Receiving an IRS Form 668-W can throw any payroll department into sudden chaos, sparking immediate anxiety over tight compliance windows and the high-stakes pressure of calculating exempt wages accurately. Before addressing these calculations, employers must first understand the broader legal framework of federal tax levies and how they fundamentally alter standard payroll workflows.

Utilizing standardized payroll document templates grants your organization the operational efficiency needed to execute these withholding orders flawlessly, protecting you from costly non-compliance penalties. However, as a crucial educational stipulation, these templates must always be paired with up-to-date IRS exemption tables to remain valid.

For example, leveraging a dedicated template for Form 668-W Part 3 (the employee's Statement of Exemptions) ensures you gather the necessary filing status details without delay. In this article, we will examine the essential templates, step-by-step calculation workflows, and compliance checklists required to confidently resolve federal tax levies.

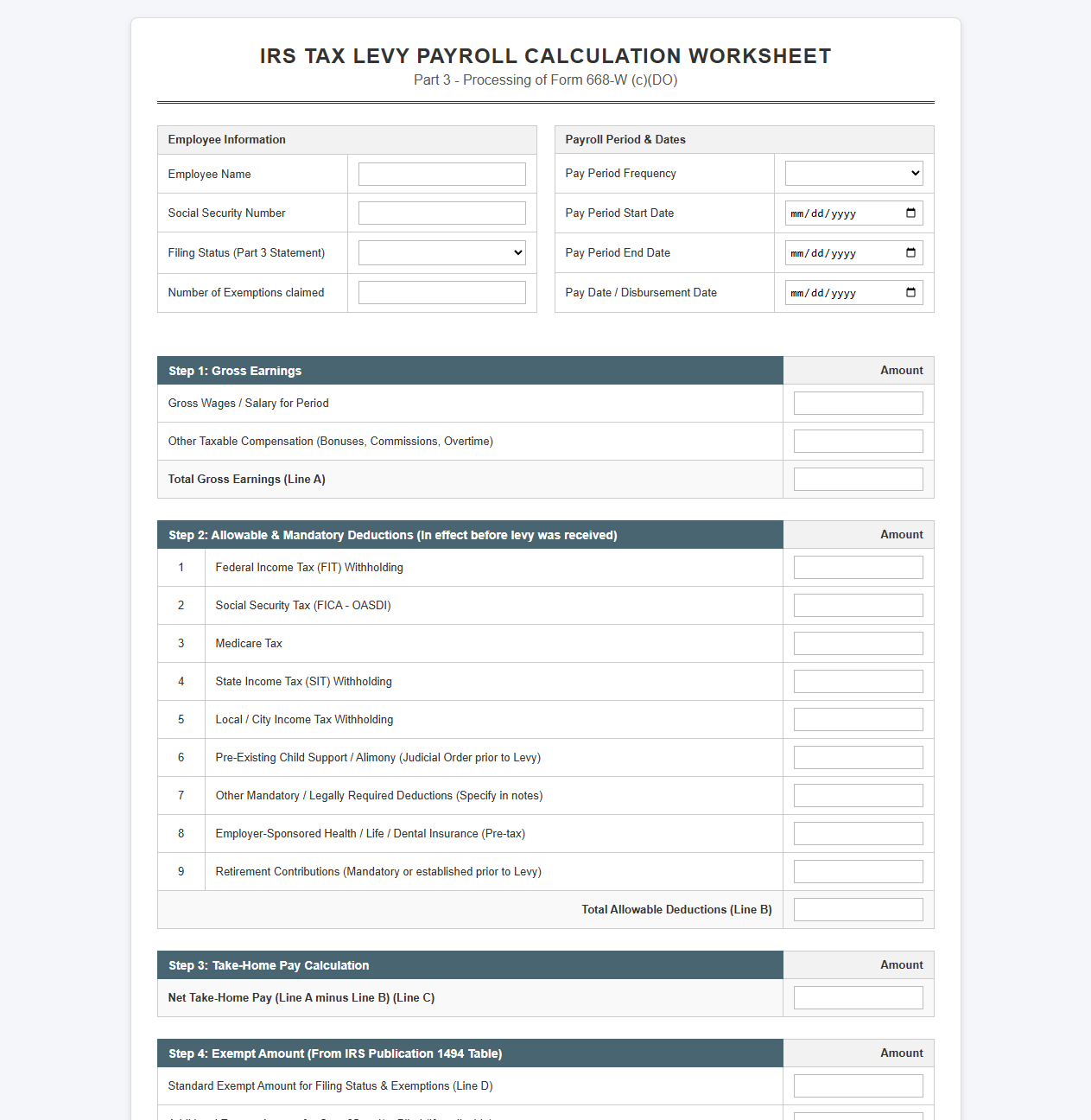

IRS Tax Levy Payroll Calculation Spreadsheet

Download: .PDF

Download: .PDF

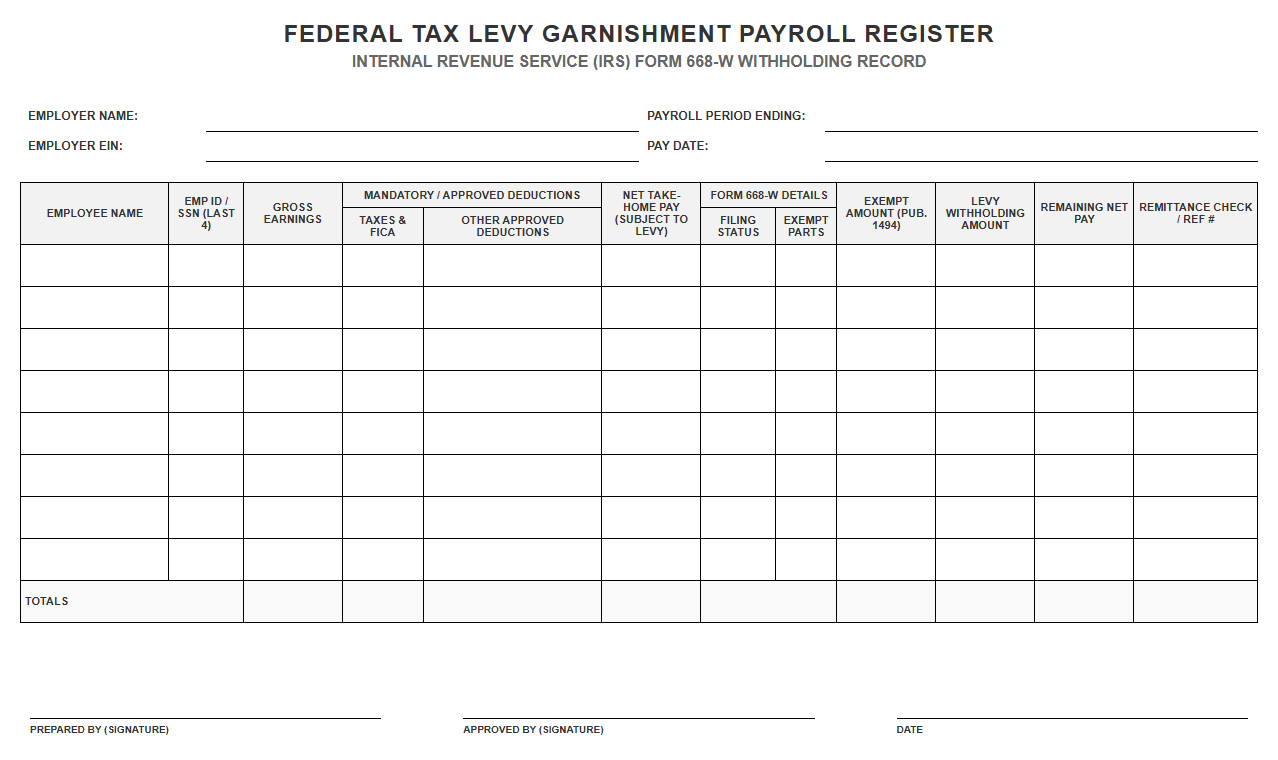

Federal Tax Levy Garnishment Payroll Register

Download: .PDF

Download: .PDF

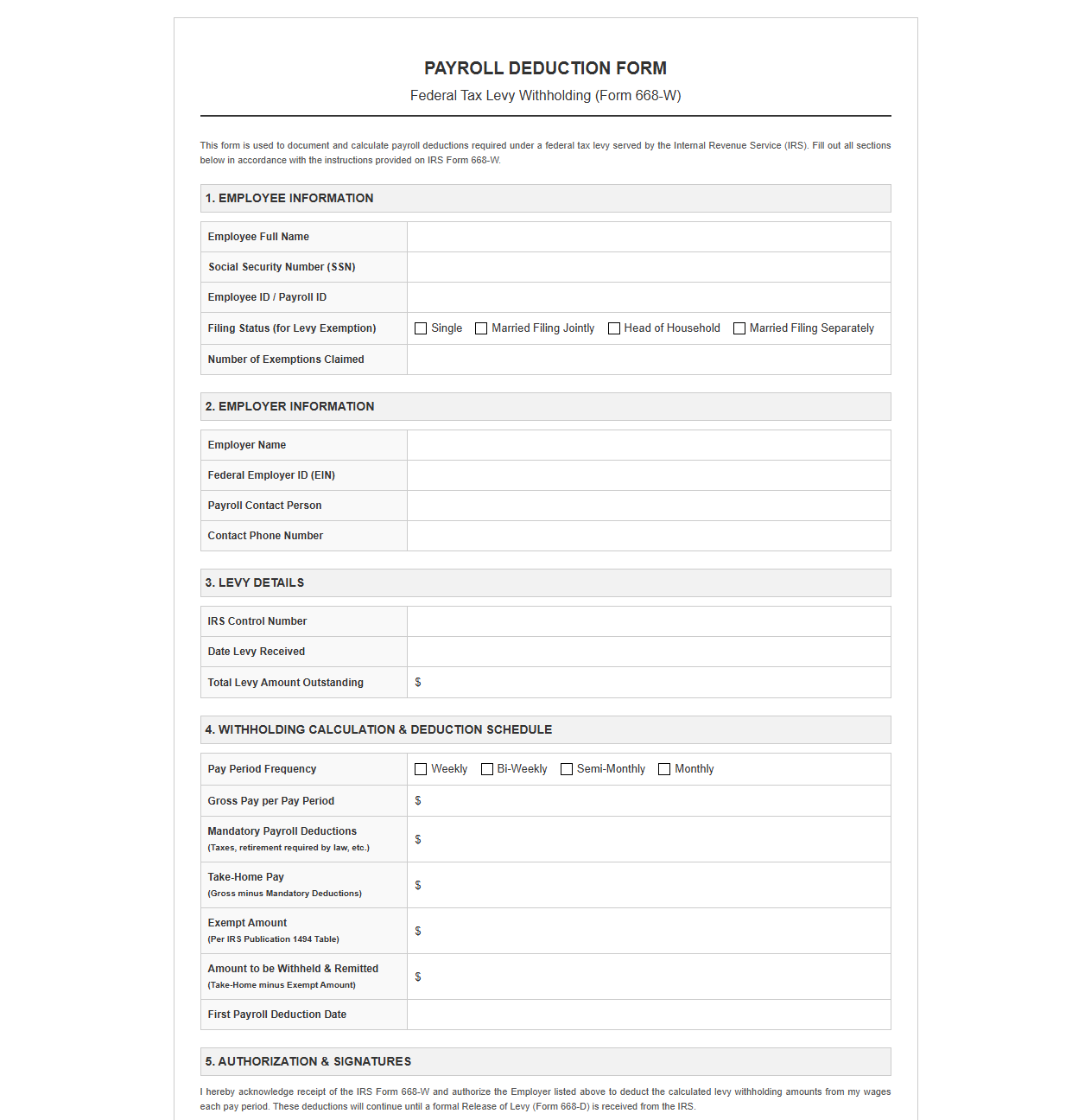

Payroll Deduction Form for Federal Tax Levy

Download: .PDF

Download: .PDF

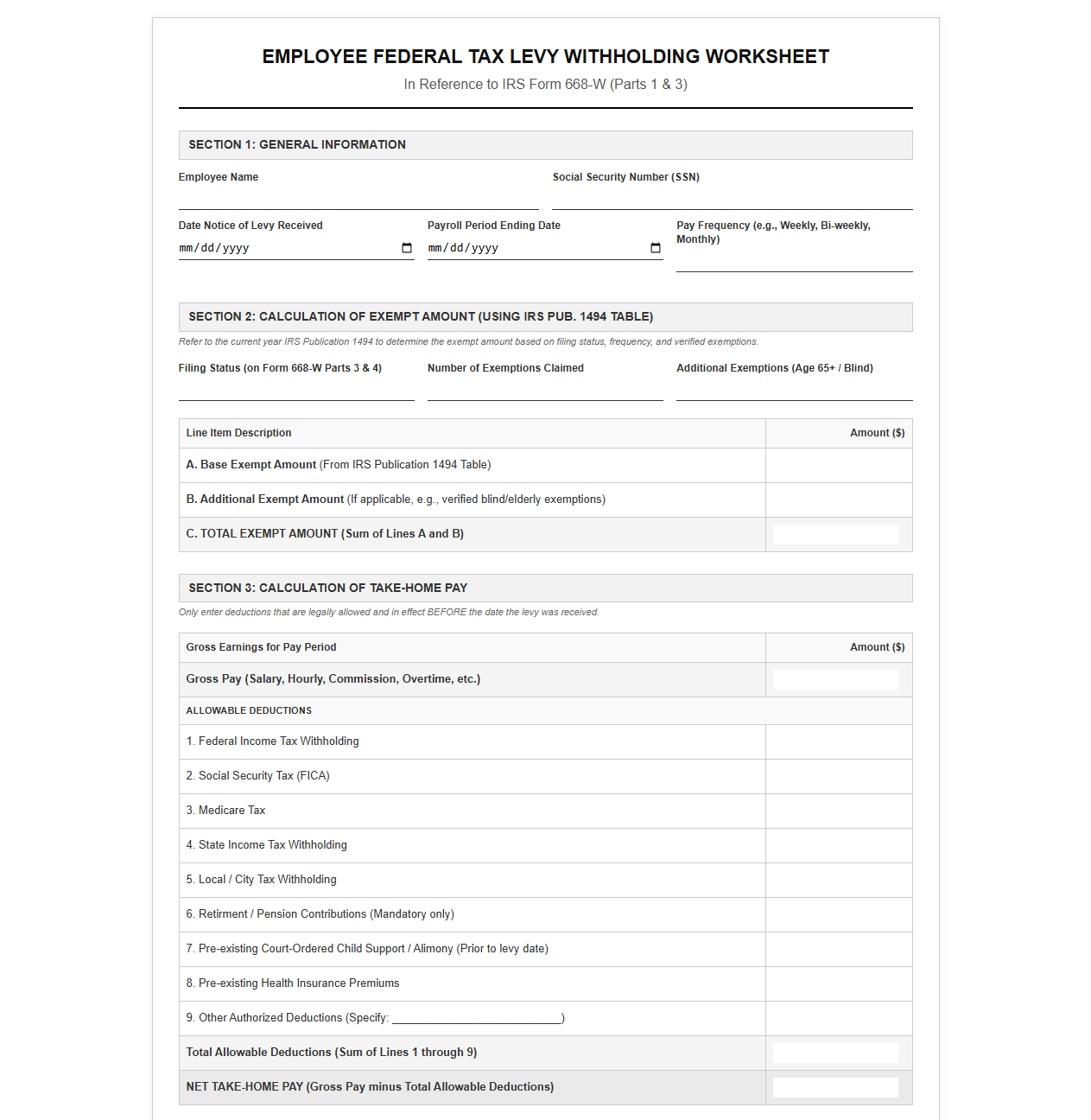

Employee Federal Tax Levy Withholding Worksheet

Download: .PDF

Download: .PDF

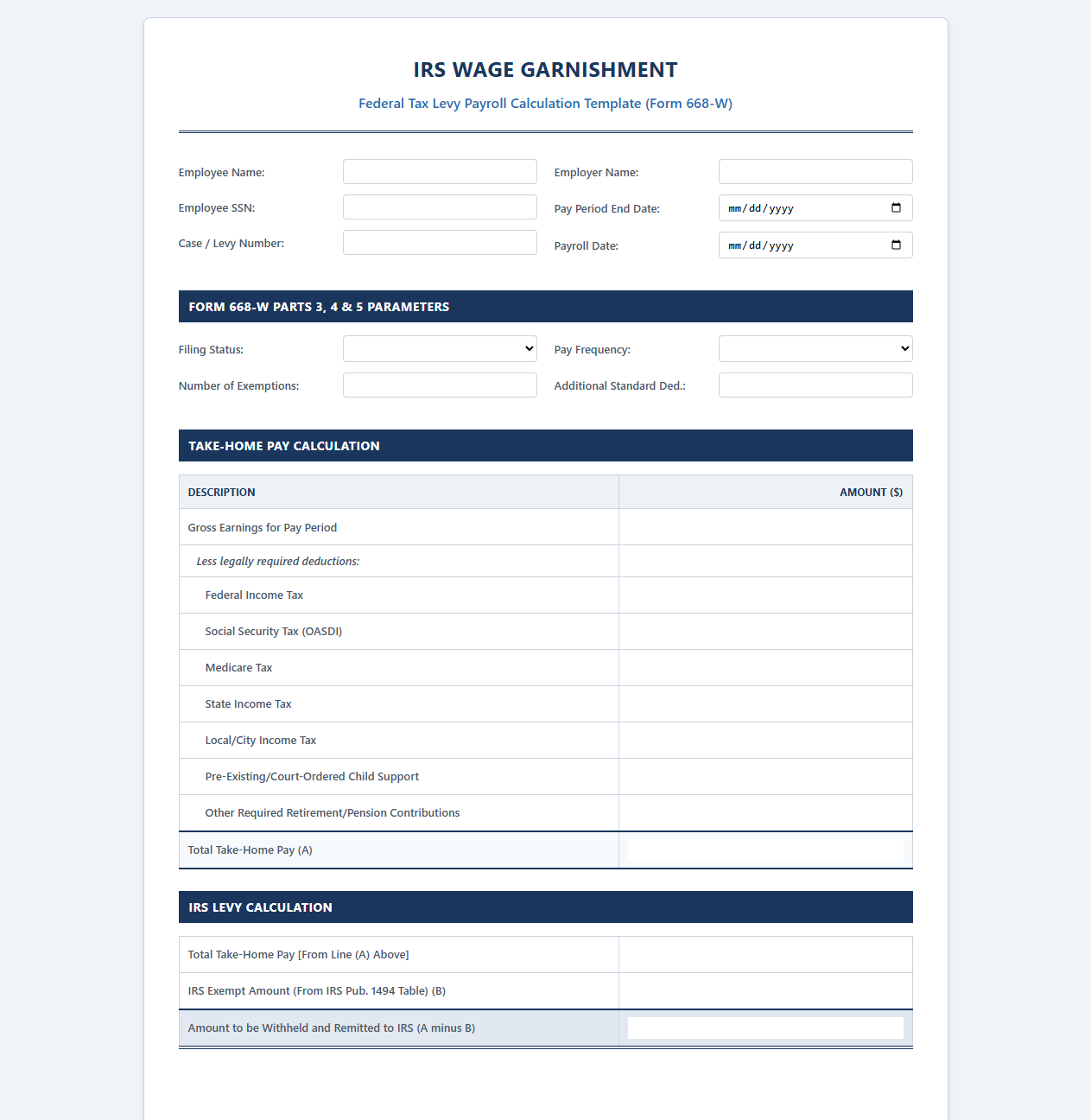

IRS Wage Garnishment Payroll Calculation Template

Download: .PDF

Download: .PDF

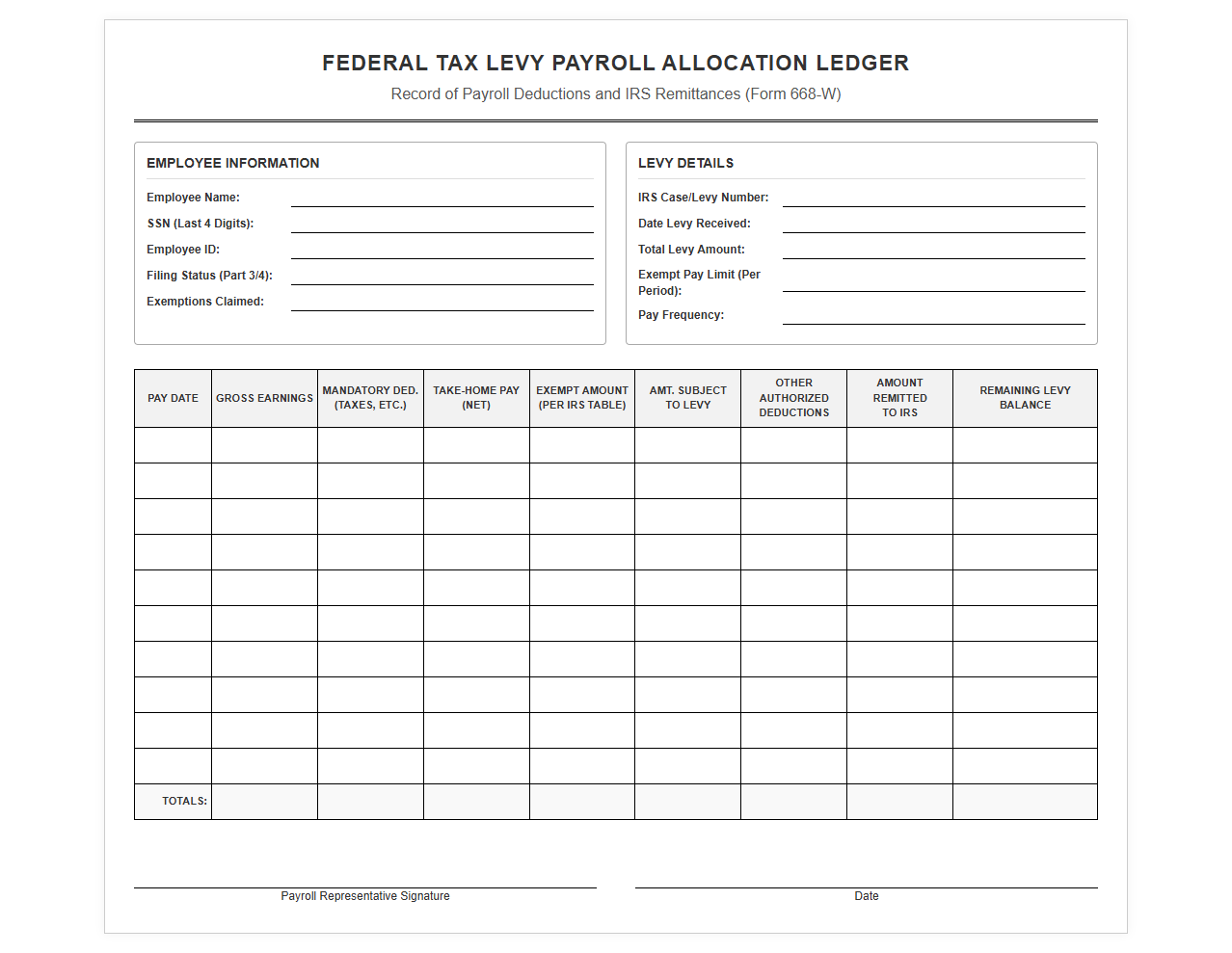

Federal Tax Levy Payroll Allocation Ledger

Download: .PDF

Download: .PDF

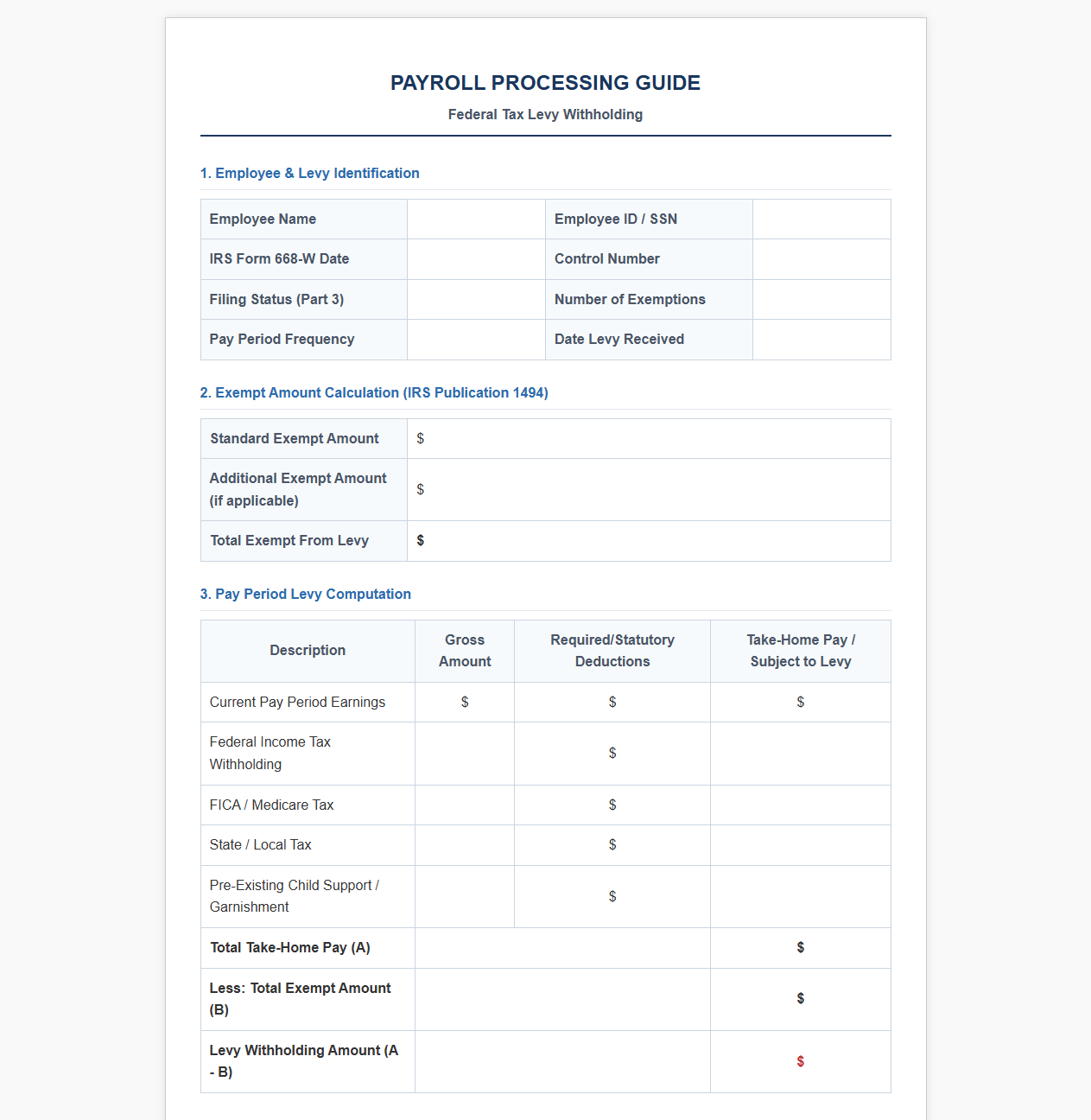

Payroll Processing Guide for Federal Tax Levies

Download: .PDF

Download: .PDF

Federal Tax Levy Employee Payroll Deduction Tracker

![]() Download: .PDF

Download: .PDF

Navigating Federal Wage Garnishments: An Introduction to IRS Levies

An IRS wage levy is a legally binding administrative action issued by the Internal Revenue Service to collect unpaid federal taxes directly from an individual's earnings. When an employee neglects or fails to resolve their tax liabilities, the IRS can attach their wages, salary, commissions, and bonuses. For employers, receiving an IRS levy notice converts the payroll department into an involuntary collection agent for the federal government.

This mandate significantly impacts payroll processing, requiring immediate system adjustments to divert a portion of the employee's net earnings to the IRS. Navigating this process demands meticulous compliance. Failing to honor an IRS wage levy can result in the employer being held personally liable for the full amount of the tax debt, plus an additional 50% statutory penalty for non-compliance. Utilizing standardized document templates is critical to establishing a clear audit trail, mitigating regulatory risks, and ensuring accurate processing across all pay cycles.

Decoding IRS Form 668-W: The Foundation of Payroll Levies

Form 668-W, "Notice of Levy on Wages, Salary, and Other Income," is the formal document the IRS sends to employers to initiate a wage garnishment. Employers are legally obligated to act upon receipt of this form, typically requiring payroll adjustments starting with the very next pay period.

The Employer's Legal Obligations

Upon receiving Form 668-W, an employer must immediately distribute the designated copies to the employee. The employee has a limited window-usually three days-to complete and return the statement of exemptions. If the employee fails to return this statement, the employer is legally required to compute the exempt amount as if the employee is married filing separately with zero dependents, which severely reduces the employee's take-home pay.

Key Data Fields for Extraction

To ensure flawless payroll processing, administrators must carefully extract the following essential details from the form:

- Employee Identifying Information: Full name, current address, and Social Security Number (SSN) to confirm identity.

- Levy Amount: The total unpaid tax liability, interest, and penalties that must be recovered.

- IRS Contact Details: The name, address, and phone number of the IRS officer or office handling the case.

- Date of Notice: The exact date of receipt, which establishes the compliance timeline and effective pay cycle.

Calculating the Exempt Amount: The Employee Statement of Exemptions Template

The IRS does not garnish 100% of an employee's earnings. Under federal law, a portion of the employee's income is exempt from levy to cover basic living expenses. This exempt amount is calculated based on the employee's filing status and the number of personal exemptions claimed on Part 3 of Form 668-W.

To calculate the exempt amount accurately, payroll departments should use the following step-by-step procedure:

- Collect the completed Part 3 (Statement of Exemptions) from the employee within three business days of receiving the levy.

- Locate the appropriate IRS Publication 1494 table corresponding to the current tax year and the employee's pay frequency (e.g., weekly, biweekly, monthly).

- Cross-reference the employee's filing status and claimed exemptions on the Publication 1494 table to find the exact exempt amount.

- Subtract this exempt amount from the employee's net take-home pay (gross pay minus mandatory statutory taxes like FICA, federal, and state income taxes). The remaining balance is the amount that must be remitted to the IRS.

Below is a standardized calculation worksheet template for documenting and auditing the exempt amount calculation:

| Calculation Step | Description / Variable | Amount / Value |

|---|---|---|

| Step 1 | Gross Earnings for the Pay Period | $ _______________ |

| Step 2 | Less: Mandatory Statutory Deductions (Taxes/FICA) | $ _______________ |

| Step 3 | Net Take-Home Pay (Step 1 - Step 2) | $ _______________ |

| Step 4 | Less: IRS Publication 1494 Exempt Amount | $ _______________ |

| Step 5 | Total Remittance Amount to IRS (Step 3 - Step 4) | $ _______________ |

Internal Payroll Processing: The Wage Garnishment Setup Worksheet

Before any funds are withheld, payroll administrators must log the levy details in their internal systems. This worksheet serves as a permanent record of the payroll configuration, ensuring that the deduction remains consistent and traceable throughout the life of the levy.

| Payroll Garnishment Setup Record | |

|---|---|

| Employee ID & Name: | __________________________________________________ |

| IRS Case / Serial Number: | __________________________________________________ |

| Date Form 668-W Received: | ____ / ____ / 20___ |

| Total Levy Amount Outstanding: | $ _________________ |

| Exemption Filing Status & Dependents: | Status: _______________ Dependents: _______________ |

| Calculated Exempt Amount per Pay Period: | $ _________________ |

| Effective Payroll Cycle Date: | ____ / ____ / 20___ |

| Set Up Completed By (Payroll Officer): | __________________________________________________ |

Employee Communication: The Written Notification Letter Template

Receiving an IRS wage levy can be highly stressful for an employee. Employers must notify the employee immediately in writing upon receipt of Form 668-W, explaining that the business is legally obligated to comply and outlining the steps the employee needs to take regarding their exemption claim.

The following template provides a legally compliant and professional way to communicate this sensitive information to the affected employee:

Date: [Insert Date]

To: [Employee Name]

From: Payroll Department / Human Resources

Subject: Notice of Federal Tax Levy on WagesPlease be advised that on [Date Received], [Company Name] received an official IRS Form 668-W (Notice of Levy on Wages, Salary, and Other Income) from the Internal Revenue Service. Under federal law, we are required to withhold a portion of your earnings to satisfy an outstanding tax liability of $[Total Amount Due].

We are enclosing copies of Form 668-W. You must complete and return Part 3 (Statement of Exemptions and Filing Status) to the Payroll Department within three (3) business days of receiving this notice. If we do not receive your completed Part 3 within this timeframe, we are legally required to calculate your exempt amount using the default status of "Married Filing Separately" with zero exemptions, which will significantly reduce your take-home pay.

The deductions will begin with the pay period ending [Pay Period End Date] and will continue until we receive an official release form (Form 668-D) from the IRS. If you have questions regarding this tax debt, please contact the IRS directly at the phone number listed on the attached form.

Sincerely,

[Payroll Manager Name]

[Company Name]

Payment Remittance: Standardizing the IRS Levy Payment Submission Log

Remitting the withheld funds to the IRS must occur immediately on the same day employees are paid. Most employers remit these payments electronically using the Electronic Federal Tax Payment System (EFTPS). Accurate record-keeping is vital to protect the business from claims of non-payment or late submission.

This tracking log must be updated during every pay run to document every dollar deducted and sent to the IRS:

| Pay Date | Check / Gross Amount | Levy Amount Withheld | EFTPS Confirmation Number | Date Remitted | Authorized Sign-Off |

|---|---|---|---|---|---|

| ___/___/20__ | $ ___________ | $ ___________ | ____________________ | ___/___/20__ | _______________ |

| ___/___/20__ | $ ___________ | $ ___________ | ____________________ | ___/___/20__ | _______________ |

| ___/___/20__ | $ ___________ | $ ___________ | ____________________ | ___/___/20__ | _______________ |

Resolving the Levy: The IRS Form 668-D Release Tracking Template

An IRS wage levy is continuous and remains in effect until the tax debt is fully satisfied, or until the IRS issues a formal release. Employers must never stop withholding funds based on an employee's verbal statement or standard tax documents; only Form 668-D (Release of Levy/Release of Property) authorizes the cessation of deductions.

How to Handle a Levy Release

When the employer receives Form 668-D, the payroll department must quickly review the document to identify the effective release date. Any wages earned after this date must be paid directly to the employee without levy deductions. If any over-withholding occurred between the release date and the processing date, those funds must be promptly refunded to the employee.

Post-Levy Audit and Closure Checklist

To safely close the garnishment file, the payroll department should complete the following administrative audit checklist:

- Verify that the physical Form 668-D is on file and contains a valid IRS signature or stamp.

- Match the total cumulative payments remitted on the Payment Submission Log with the total balance requested on the original Form 668-W.

- Deactivate the levy deduction code in the payroll system to prevent future unauthorized withholding.

- Document and process any necessary refunds to the employee if deductions occurred after the official release date.

- Archive all related records, including Form 668-W, Form 668-D, internal worksheets, and communication logs, for a minimum of seven years to comply with standard corporate document retention policies.

Leave a comment