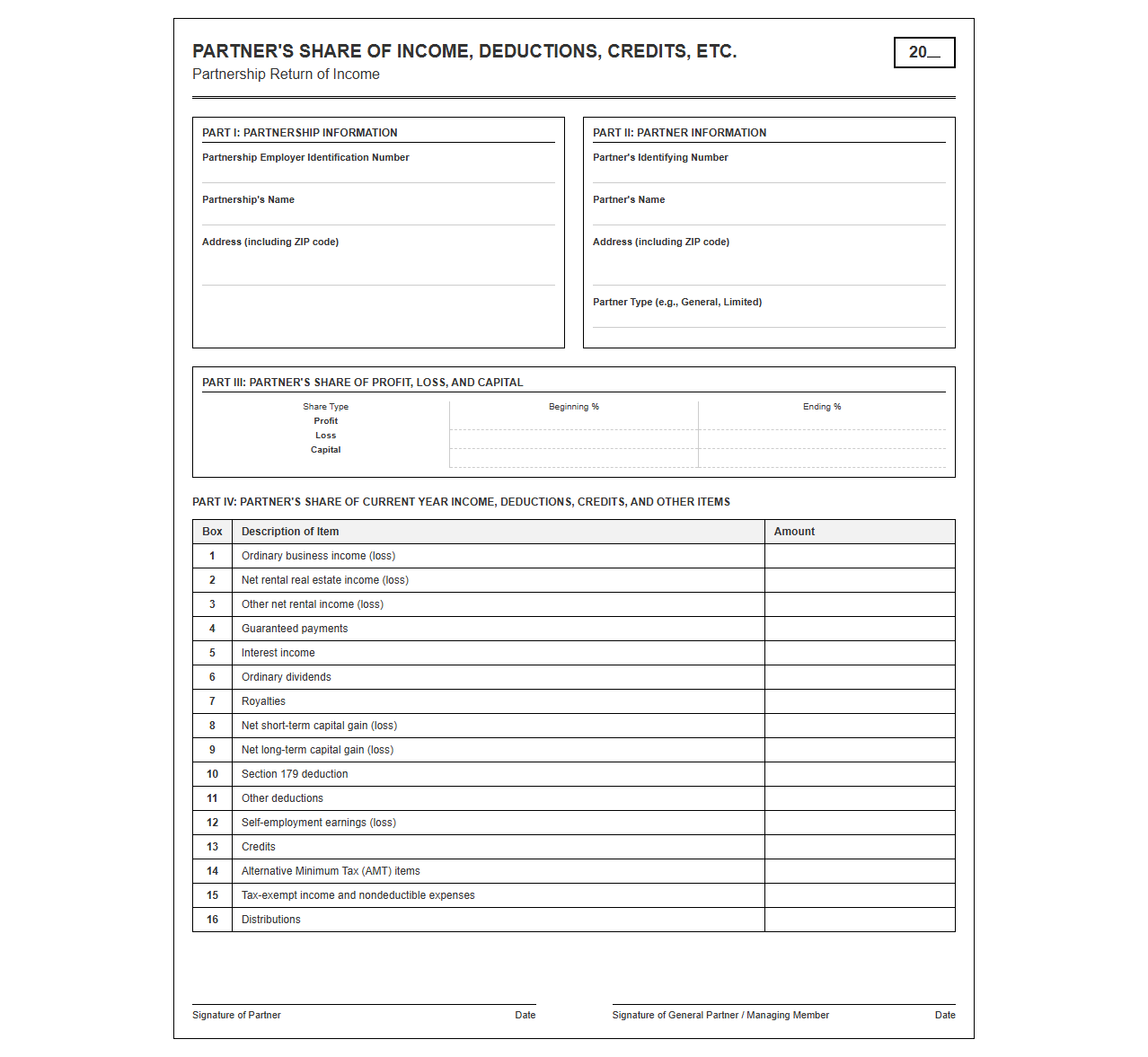

Partner Share of Income and Expenses Template

Download: .PDF

Download: .PDF

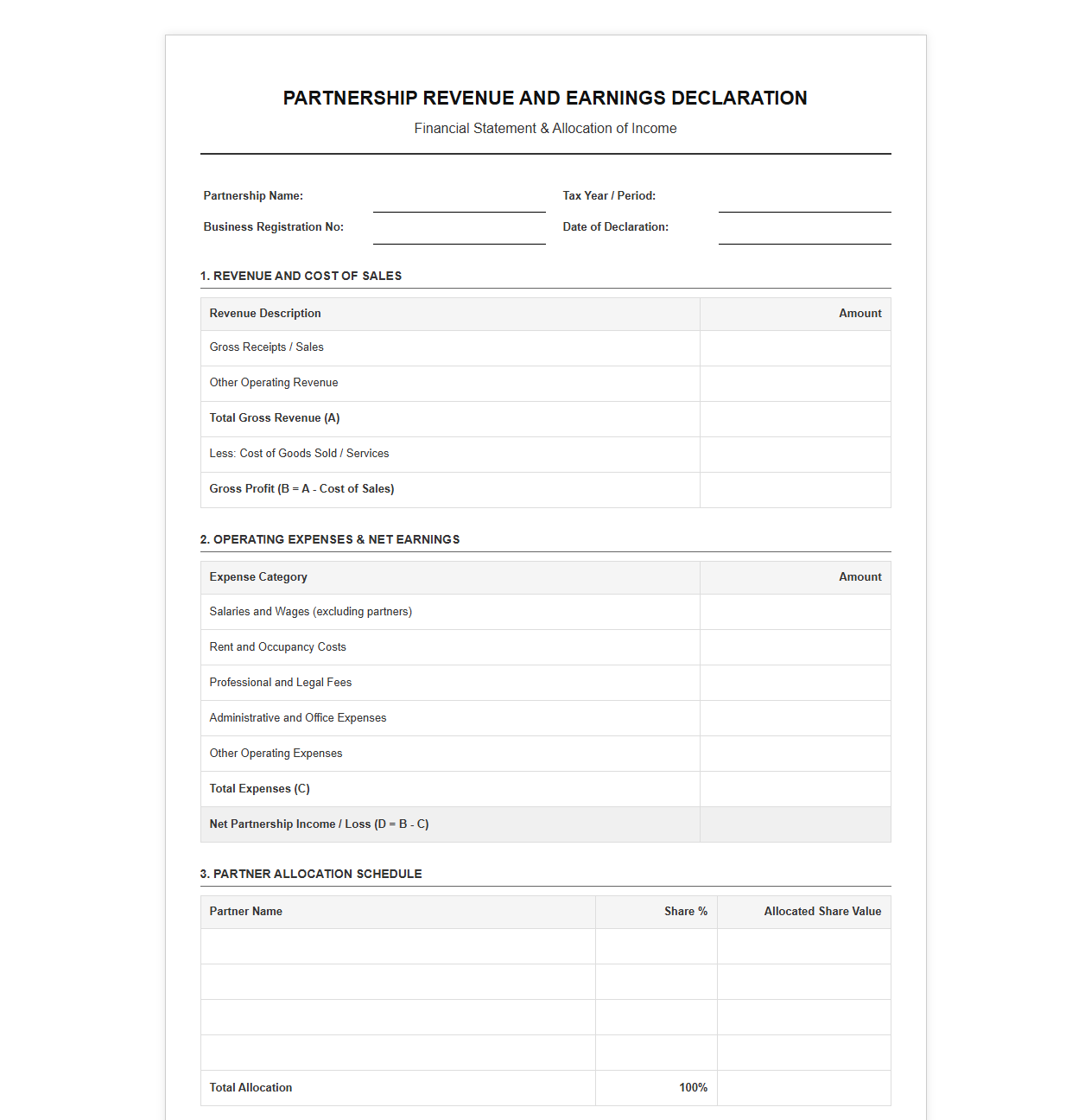

Partnership Revenue and Earnings Declaration

Download: .PDF

Download: .PDF

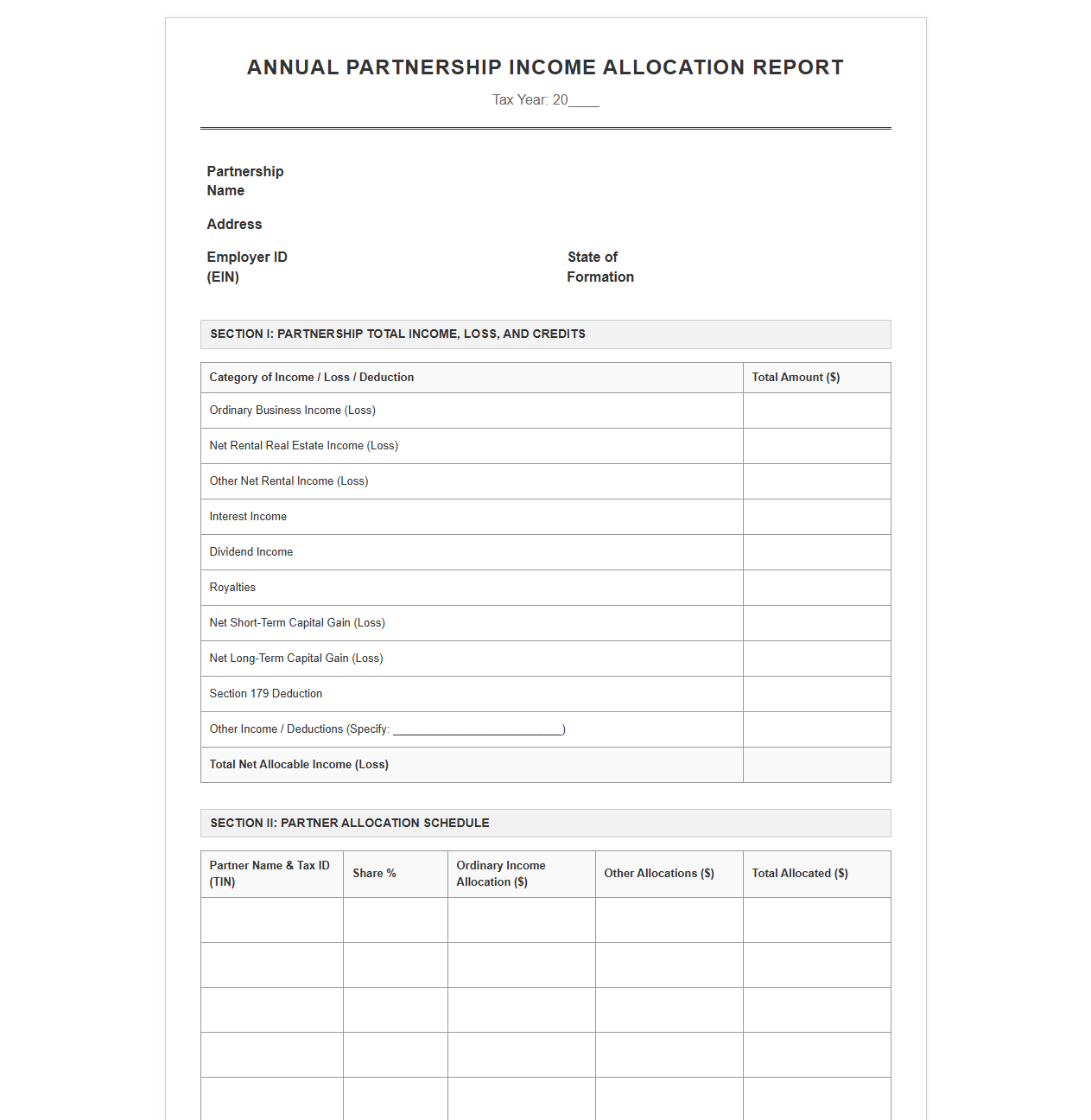

Annual Partnership Income Allocation Report

Download: .PDF

Download: .PDF

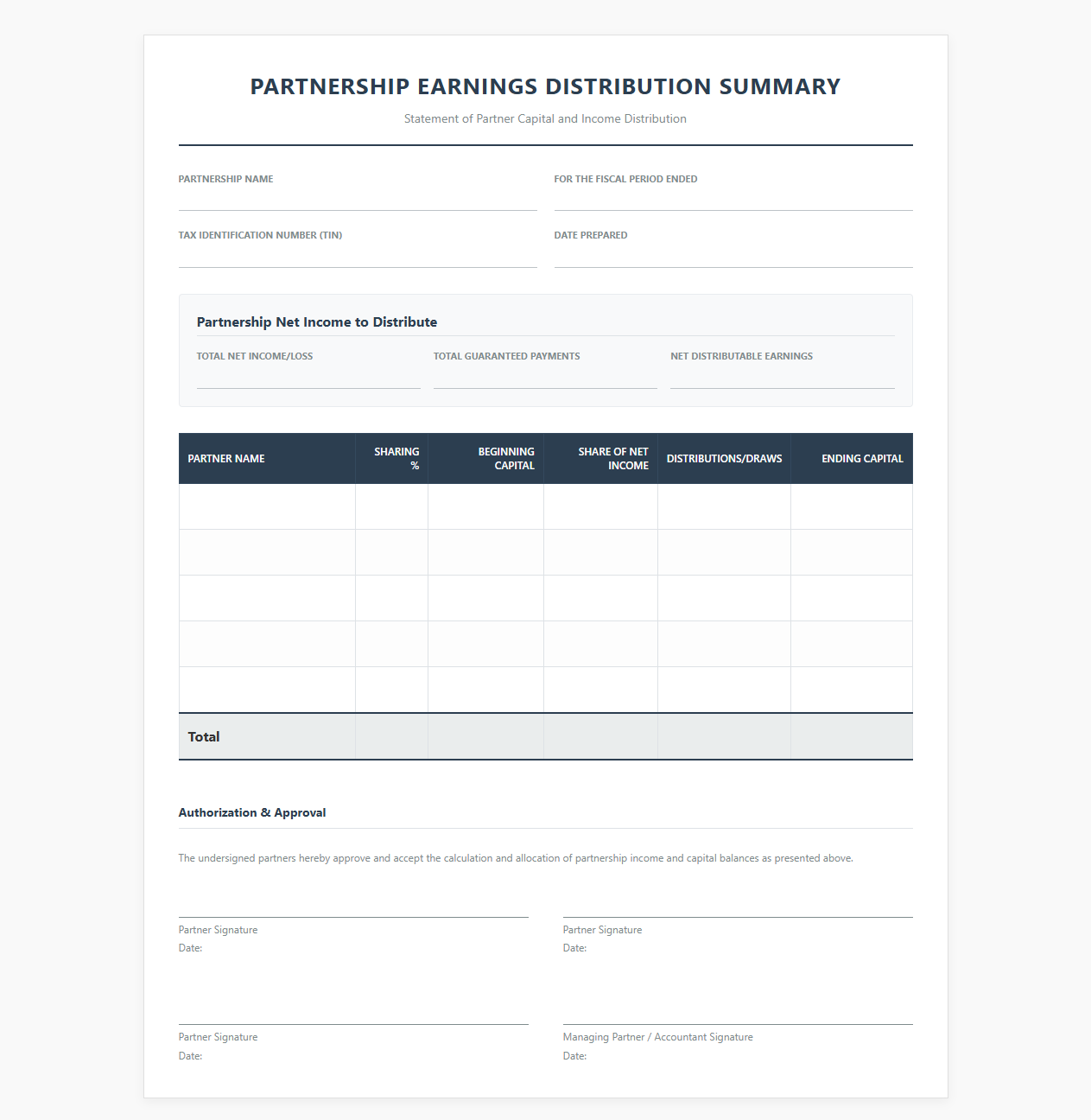

Partnership Earnings Distribution Summary Template

Download: .PDF

Download: .PDF

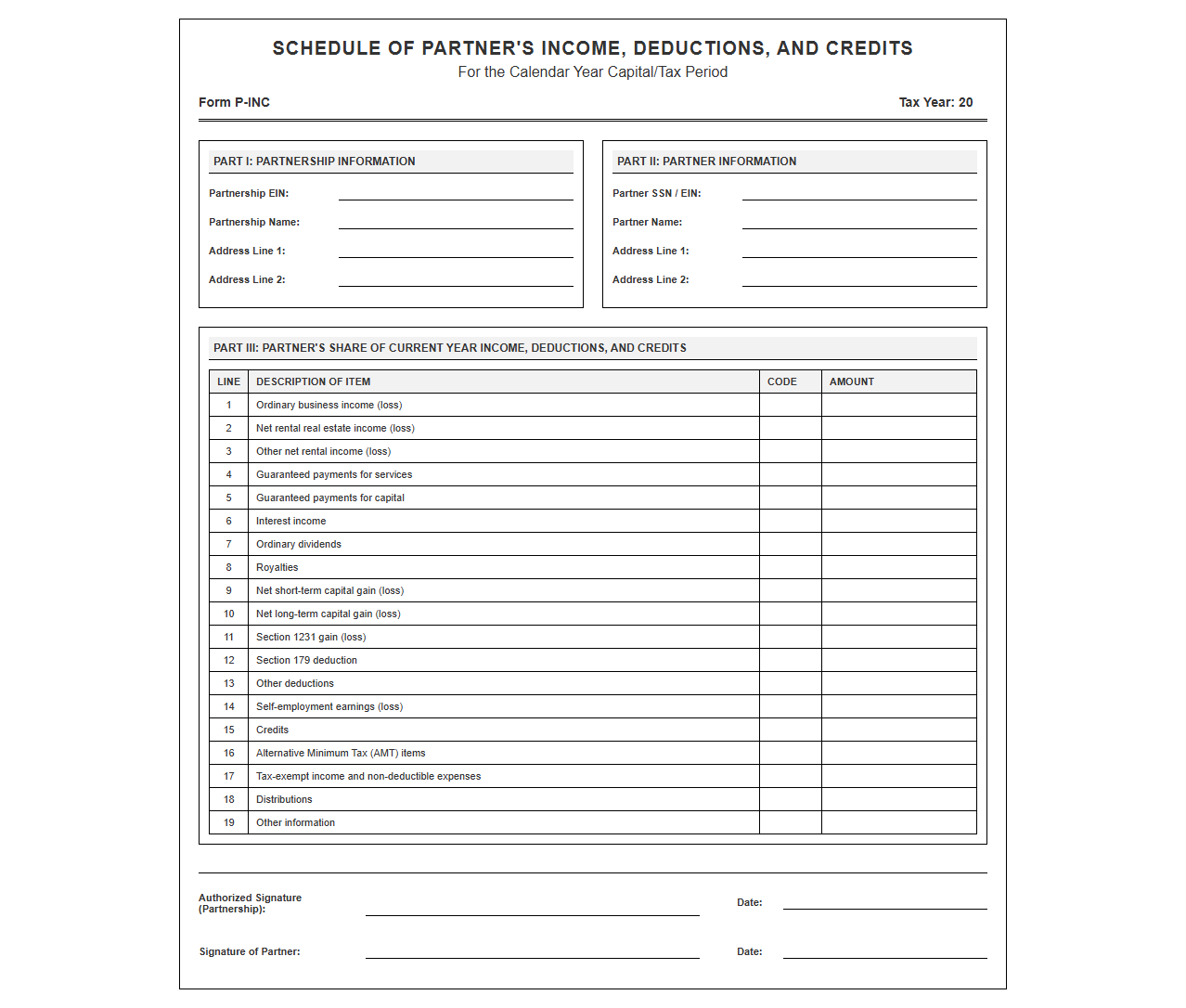

Schedule of Partner Income and Deductions

Download: .PDF

Download: .PDF

Partnership Taxable Income Statement Template

Download: .PDF

Download: .PDF

Introduction: The Complexity of Partnership Revenue Sharing

Navigating the financial dynamics of a partnership requires balancing growth objectives with individual expectations. Distributing revenue is not merely a task of dividing profits at the end of the year; it is a complex process shaped by varying capital contributions, individual performance metrics, and distinct operational roles. Without clear guidelines, financial distribution can easily become a major source of friction between co-owners.

Maintaining accurate financial reporting is critical for preserving organizational trust and ensuring compliance. When financial records are clear and transparent, partners can easily verify that their payouts align with agreed-upon terms. This transparency keeps everyone focused on strategic growth rather than financial disputes, securing the enterprise's long-term viability.

Key Elements of a Partnership Income Statement

Unlike a standard corporation or sole proprietorship, a partnership's income statement must adapt to show how earnings flow to multiple owners. The document must clearly demonstrate how profits transition from the company's bottom line to individual capital accounts.

Understanding these unique components is essential for clean book-keeping:

- Net Income Allocation: The formal division of the business's net profit or loss among the partners based on the partnership agreement.

- Partners' Drawings: Pre-arranged withdrawals of cash or assets made by partners against their expected share of profits, tracked separately from operational expenses.

- Capital Accounts: Individual equity accounts that track each partner's initial investment, share of retained profits, and total lifetime withdrawals.

Standard Revenue Distribution Methods Explained

Partnerships often deploy different formulas to split their yearly earnings. Choosing the right method depends on how much capital each partner contributes versus their daily operational involvement.

| Distribution Method | Primary Focus | Best Suited For |

|---|---|---|

| Fixed Ratios | Predetermined percentage split (e.g., 50/50 or 60/40) | Equal partners or simple, structured arrangements |

| Capital Percentage | Proportion of capital initially or currently invested | Capital-intensive businesses with silent investors |

| Interest on Capital Balances | Paying interest on invested capital before splitting remaining profits | Compensating partners who risk higher capital amounts |

Step-by-Step Guide to Calculating Partner Allocations

Let us walk through a practical calculation to show how a business divides a net income of $100,000 among three partners (Partner A, Partner B, and Partner C) using a combination of salary allowances and remaining fixed ratios.

- Calculate the total salary allowances allocated to partners first:

Partner A: $30,000andPartner B: $20,000. - Subtract the total salary allowances ($50,000) from the total net income ($100,000) to find the remaining profit:

$100,000 - $50,000 = $50,000. - Split the remaining $50,000 equally among all three partners (1/3 each):

$50,000 / 3 = $16,667 per partner. - Add each partner's salary allowance to their share of the remaining profit to find their final allocation:

Partner A: $46,667,Partner B: $36,667, andPartner C: $16,666.

Essential Income Statement Templates for Partnerships

To accurately capture these multi-partner distributions, your financial reporting needs structured, customizable templates. A well-designed partnership income statement separates operational performance from the allocation of net income.

The core statement tracks traditional business metrics, listing total revenue, cost of goods sold, and operating expenses. This leads to the net income figure, which acts as the starting point for the allocation schedule.

Common Pitfalls in Partnership Reporting and How to Avoid Them

Inconsistent accounting practices can quickly lead to costly disputes and compliance issues. One of the most common errors is mischaracterizing partner transactions, which can result in incorrect tax filings and skewed equity balances.

"Failing to track fluctuations in partner capital accounts throughout the fiscal year is a primary driver of partnership disputes during tax season."

To avoid these errors, always record draw accounts separately from business expenses. Treat partner salary allocations as equity distributions rather than operational expenses unless they are formally designated as guaranteed payments. Maintaining this distinction ensures clean tax reporting and accurate financial statements.

Best Practices for Long-Term Financial Harmony

Proactive communication and structured processes are the true keys to preventing financial friction. Partners must commit to clear, recurring routines to ensure everyone remains aligned as the business evolves.

Schedule comprehensive quarterly financial reviews to walk through capital accounts, drawing balances, and distribution schedules together. This keeps expectations realistic and surfaces discrepancies early.

Update the partnership agreement whenever there is a shift in roles, capital contributions, or operational expectations. A legal document should always reflect the current operational reality of the business.

Utilize specialized, automated accounting software that supports multi-partner ledger tracking. Automating calculations minimizes human error, ensures real-time visibility, and maintains a clean audit trail for all parties involved.

Leave a comment