Navigating nonresident alien (NRA) payroll tax withholding is a notorious administrative headache for HR and payroll professionals, fraught with complex compliance risks and IRS penalties. This difficulty stems from the intricate web of federal regulations and international tax treaties that govern foreign national employees.

However, establishing a standardized documentation process grants your organization both operational efficiency and robust audit protection. While standardized templates greatly streamline data collection, it is important to stipulate that these tools must be tailored to your specific organizational structure and should not replace professional tax counsel.

Utilizing structured templates for critical intake forms-such as Form W-8BEN for beneficial status or Form 8233 for treaty-exempt compensation-ensures accurate withholding calculations from day one. In this article, we will outline the essential payroll document templates your team needs, how to implement them, and best practices for maintaining flawless compliance.

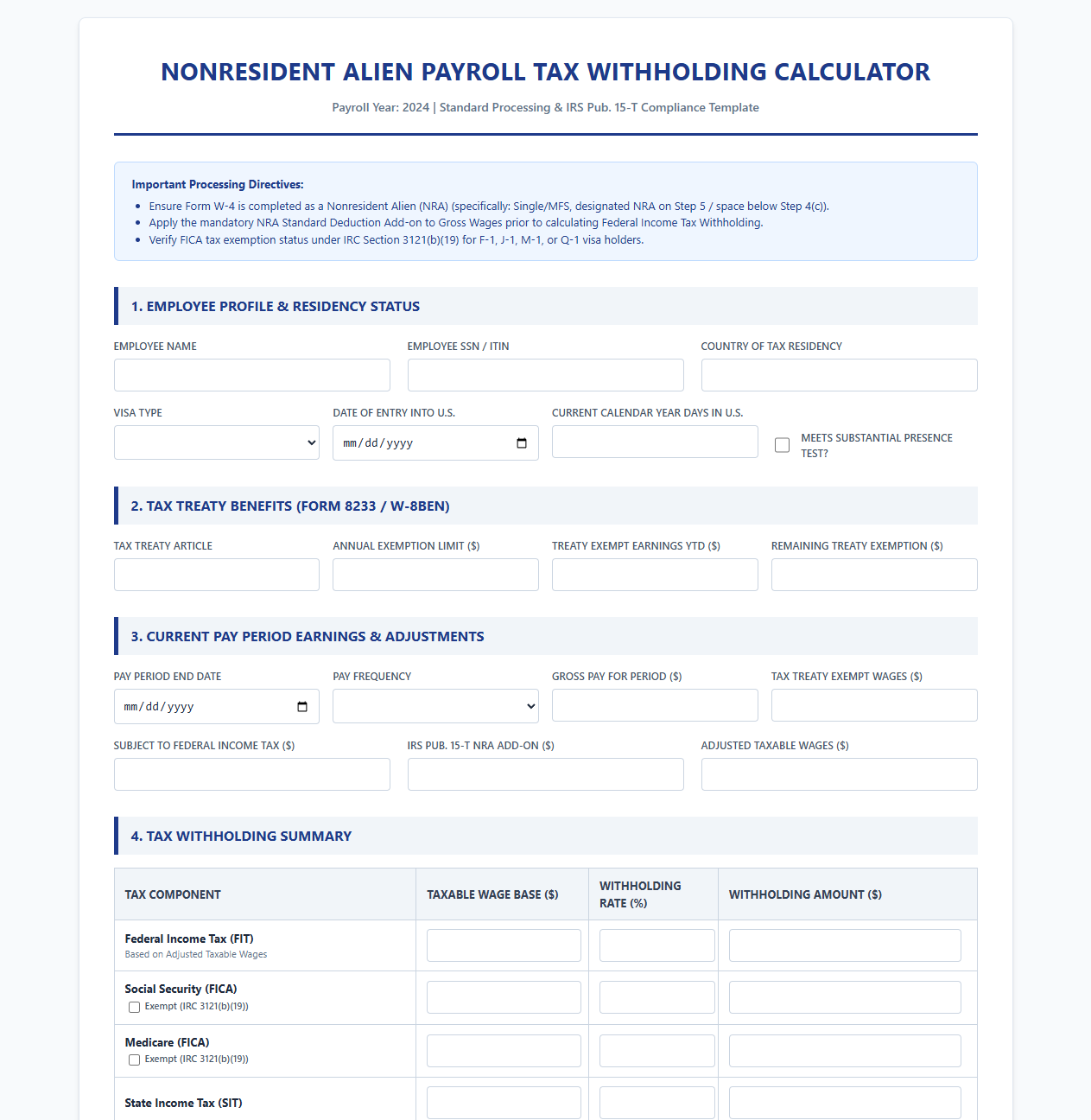

Nonresident Alien Payroll Tax Withholding Calculator

Download: .PDF

Download: .PDF

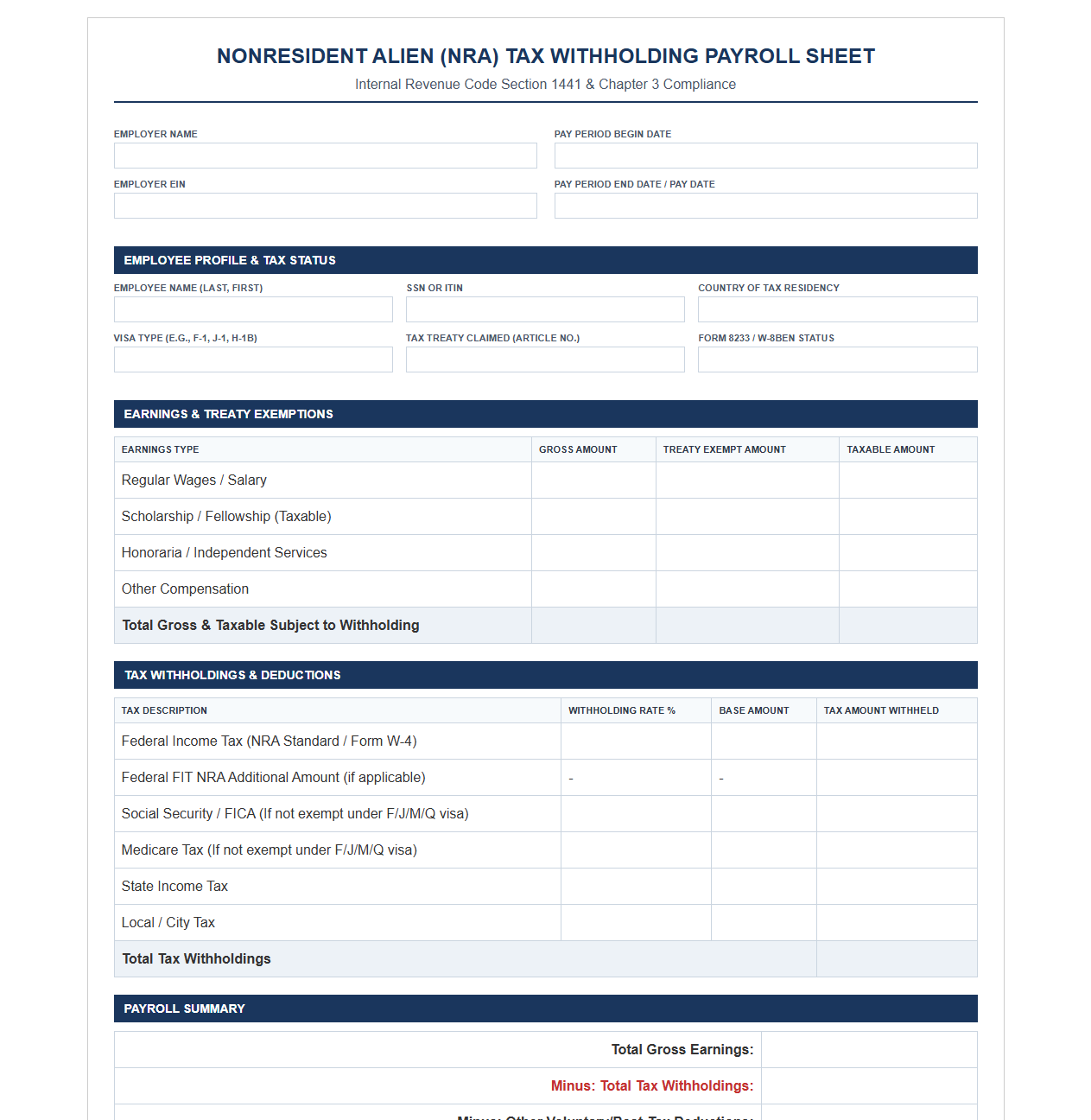

NRA Tax Withholding Payroll Sheet

Download: .PDF

Download: .PDF

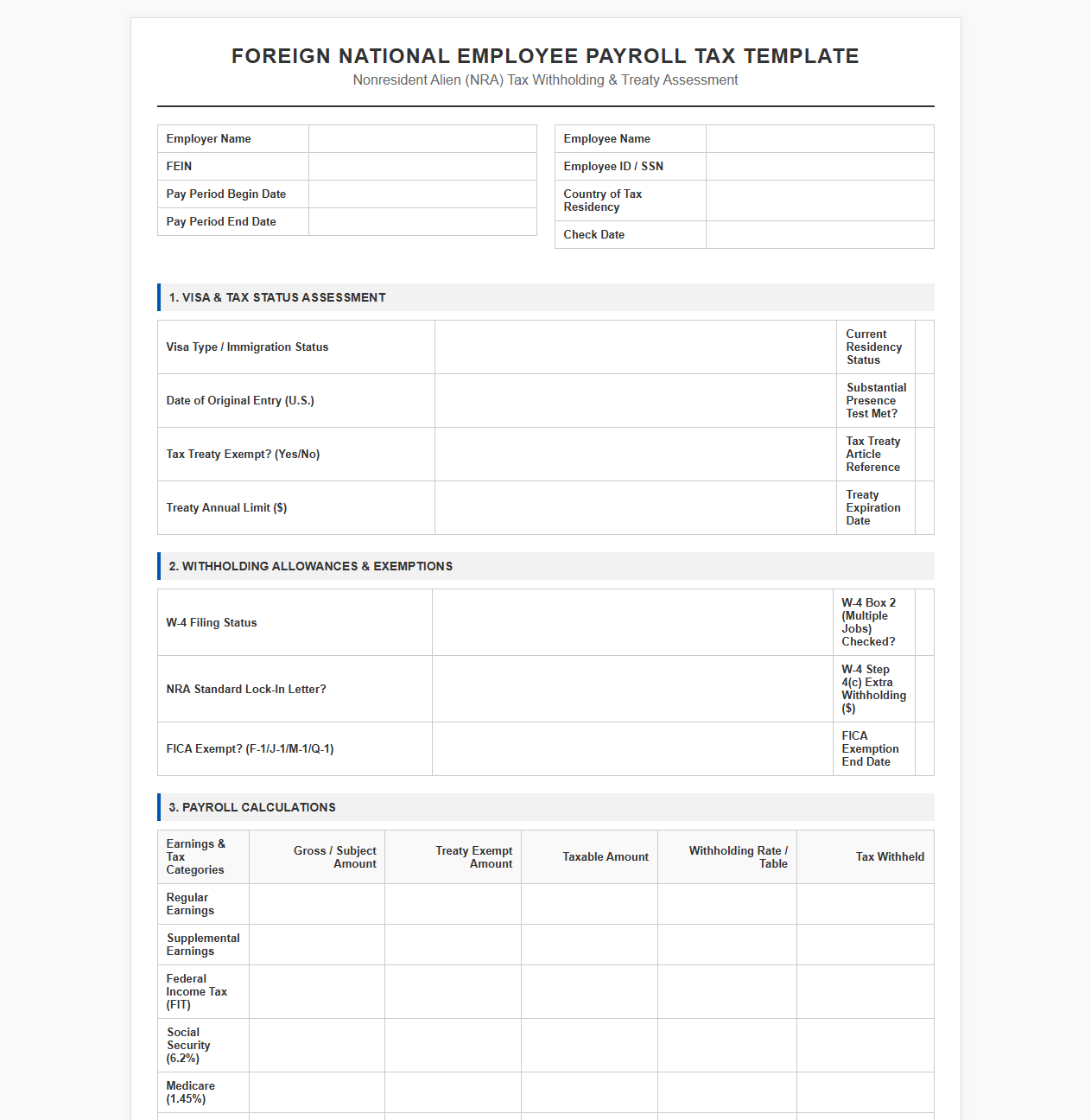

Foreign National Employee Payroll Tax Template

Download: .PDF

Download: .PDF

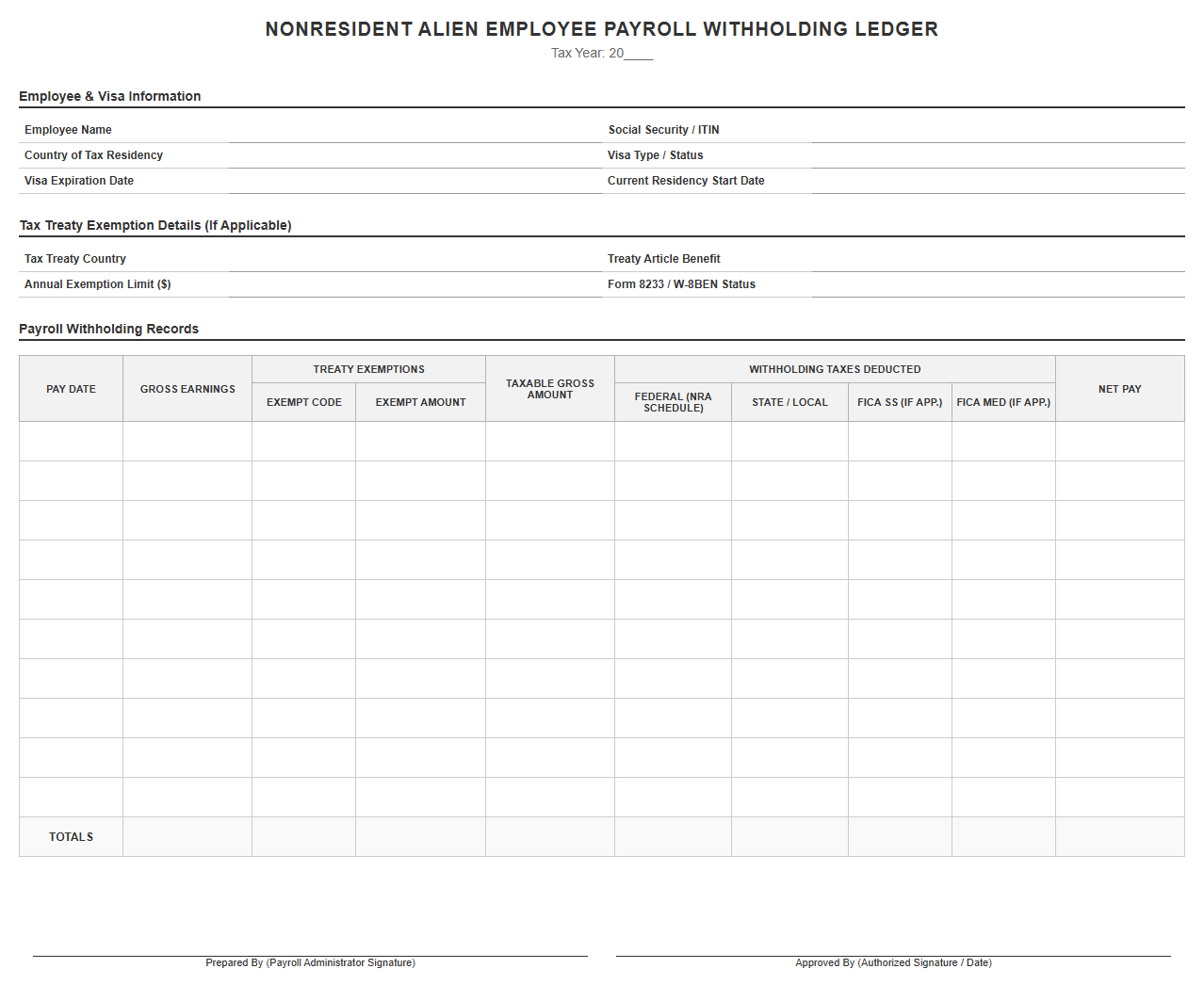

Nonresident Alien Employee Payroll Withholding Ledger

Download: .PDF

Download: .PDF

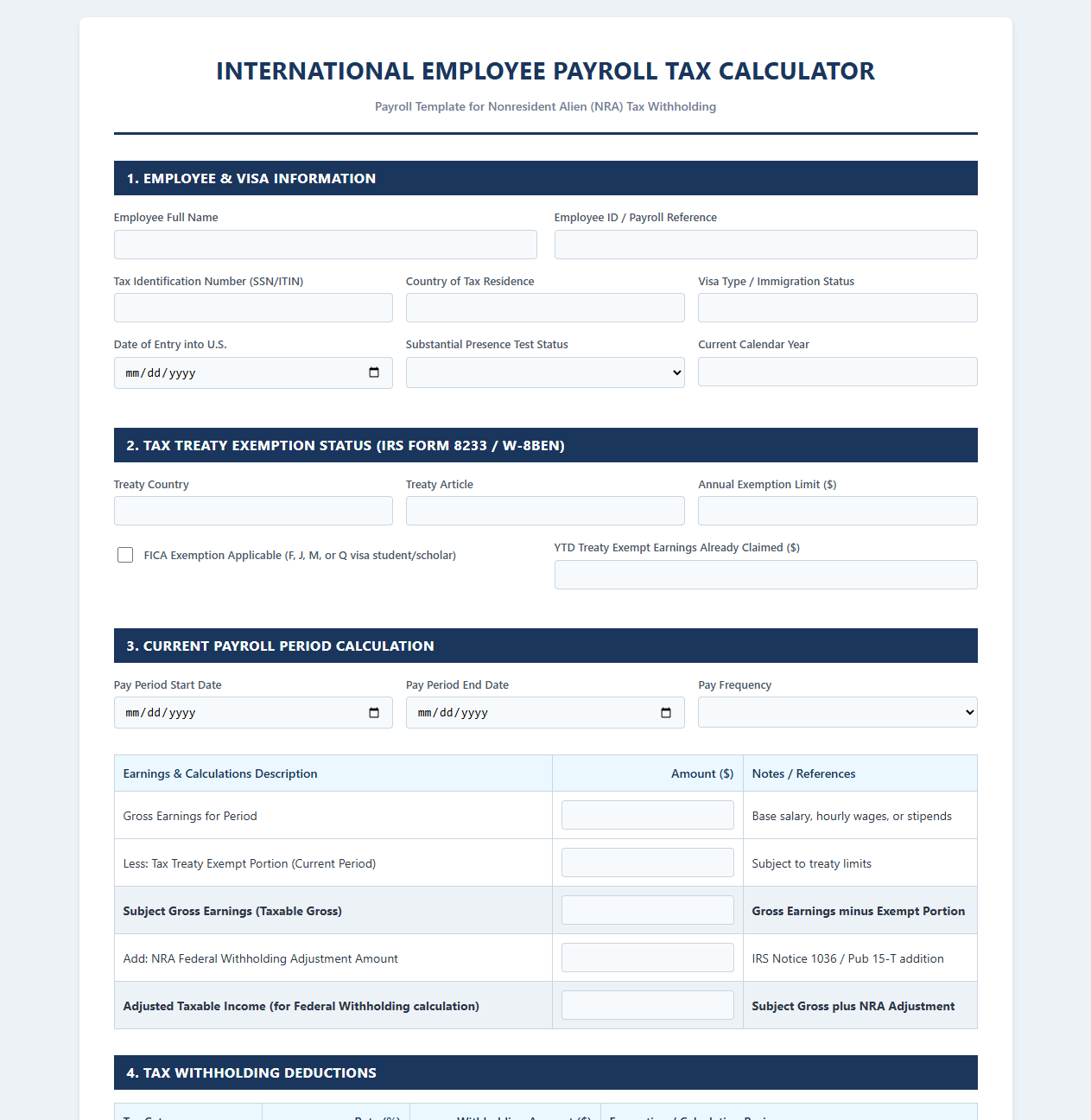

International Employee Payroll Tax Calculator

Download: .PDF

Download: .PDF

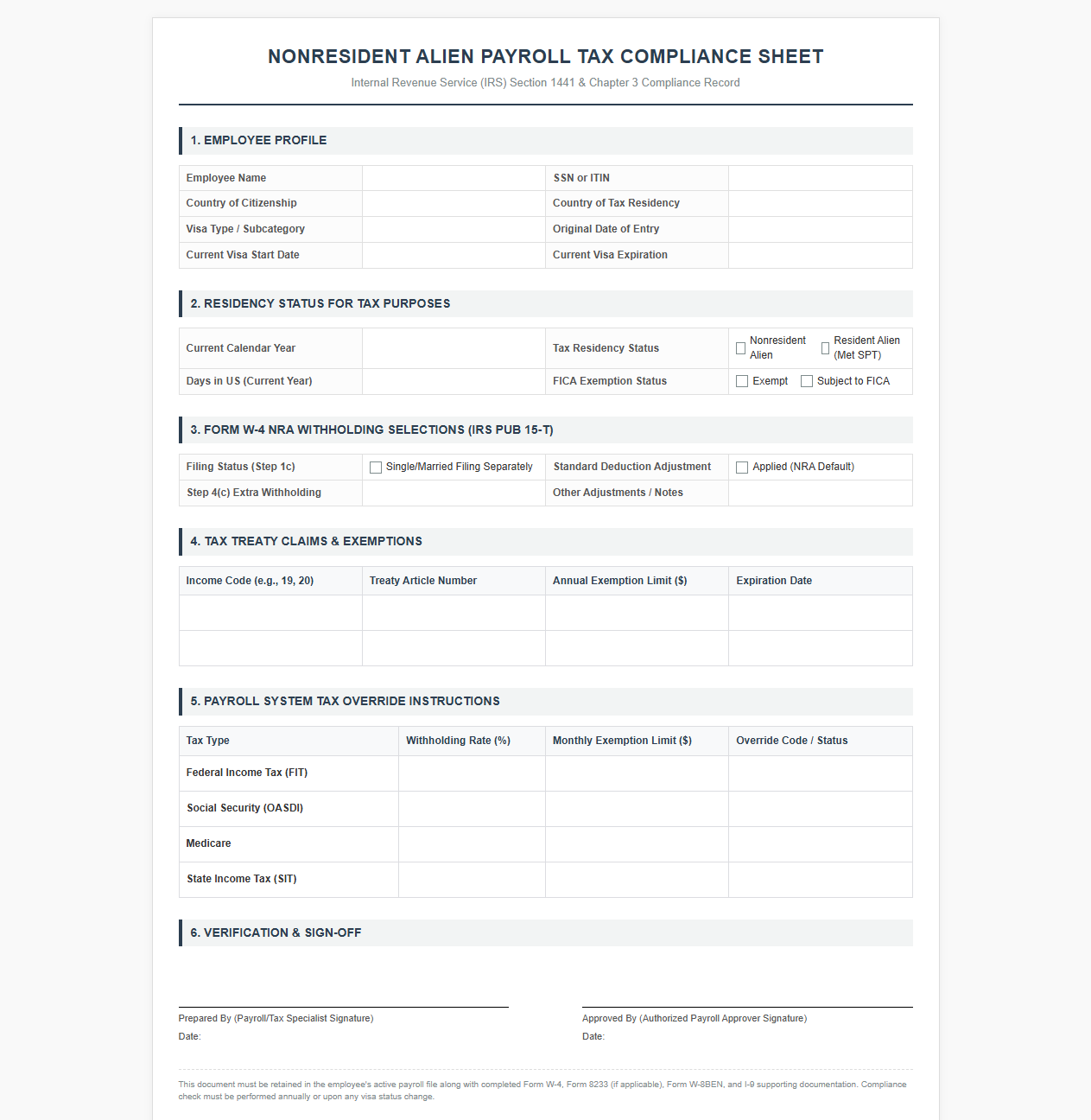

Nonresident Alien Payroll Tax Compliance Sheet

Download: .PDF

Download: .PDF

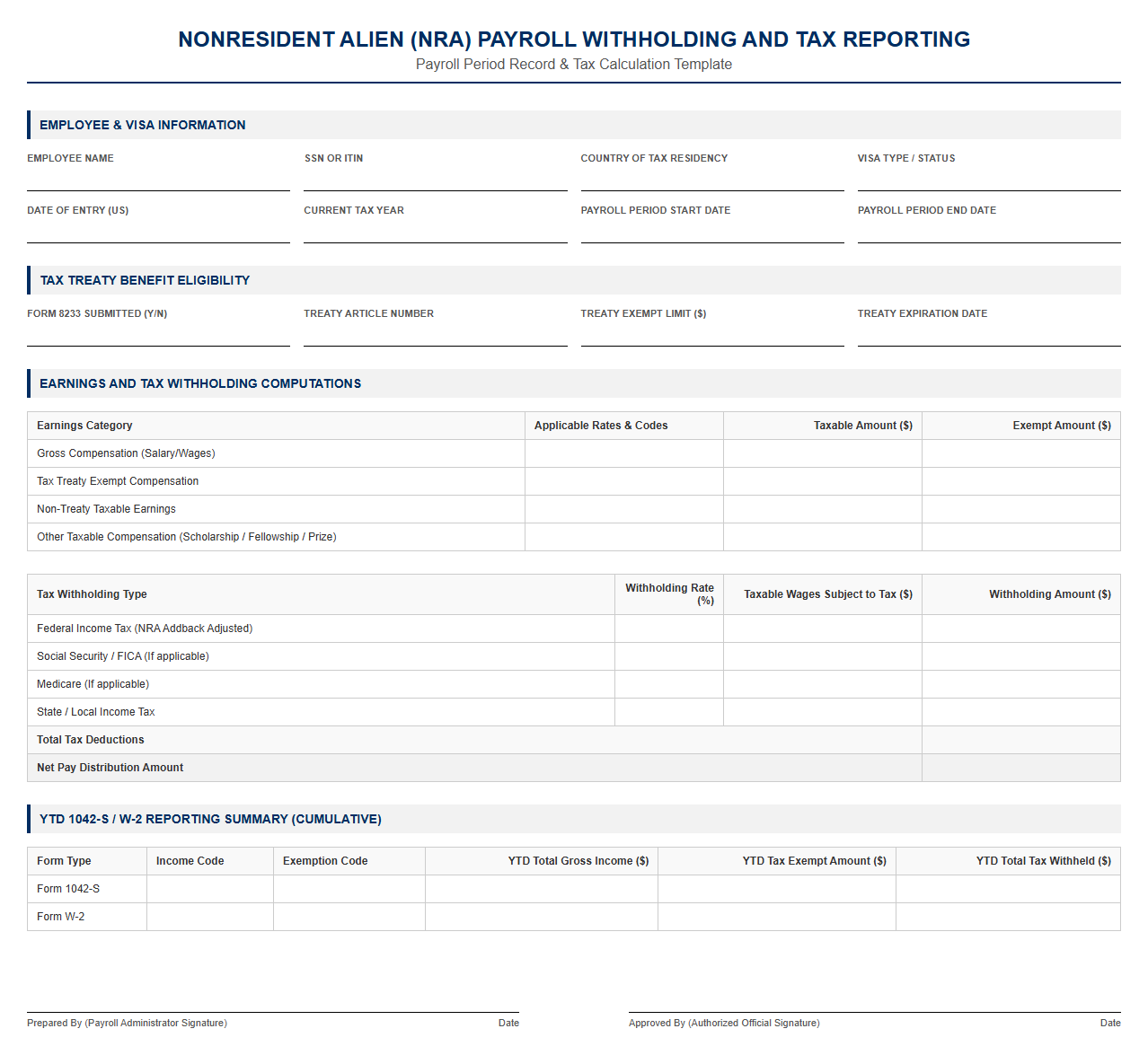

NRA Payroll Withholding and Tax Reporting Template

Download: .PDF

Download: .PDF

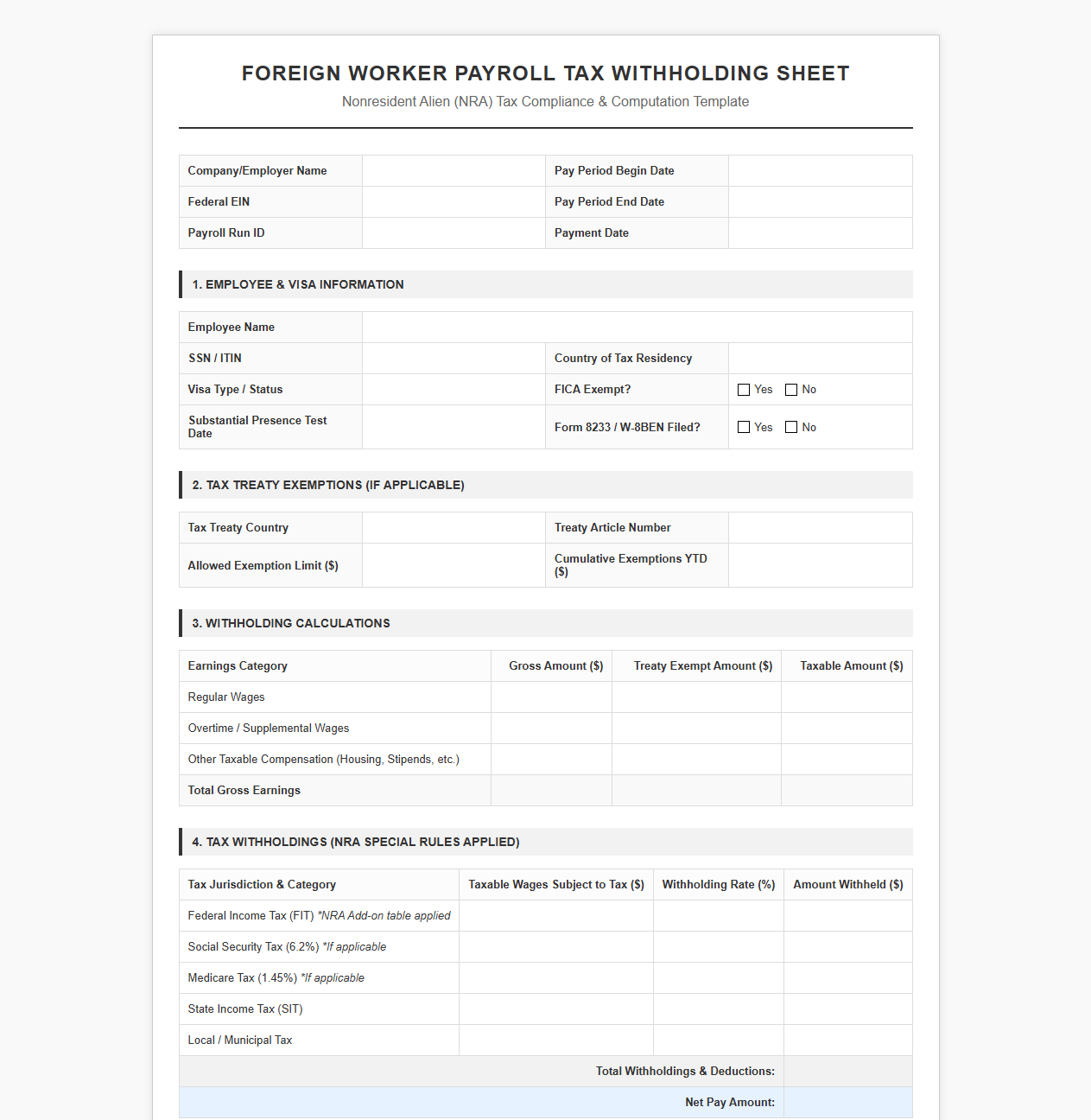

Foreign Worker Payroll Tax Withholding Sheet

Download: .PDF

Download: .PDF

Navigating Nonresident Alien Tax Compliance in Modern Payroll

Managing payroll for international employees introduces complex regulatory responsibilities. For United States organizations, hiring foreign talent requires strict adherence to Internal Revenue Service (IRS) regulations governing nonresident aliens (NRAs). As a withholding agent, an employer assumes the legal and financial responsibility for accurately identifying tax status, determining withholding rates, and remitting taxes to the federal government. Failing to correctly apply the substantial presence test can lead to severe misclassifications, resulting in back taxes, interest, and substantial administrative penalties.

To mitigate these risks, organizations must move away from ad-hoc processes and implement standardized document templates. Consistent templates act as a crucial defensive barrier, ensuring that payroll administrators capture the exact data required to establish residency status, validate treaty eligibility, and secure proper withholdings from day one. In an era of remote work and global mobility, structured documentation is the cornerstone of a compliant corporate payroll architecture.

The Foundation: Standardizing Form W-8BEN for Payroll Portals

Form W-8BEN (Certificate of Foreign Status of Beneficial Owner) is the foundational document for establishing that an individual is a foreign person and the beneficial owner of the income being paid. In the context of payroll processing, this form ensures that the organization does not apply standard domestic withholding rules to a foreign national who may qualify for reduced withholding rates or complete tax exemptions under an applicable income tax treaty. Integrating clear instructions into your employee self-service payroll portal helps guide nonresident alien employees through the nuances of this form, minimizing processing delays.

To maintain absolute compliance, payroll departments must carefully audit every submitted Form W-8BEN. The verification team must ensure the following critical fields are complete and accurate before applying any tax modifications:

- Line 1: Full legal name of the individual matching their passport and visa documentation.

- Line 2: Country of citizenship, which must align with the treaty benefits claimed.

- Line 3: Permanent residence address (must be outside the United States; a P.O. Box is generally invalid).

- Line 5 or 6: A valid U.S. Taxpayer Identification Number (SSN or ITIN) or a Foreign Tax Identifying Number.

- Part II, Line 9 & 10: Explicit claim of tax treaty benefits, including the specific country of treaty residence and the treaty article being invoked.

- Part III: A hand-signed (or legally compliant electronic signature) and dated certification.

Managing Tax Treaty Exemptions with Form 8233

While Form W-8BEN is utilized for passive income or specific independent services, Form 8233 (Information Notice of Claim of Treaty Exemption for Compensation for Independent Personal Services of a Nonresident Alien Individual) is the primary document required for employees claiming treaty exemptions on dependent personal services (salaries and wages). This form must be completed annually and submitted to the IRS for review. Because a valid Form 8233 legally permits the employer to stop or reduce Federal Insurance Contributions Act (FICA) or federal income tax withholding, administrators must execute a strict verification routine to validate the treaty claim.

Before implementing the tax exemption in the payroll engine, administrators must coordinate with the IRS. This sequential process dictates how the 10-day review period must be managed:

- The employee completes and signs Form 8233, including the required withholding agent certification section, and submits it alongside a supporting statement detailing visa history and eligibility criteria.

- The payroll administrator reviews the document for completeness, verifies the tax treaty article, and officially signs the withholding agent acceptance block.

- The employer submits the completed Form 8233 to the IRS via the secure fax or mail portal designated for international withholding.

- The payroll department initiates a 10-day holding period from the date of mailing or transmission, during which the employer must wait for an IRS response.

- If the IRS does not object to the treaty claim within those 10 calendar days, the payroll department may safely apply the tax treaty exemption to the employee's subsequent paychecks.

Implementing an Internal Tax Treaty Verification Checklist

To guarantee that no step is missed during the verification process, payroll departments should utilize a standardized internal checklist. This document serves as a critical audit trail, linking the employee's immigration status, treaty eligibility, and active payroll profile. Below is the structured layout for the internal tax treaty verification process:

| Verification Step | Required Action / Documentation | Responsible Party |

|---|---|---|

| Immigration Status Check | Confirm active F-1, J-1, H-1B, or O-1 visa class. Verify passport validity. | HR/Global Mobility Specialist |

| Substantial Presence Test | Review historic presence data using travel history from I-94 travel records. | Payroll Administrator |

| Form 8233/W-8BEN Audit | Validate signatures, treaty articles, and foreign address details. | Payroll Administrator |

| Supporting Statement Review | Ensure the treaty attachment contains the mandatory student/teacher certification. | Tax Compliance Officer |

| IRS 10-Day Waiting Period | Track IRS submission date and wait 10 days before updating payroll tax profile. | Payroll Administrator |

Documenting Presence and Source of Income: The NRA Statement Template

Correctly identifying whether compensation is U.S.-sourced or foreign-sourced is vital for accurate withholding. Nonresident aliens are only taxed on U.S.-sourced income, whereas resident aliens are taxed on their worldwide income. To capture physical presence details that might not be recorded on standard federal tax forms, payroll teams must utilize a custom NRA Statement. This template captures specific arrival and departure dates, visa adjustments, and explicit statements regarding where the actual services will be performed.

Standardizing this declaration ensures that employees understand the legal nature of their tax residency status. Incorporating a clear, legally binding clause protects the organization against future audits by shifting the responsibility of travel record accuracy to the employee:

"I hereby declare under penalty of perjury that I am a citizen or subject of the country listed below, and that my physical presence within the United States during the current tax year does not meet the requirements of the Substantial Presence Test. I certify that all services performed under this agreement are conducted entirely at my designated work location, and I will notify the payroll department within 10 days of any change to my visa status or physical residency."

Streamlining Year-End Compliance: Preparing for Form 1042-S Reporting

At the close of each calendar year, payroll departments must compile, reconcile, and file Form 1042-S (Foreign Person's U.S. Source Income Subject to Withholding). Unlike domestic Form W-2 reporting, Form 1042-S must be prepared for each type of income subject to withholding paid to nonresident foreign individuals. Ensuring that monthly payroll registers, tax treaty exemptions, and employee withholding templates are fully aligned throughout the year makes the year-end reconciliation process smooth and reduces the risk of reporting discrepancies.

Administrators must reconcile total gross income, exempt amounts, and actual taxes withheld across all active payroll files prior to generating the final forms. A single misaligned data point can trigger automated IRS mismatch notices, auditing flags, and substantial financial corrections.

Digital Integration: Automating the NRA Payroll Workflow

To eliminate manual errors and streamline the complex compliance landscape of nonresident alien taxation, modern enterprises are migrating toward automated, digital workflows. Integrating standardized tax templates directly into Human Resource Information Systems (HRIS) allows organizations to digitize the collection of Form W-8BEN, Form 8233, and custom residency questionnaires. Software-guided onboarding portals can analyze employee responses instantly, identifying tax status with high accuracy and automatically updating payroll systems.

By executing these strategies, enterprises achieve real-time validation of worker statuses, protecting the organization from costly compliance failures. Transitioning to integrated systems ensures permanent audit readiness, transforming what was once a highly stressful manual audit cycle into an automated, background tax assurance workflow.

Leave a comment