Navigating an IRS tax dispute is notoriously stressful, often leaving tax practitioners overwhelmed by administrative overhead and client management. Before even addressing the tax authorities, professionals must establish a clear, legally sound framework with their clients to avoid scope creep and administrative disputes.

Implementing robust representation agreement templates grants practitioners immediate liability protection and fosters client trust through absolute transparency. However, as a critical stipulation, these documents must strictly adhere to IRS Circular 230 regulations to ensure compliance. Relying on concrete examples, such as structured Fee Agreements and customized Form 2848 authorization addenda, serves as proof of professional diligence and protects your practice.

In this article, we will explore the indispensable agreement templates required for IRS representation, how to customize them for maximum efficacy, and best practices for securing seamless client compliance.

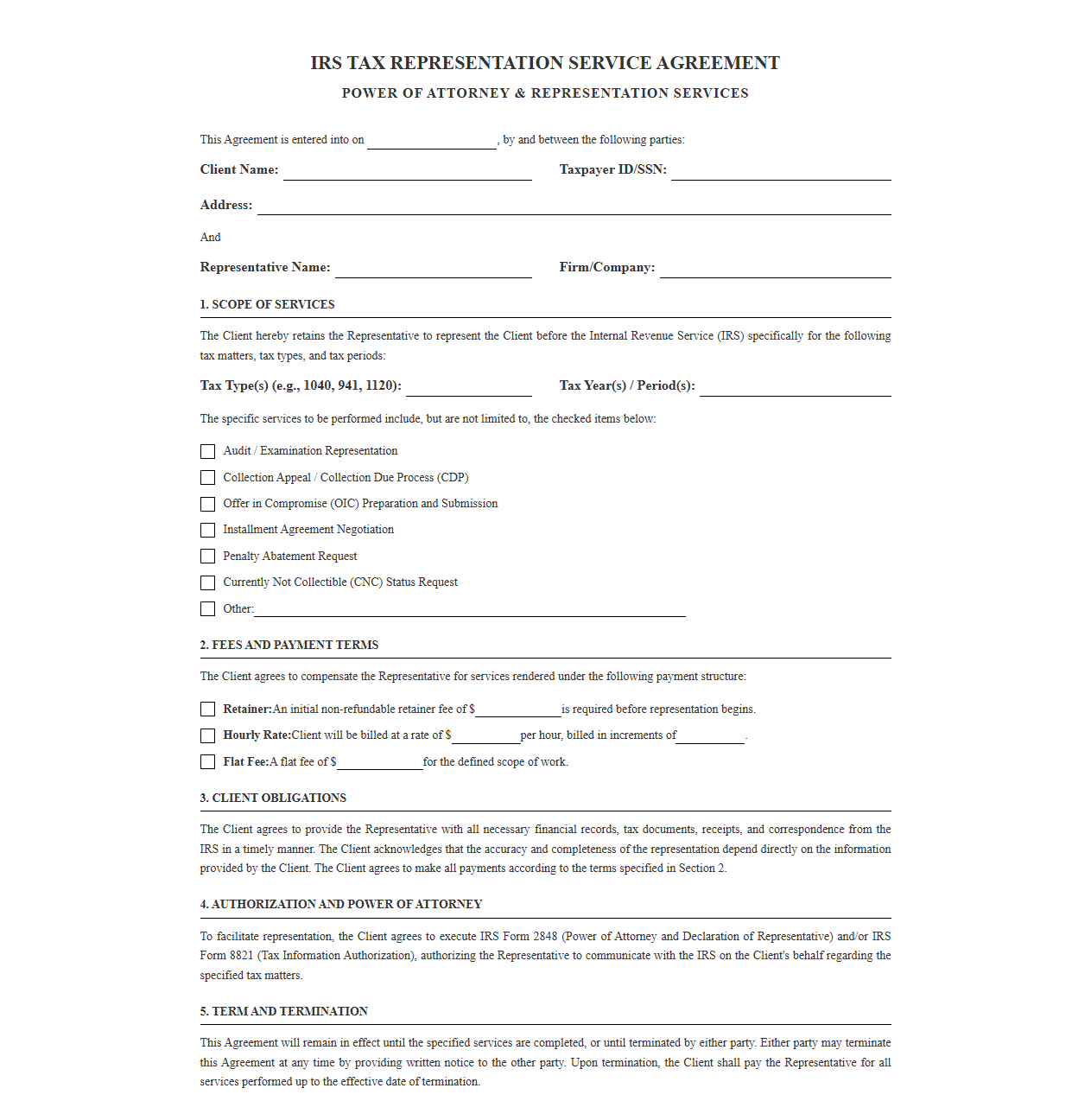

IRS Tax Representation Service Agreement Form

Download: .PDF

Download: .PDF

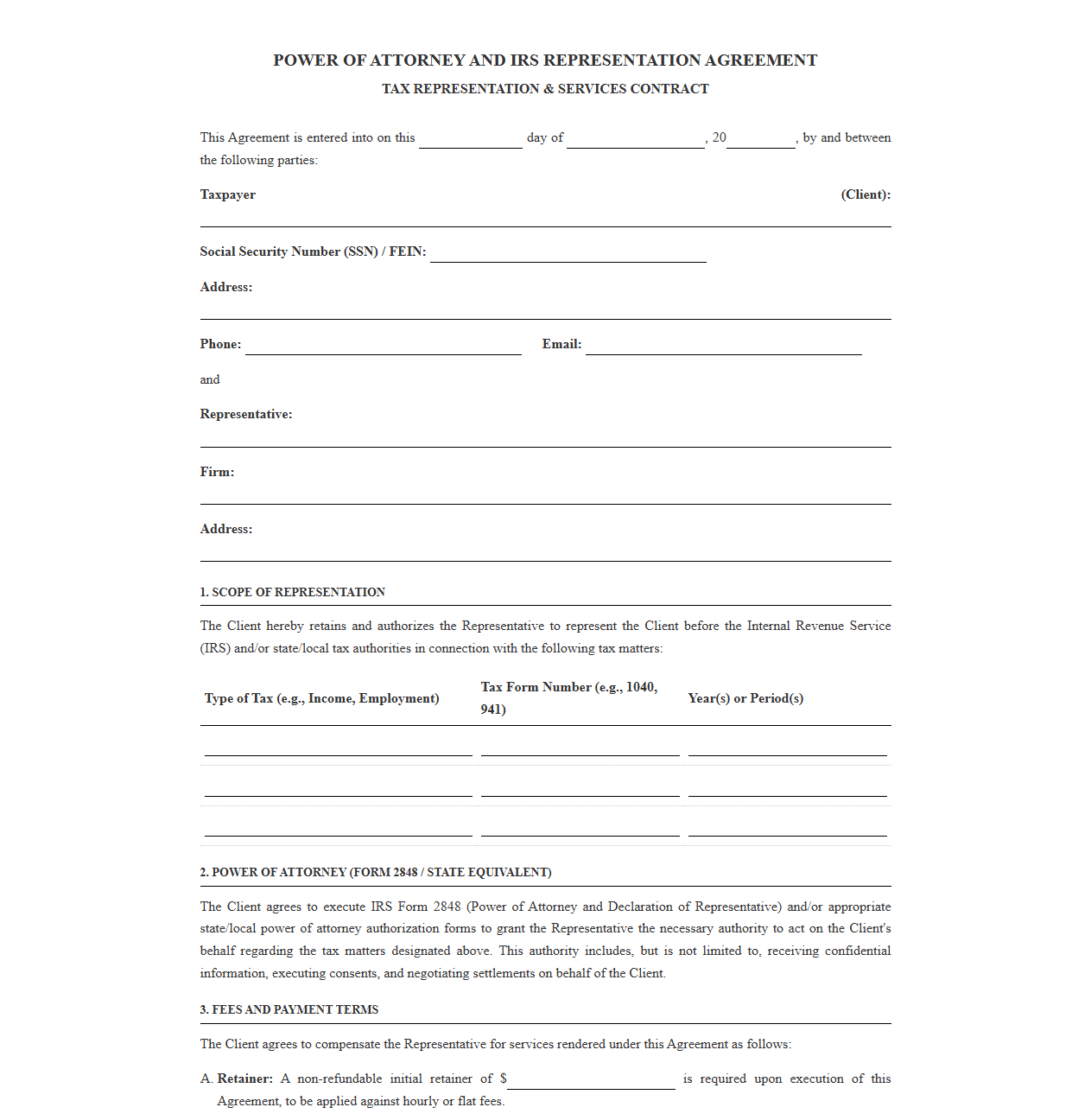

Power of Attorney and IRS Representation Contract

Download: .PDF

Download: .PDF

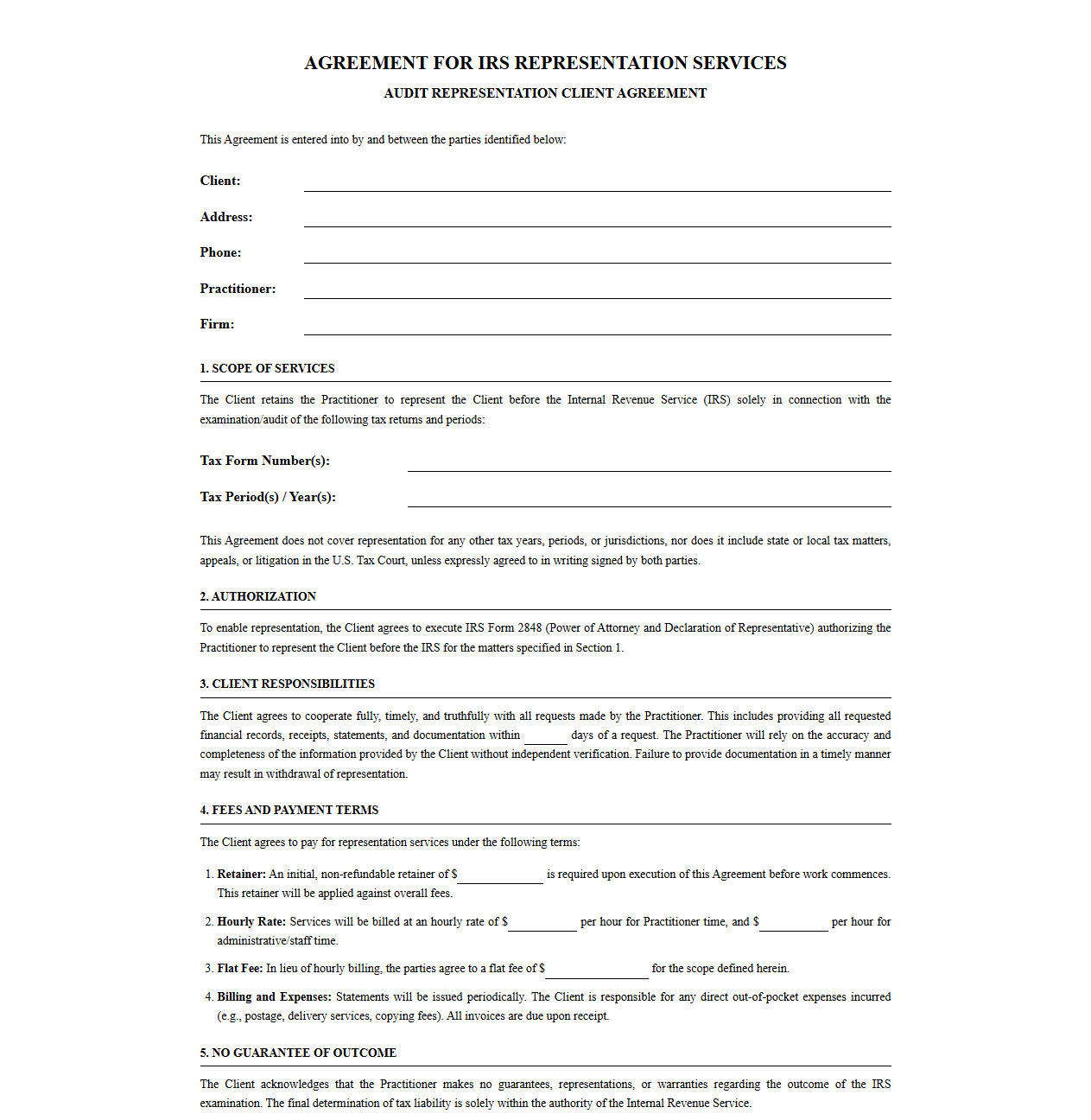

IRS Audit Representation Client Agreement

Download: .PDF

Download: .PDF

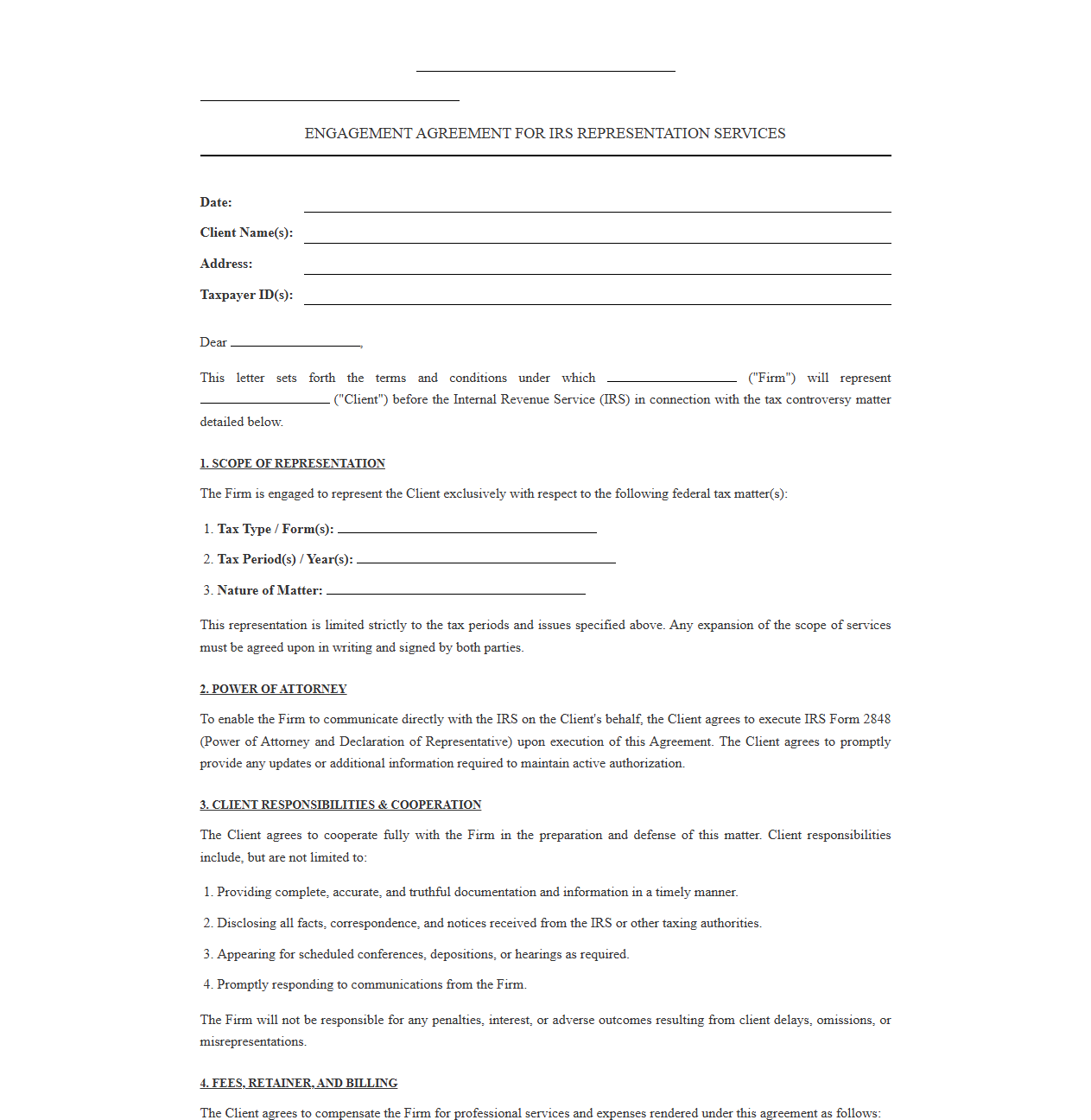

Tax Controversy Representation Engagement Letter

Download: .PDF

Download: .PDF

Professional IRS Representation Services Contract

Download: .PDF

Download: .PDF

Agreement for IRS Tax Relief Representation

Download: .PDF

Download: .PDF

IRS Practice and Representation Service Agreement

Download: .PDF

Download: .PDF

Taxpayer Representation Services Engagement Agreement

Download: .PDF

Download: .PDF

IRS Representation and Tax Advocacy Agreement

Download: .PDF

Download: .PDF

Introduction to Tax Representation Agreements

Navigating the complexities of IRS audits, appeals, or collection matters requires a highly structured professional relationship. A formal tax representation agreement serves as the foundational bedrock for this partnership, establishing legal clarity and mutual expectations from the very beginning. Without a written contract, both the practitioner and the taxpayer risk severe misunderstandings regarding the depth of the representation and the boundaries of responsibilities. Utilizing a well-drafted template ensures that all regulatory standards are met while protecting both parties throughout the dispute resolution process.

Defining the Scope of IRS Representation

One of the most critical aspects of a tax representation agreement is clearly establishing the boundaries of the engagement. Practitioners must explicitly state which tax forms, specific tax periods, and exact jurisdictions they are authorized to handle to prevent scope creep.

- The filing and execution of Form 2848 (Power of Attorney and Declaration of Representative) to formally communicate with the IRS.

- The precise tax years under examination or dispute, such as individual income taxes for the years 2021 through 2023.

- The specific IRS departments or divisions involved, such as the Office of Appeals or the Automated Underreporter unit.

- Exclusions of service, clarifying that state tax audits or subsequent litigation in Tax Court require a separate agreement.

Essential Retainer and Fee Structure Templates

Establishing a transparent financial arrangement prevents billing disputes and fosters trust. Practitioners commonly use different pricing models depending on the complexity of the case, and these must be detailed explicitly in the engagement letter.

- Hourly Rate Structures: Billing based on the actual time spent on the case, requiring meticulous log tracking and periodic updates to the client.

- Flat Fee Arrangements: A fixed sum for a defined scope of work, providing predictable costs for the client but requiring strict boundaries on what is included.

- Retainer Terms: An upfront deposit held in a trust account, which is drawn down as work is performed and must be replenished as specified.

Clear terms regarding billing cycles, late fees, and non-payment consequences ensure a smooth financial workflow.

Client Responsibilities and Truthfulness Clauses

A successful defense before the IRS relies entirely on the accuracy and completeness of the financial records provided by the taxpayer. The client must understand their legal and professional duty to be fully transparent with their representative.

The client is solely responsible for the truthfulness, accuracy, and completeness of all financial records, tax returns, and statements provided to the practitioner.

Withholding critical information or presenting falsified documents can lead to immediate withdrawal by the practitioner. Failure to disclose key tax liabilities or hidden assets can result in severe penalties from the IRS and compromises the representative's ability to advocate effectively.

Privacy, Confidentiality, and Privilege Protection

Taxpayers must feel secure knowing their highly sensitive financial data is protected by strict confidentiality standards. A robust privacy clause outlines how personal identifiable information is safeguarded and defines the exact limits of the practitioner-client privilege.

While IRC Section 7525 extends a limited confidentiality privilege to federally authorized tax practitioners, clients must understand that this protection does not apply to criminal tax matters or state tax issues. Maintaining absolute confidentiality on all non-privileged communication remains a core ethical duty of the practitioner, ensuring that sensitive data is never disclosed to unauthorized third parties without express written consent.

Termination of Services and Dispute Resolution

A clear exit strategy protects both parties if the professional relationship must end prematurely. The agreement must explicitly detail how termination is triggered, how outstanding fees are handled, and how disagreements are resolved.

- Termination Notice: Either party may terminate the representation upon written notice, subject to ethical guidelines and IRS rules.

- Outstanding Balances: Upon termination, the client remains responsible for paying all accrued fees and expenses incurred up to the termination date.

- Dispute Resolution: Any disputes arising from the agreement will first be subject to mediation, and if unresolved, settled through binding arbitration.

Finalizing and Executing the Engagement Letter

The final step in establishing the professional relationship is the proper execution of the engagement letter. Once both the practitioner and the client have reviewed all clauses, securing legally binding digital signatures ensures compliance and immediate commencement of work.

After execution, archiving the document securely in a document management system is vital. This establishes a clear chronological record that can be referenced during the representation. Properly executing this document formalizes your authority and allows you to submit the necessary authorization forms to the IRS, confidently moving forward with the taxpayer's defense.

Leave a comment