Discovering a discrepancy in past payroll records or historical financial statements is a highly stressful ordeal that can quickly disrupt business operations. Before addressing these errors, however, organizations must establish a rigorous auditing workflow to trace the exact origin of the mismatch. Standardizing this diagnostic phase with structured templates grants financial teams the immediate clarity and efficiency needed to secure swift, compliant resolutions.

Please note: While standardized templates streamline the correction process, they function as organizational aids rather than a replacement for certified CPA oversight. For instance, when rectifying a retroactive pay adjustment or resolving a miscalculated Q3 tax contribution, precise data entry is paramount, and templates ensure no critical variables are overlooked.

This article will guide you through the process of using prior period earnings statement templates to isolate historical errors, maintain regulatory compliance, and fortify your ongoing payroll reporting workflows.

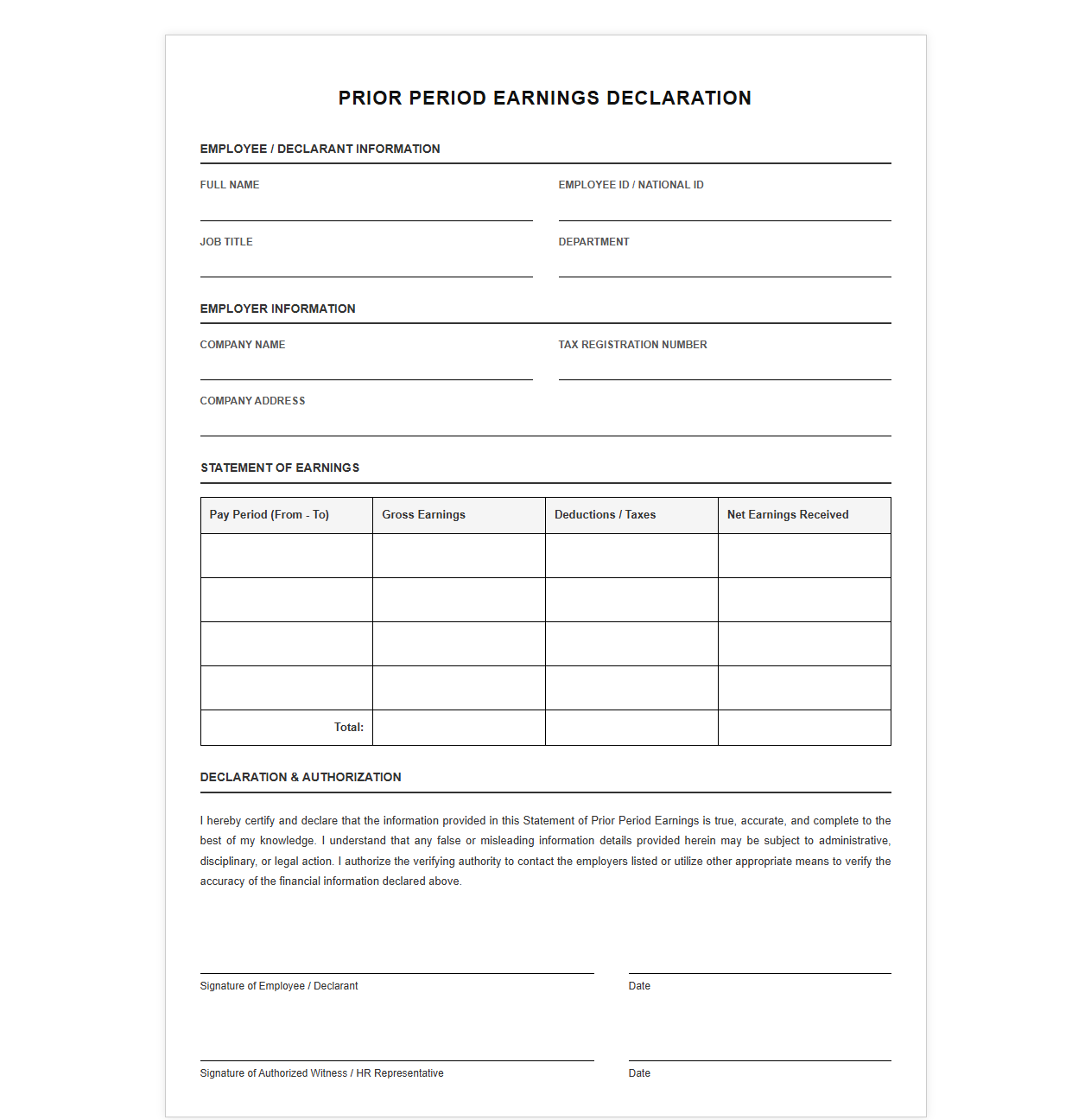

Prior Period Earnings Declaration Template

Download: .PDF

Download: .PDF

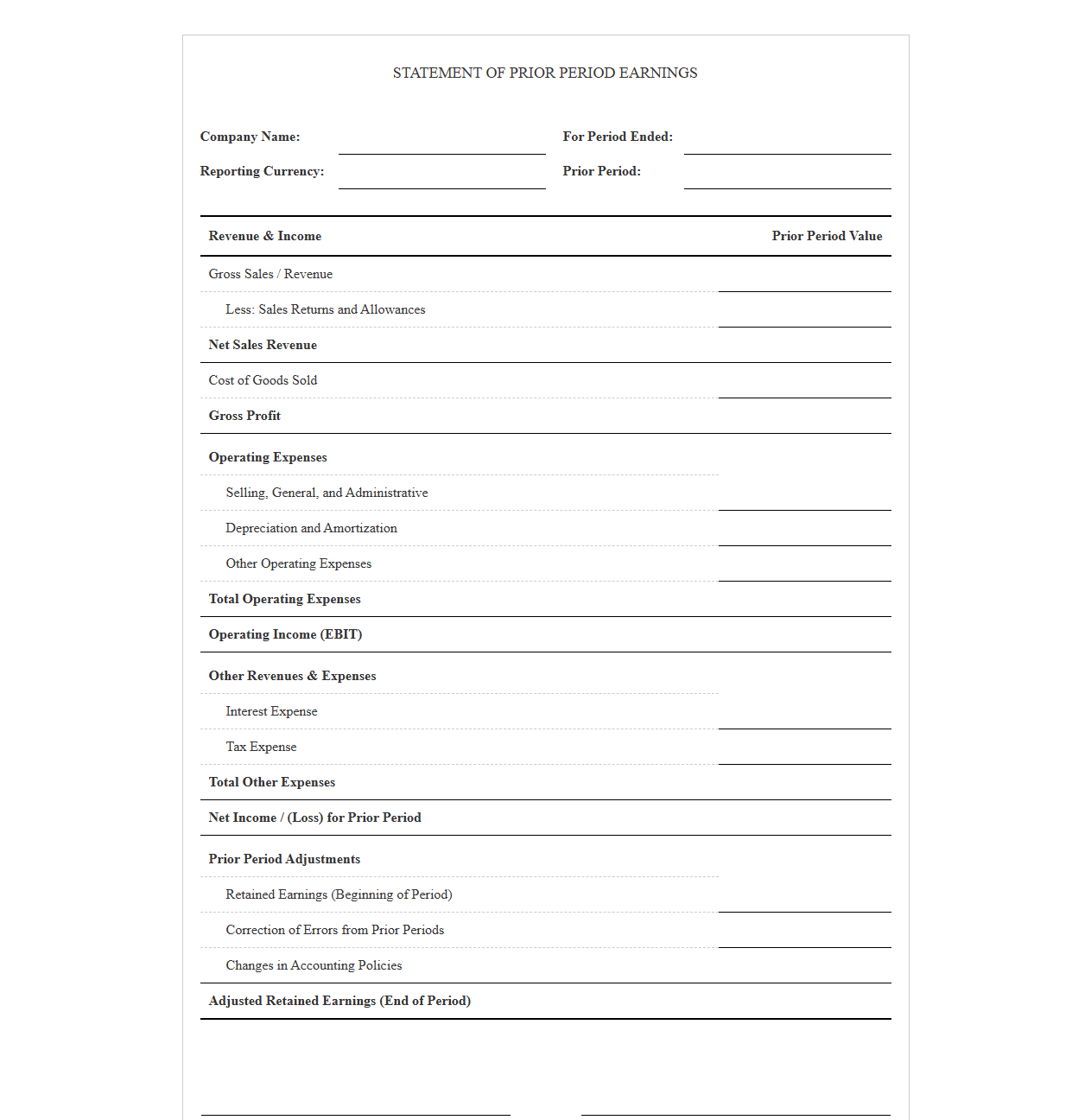

Previous Period Income Statement Form

Download: .PDF

Download: .PDF

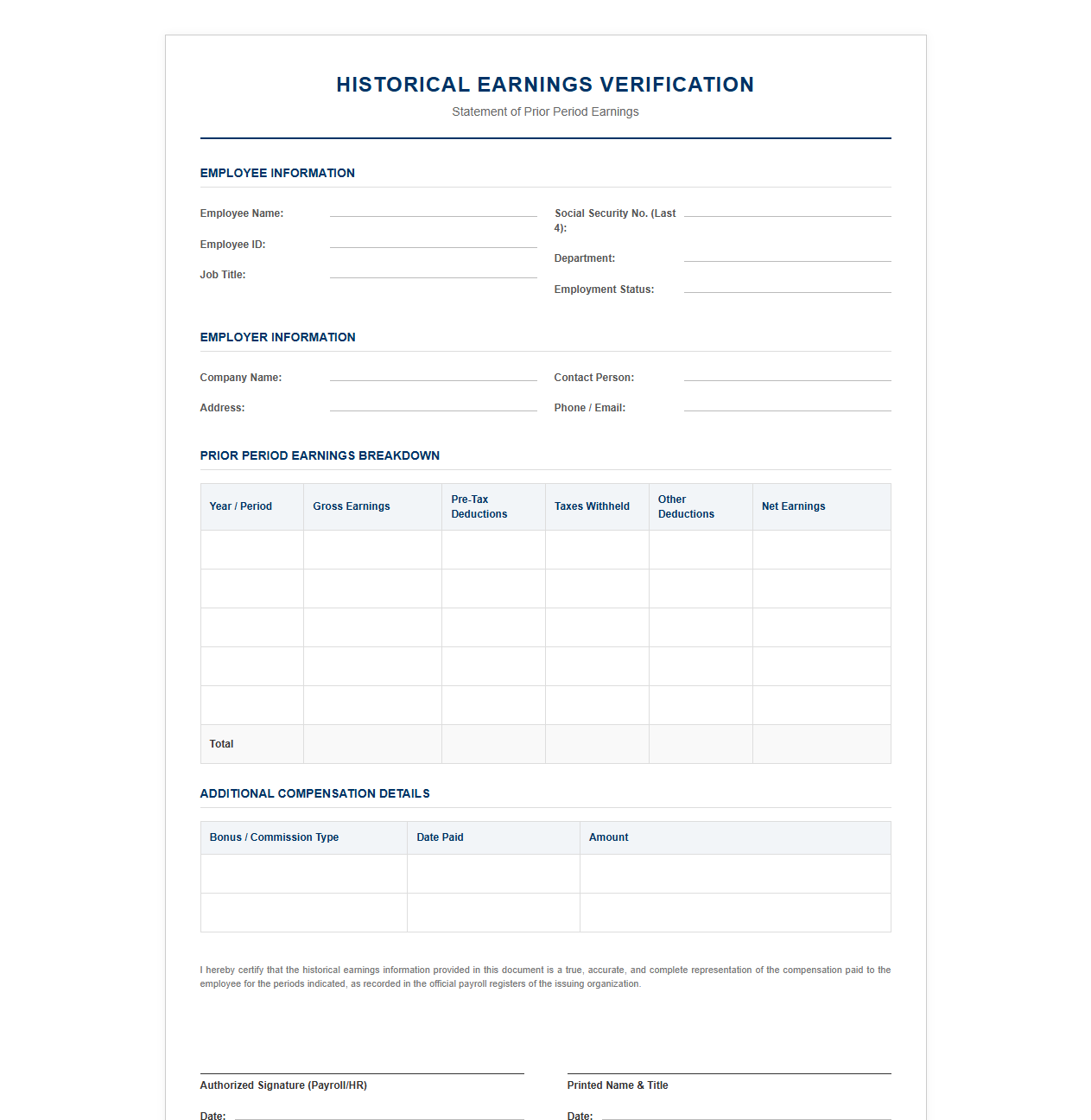

Historical Earnings Verification Document Template

Download: .PDF

Download: .PDF

Prior Financial Period Earnings Report Template

Download: .PDF

Download: .PDF

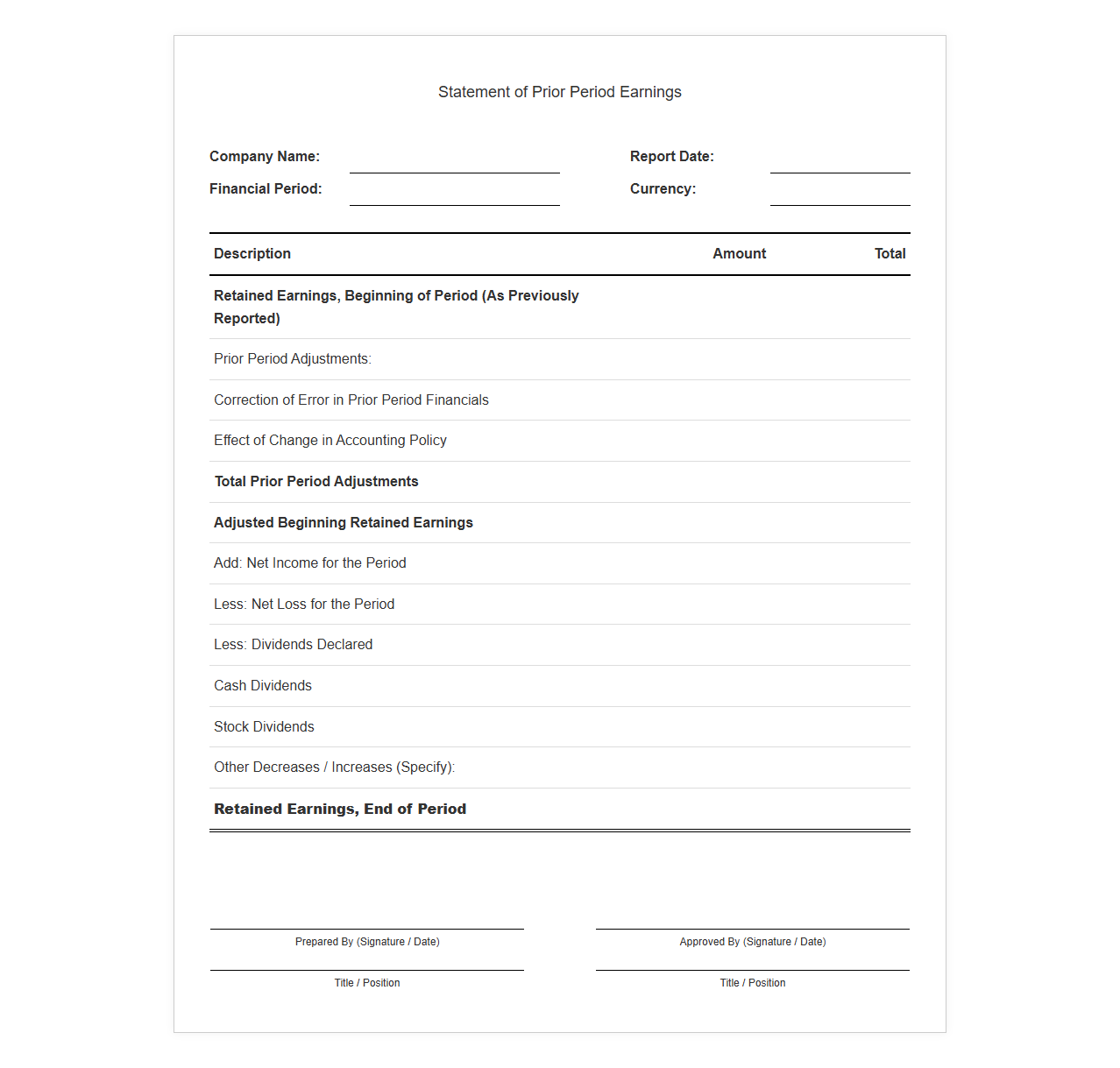

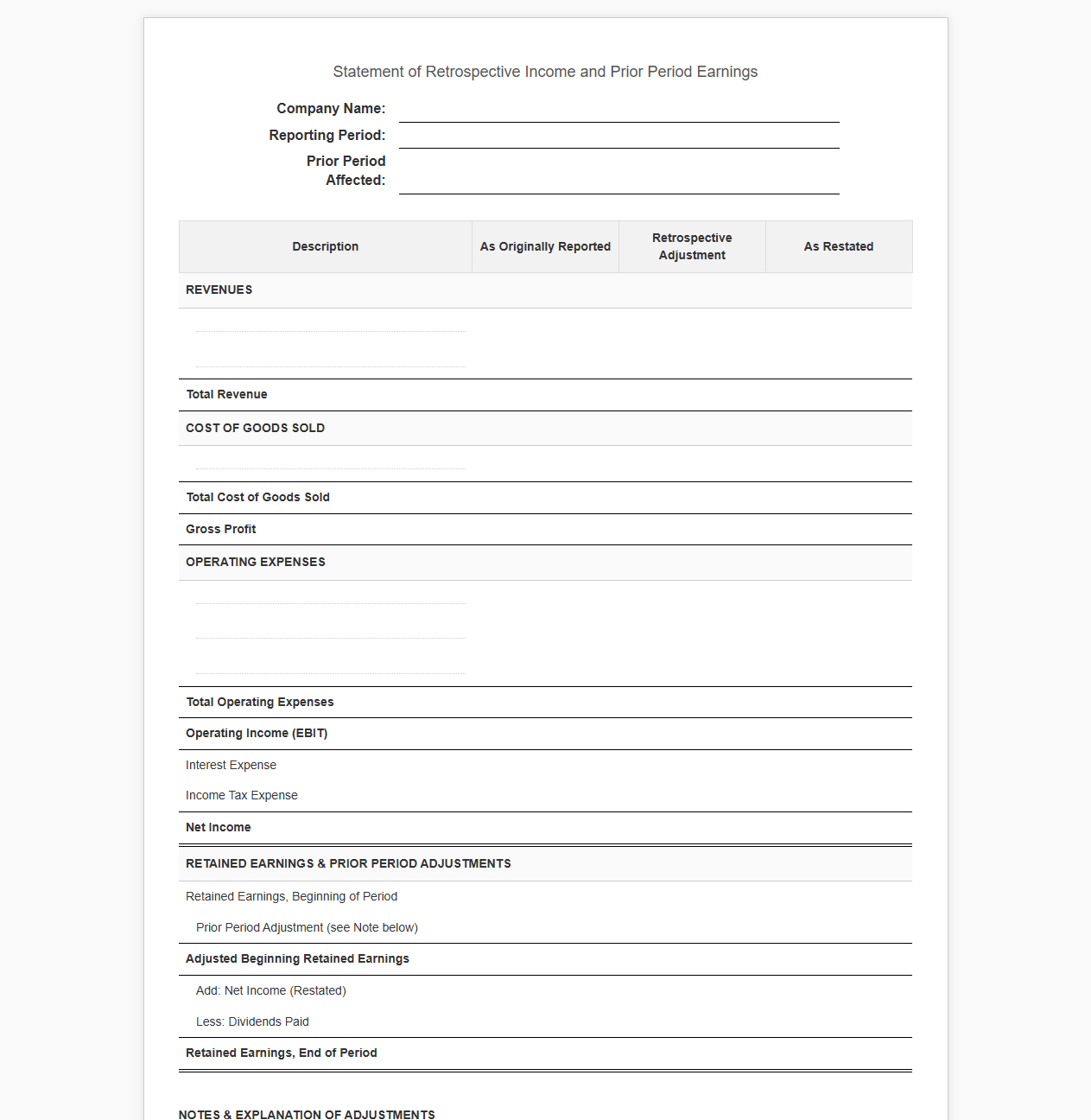

Retrospective Income Statement Template

Download: .PDF

Download: .PDF

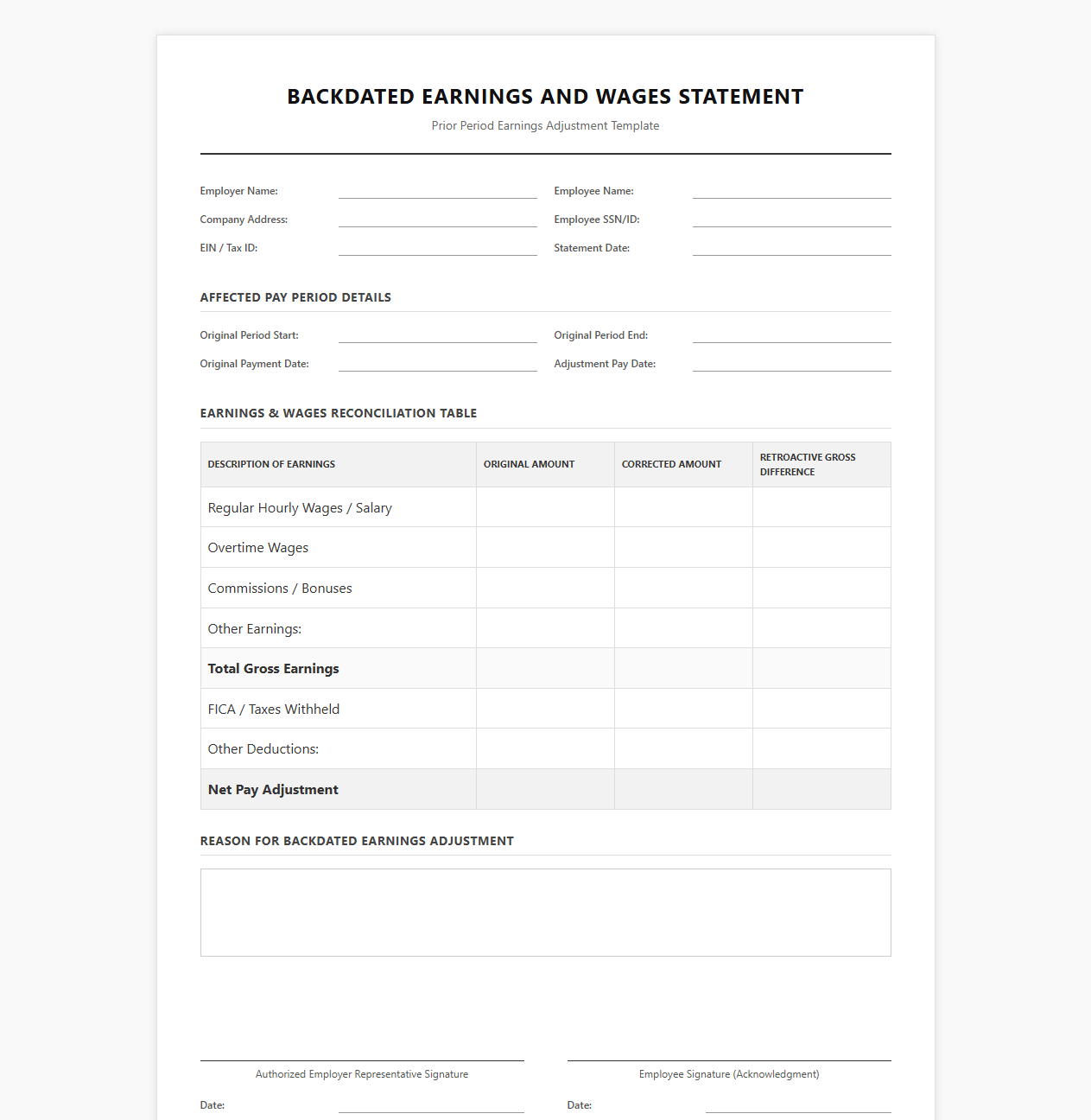

Backdated Earnings and Wages Statement Template

Download: .PDF

Download: .PDF

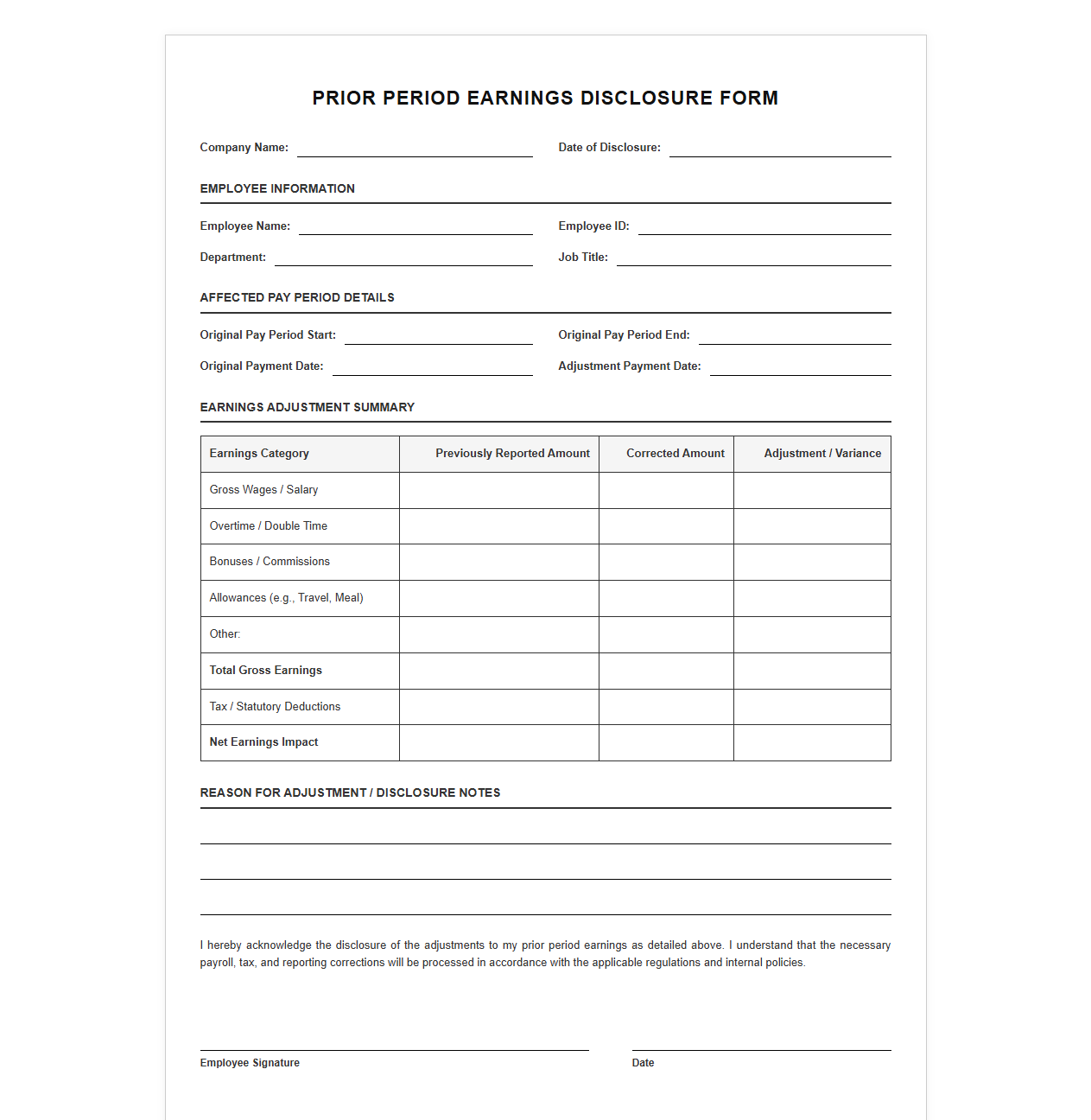

Past Period Earnings Disclosure Form

Download: .PDF

Download: .PDF

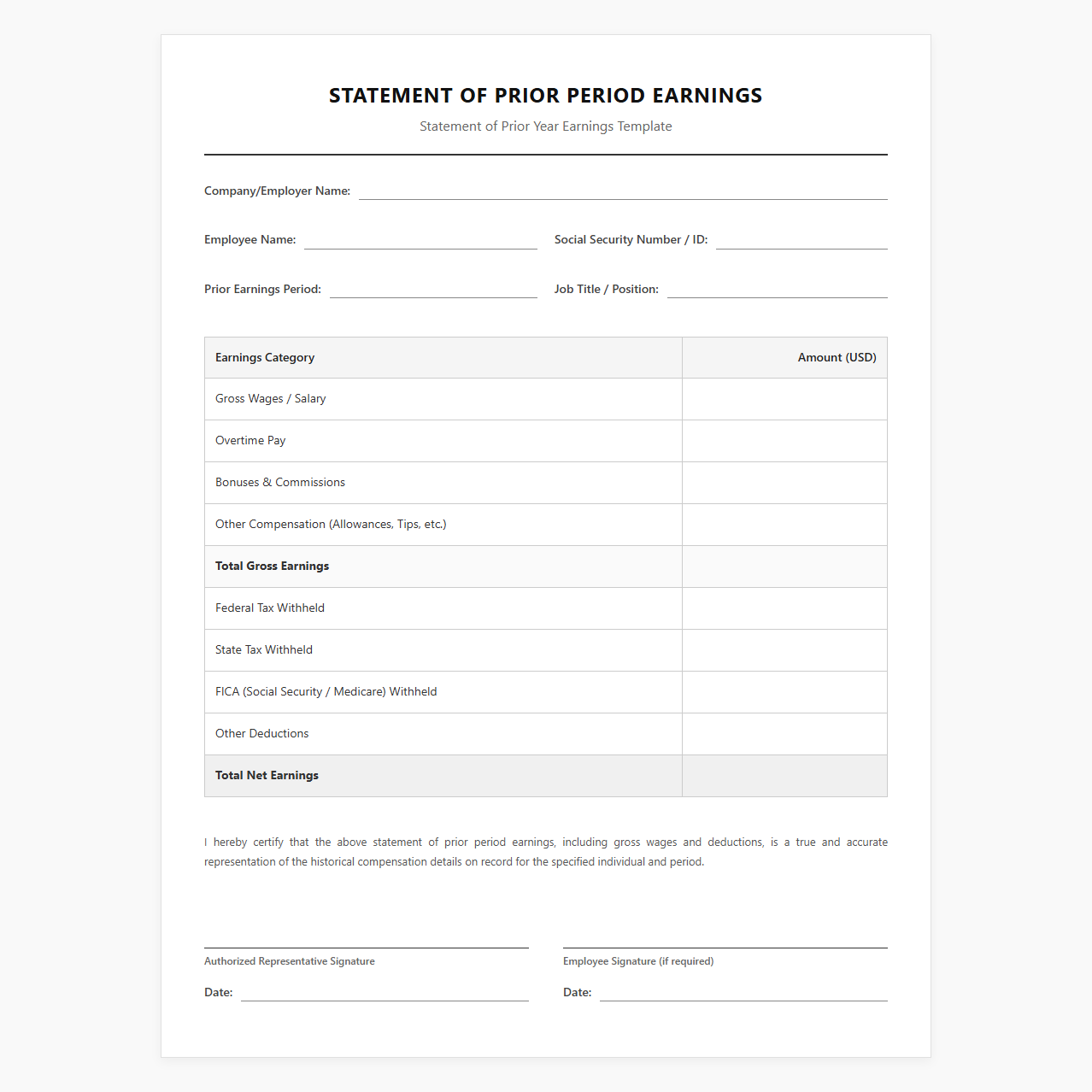

Statement of Prior Year Earnings Template

Download: .PDF

Download: .PDF

Understanding Financial Discrepancies in Historical Accounts

Financial discrepancies in past earnings reports often emerge from overnight processing delays, late-arriving invoices, or shifting regulatory interpretations. When these errors remain unaddressed, they distort the true financial health of an organization. Correcting these anomalies is not merely a technical necessity; it is a critical step to maintain organizational credibility with stakeholders, investors, and regulatory bodies who rely on precise historical data for decision-making.

The Strategic Value of Prior Period Earnings Templates

A prior period earnings statement template is a structured framework designed to log, analyze, and adjust historical financial data. By providing a uniform layout, these templates standardize the reconciliation process across accounting teams. This consistency ensures that every correction follows the same mathematical logic, reducing human error and accelerating the preparation of restated financials.

Identifying the Root Causes of Statement Inconsistencies

Historical accounting errors rarely occur in a vacuum. Most discrepancies can be traced back to systemic workflow issues or manual mistakes during the closing cycle:

- Transaction timing mismatches, where revenue or expenses are recognized in the incorrect fiscal period.

- Manual data entry oversights, including transposing numbers or misclassifying accounts.

- Misinterpretation of evolving accounting standards or depreciation schedules.

Selecting the Right Template for Your Financial Framework

Choosing the correct reconciliation template requires a deep understanding of your regulatory environment. Organizations must ensure their templates align with either GAAP or IFRS requirements, depending on their jurisdiction. For comprehensive guidance on selecting frameworks that match your operational complexity, you can review established financial compliance resources on the FASB official portal.

A Step-by-Step Process for Executing the Correction

To ensure a precise adjustment, accounting teams should follow a highly structured, chronological workflow when executing historical corrections:

- Import the original historical financial data into the standardized template.

- Identify and isolate the specific ledger entries requiring adjustment.

- Apply the corrected figures within the designated template cells to automatically recalculate balances.

- Verify that the adjusted ledger balances perfectly against original source documents.

Ensuring Regulatory Compliance and Audit Readiness

Adjusting prior period earnings carries significant legal and tax implications. Regulatory bodies require companies to be fully transparent about why a restatement occurred, which is achieved through comprehensive footnotes and disclosures in the revised financial reports.

"All material corrections to prior period financial statements must be accompanied by clear disclosures detailing the nature of the error and the impact on previously reported net income." - Financial Accounting Standards Board (FASB)

Implementing Controls to Prevent Future Discrepancies

Securing the integrity of future financial reporting requires a proactive approach. Organizations must transition from reactive correction to active prevention by strengthening internal control frameworks. Leveraging accounting automation software minimizes human data entry errors, while establishing routine, independent audits ensures that minor discrepancies are caught and resolved before they escalate into systemic reporting issues.

Leave a comment