Corporations facing IRS scrutiny under the accumulated earnings tax (IRC Section 531) often struggle to justify their retained earnings without robust, formalized documentation. Navigating this complex regulatory landscape requires a clear understanding of IRS evaluation metrics before compiling your defensive files. Fortunately, utilizing standardized document formats grants tax professionals and corporate officers the exact framework needed to accelerate audit readiness and mitigate compliance risks.

Please note: while these templates streamline the documentation process, they serve as foundational guides and must be tailored to your specific corporate lifecycle and local jurisdictions.

To assist your defense, this guide provides actionable tools, including Bardahl formula calculation worksheets and formal corporate resolution templates. In the following sections, we will explore the essential document formats, key defense strategies, and step-by-step templates required to successfully resolve accumulated earnings tax liabilities.

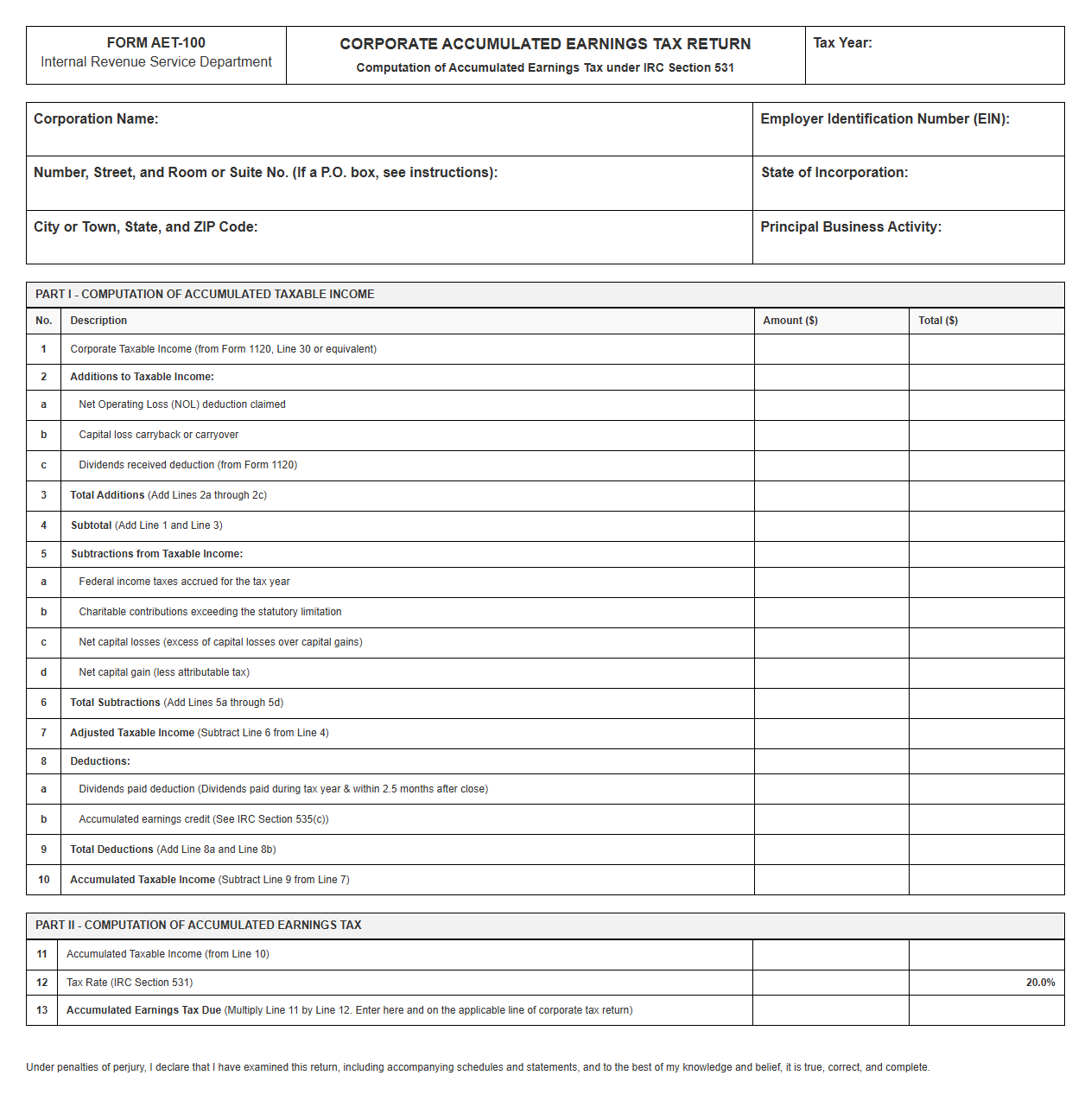

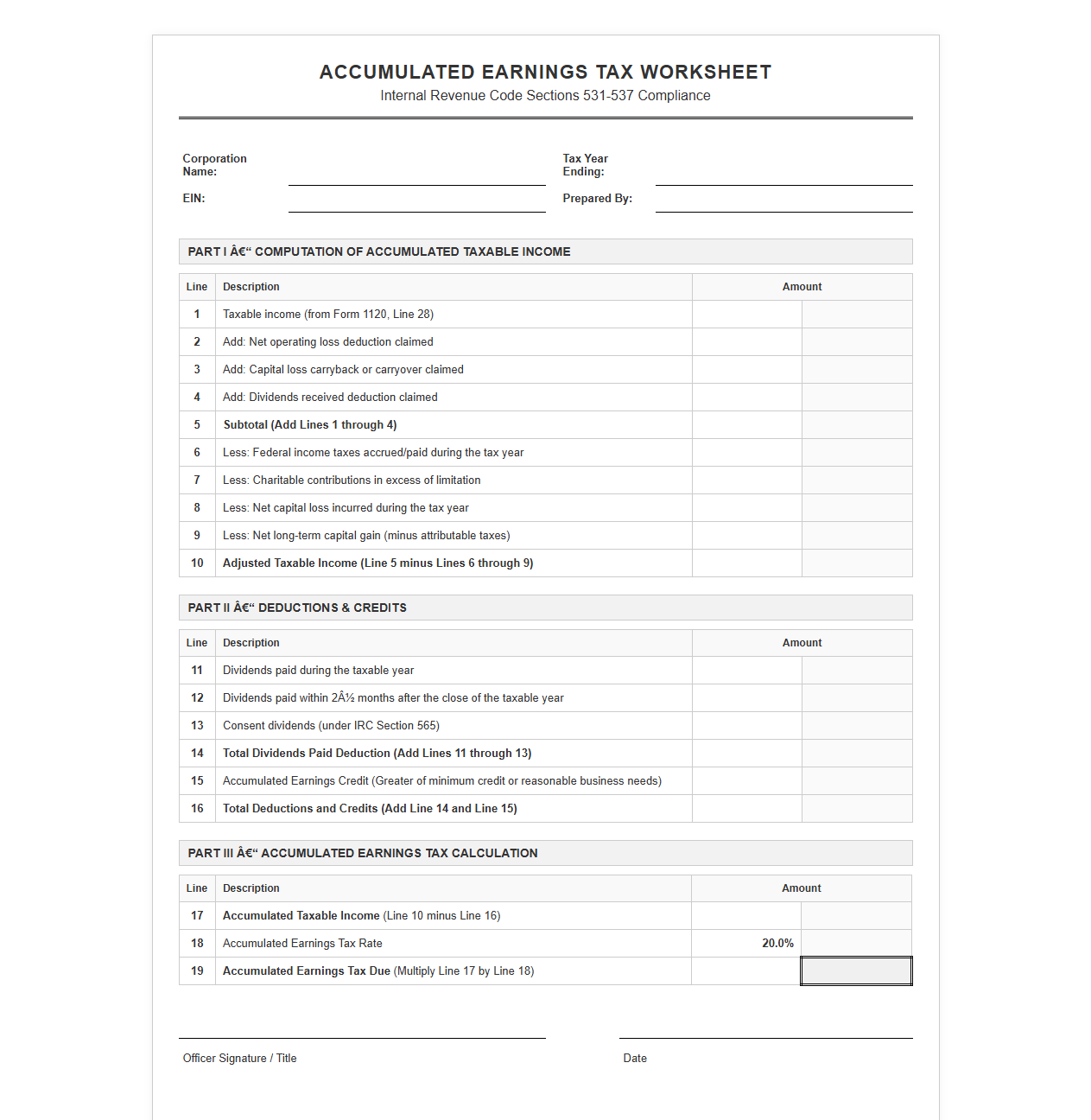

Accumulated Earnings Tax Return Template

Download: .PDF

Download: .PDF

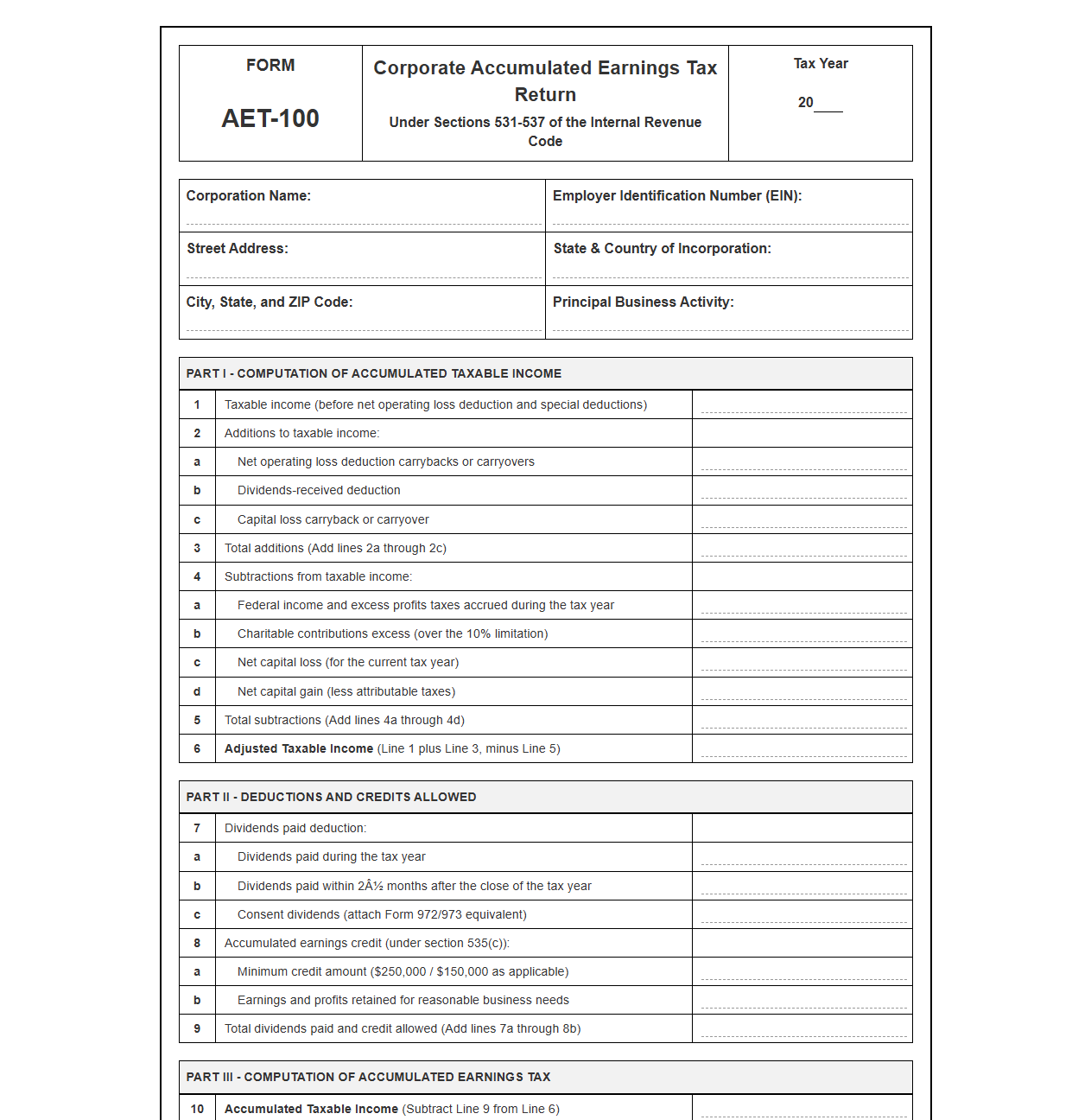

Corporate Accumulated Earnings Tax Filing Form

Download: .PDF

Download: .PDF

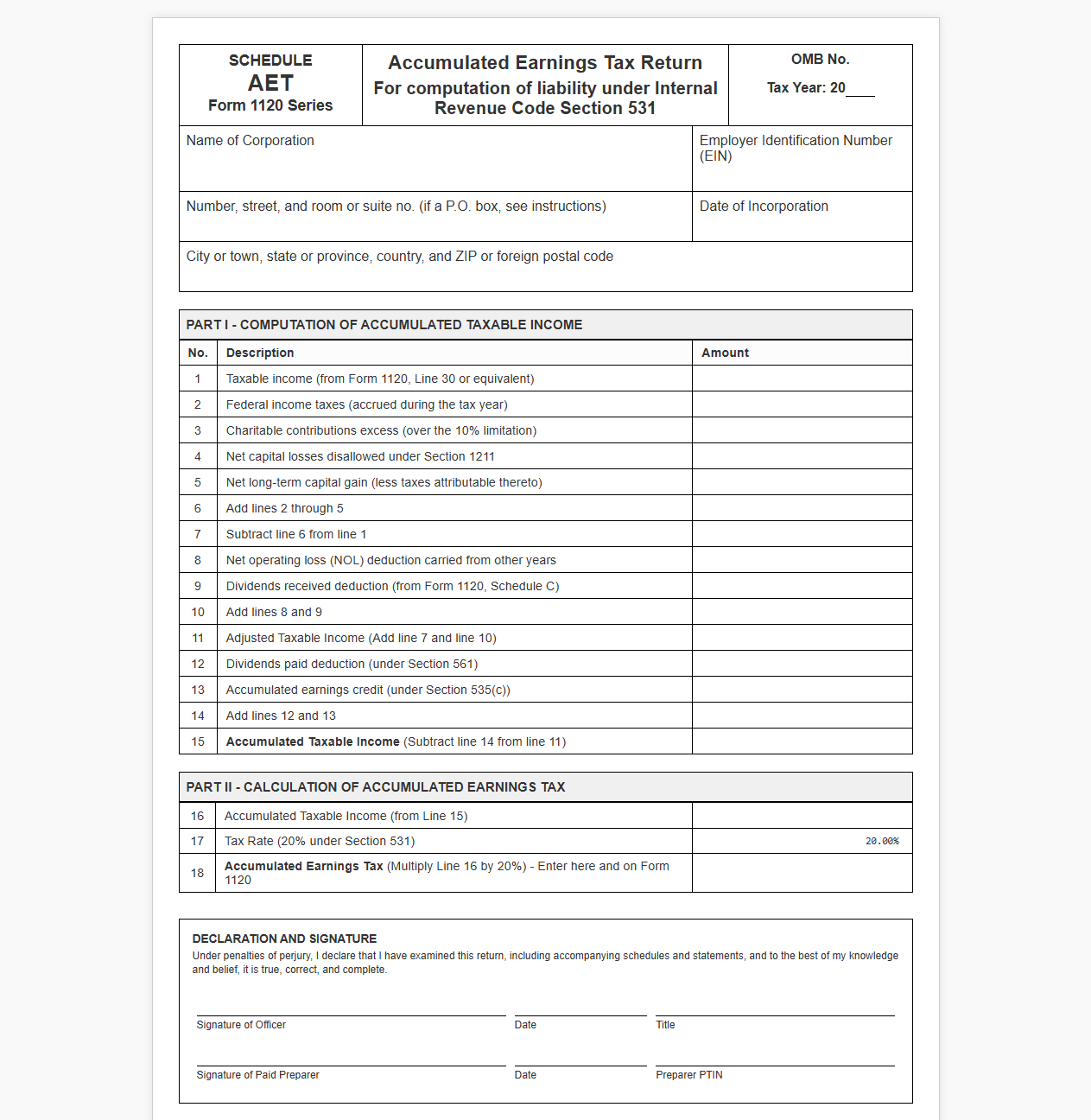

Form for Corporate Accumulated Earnings Tax Return

Download: .PDF

Download: .PDF

Corporate Accumulated Earnings Tax Calculation Sheet

Download: .PDF

Download: .PDF

Annual Corporate Accumulated Earnings Tax Return

Download: .PDF

Download: .PDF

IRS Section 531 Accumulated Earnings Tax Return

Download: .PDF

Download: .PDF

Corporate Accumulated Earnings Tax Declaration Template

Download: .PDF

Download: .PDF

Accumulated Earnings Tax Return Worksheet for Corporations

Download: .PDF

Download: .PDF

Understanding Corporate Accumulated Earnings Tax Liability

The Accumulated Earnings Tax (AET) is a penalty tax imposed by the Internal Revenue Service (IRS) on corporations that retain earnings instead of distributing them as dividends to shareholders. Under Section 531 of the Internal Revenue Code, this tax is designed to prevent corporations from being used as a shield to avoid personal income taxes on their shareholders. When a corporation's accumulated earnings exceed the reasonable needs of the business, Section 532 subjects the entity to an additional tax rate on its accumulated taxable income.

To defend against an IRS audit under Section 531, a corporation must demonstrate that its retained earnings are held for "reasonable anticipated needs of the business" as defined under Section 537. Having pre-structured document templates is critically important. These templates allow corporate officers to systematically record and prove that their accumulation of earnings is tied to concrete, active projects rather than tax avoidance, creating a clear paper trail before the IRS raises questions.

Essential Elements of a Defense-Ready Corporate Resolution Template

A formal Board of Directors resolution serves as the primary corporate record of intent. To withstand IRS scrutiny, the resolution must document specific, definite, and feasible plans for utilizing accumulated earnings. Standard boilerplates are insufficient; the documentation must outline exact operational goals.

- Recital Clauses (Whereas Clauses): Clearly state the current financial position of the corporation and the specific business opportunities or risks identified by the board.

- Specific Project Authorization: Detail the exact nature of the project, such as purchasing a new facility, acquiring a competitor, or funding a specific research and development phase.

- Allocation of Funds: Formally designate a precise dollar amount from the accumulated earnings to be set aside exclusively for the approved project.

- Timeline and Feasibility Clause: Establish a realistic schedule with milestones, proving that the project is active and not a vague future concept.

- Officer Directive: Instruct corporate officers to execute contracts, obtain permits, or make down payments to demonstrate immediate action toward the goal.

Format for the Statement of Business Needs (IRC Section 537)

Under Section 537, the corporation must maintain a detailed Statement of Business Needs. This document serves as the operational roadmap justifying the retention of capital. Below is a fillable template format designed to outline expansion plans, product development, or business acquisitions.

STATEMENT OF BUSINESS NEEDS & CAPITAL ACCUMULATION JUSTIFICATION

PURSUANT TO IRC SECTION 537

1. GENERAL INFORMATION

Corporation Name: [Insert Company Name]

Fiscal Year Ending: [Insert Year-End Date]

Prepared By: [Insert Officer Name/Title]

2. IDENTIFIED BUSINESS NEED

Category (check all that apply):

[ ] Plant Expansion/Real Estate Acquisition

[ ] Product Development / R&D

[ ] Business Acquisition (M&A)

[ ] Working Capital Requirements (Bardahl Formula)

[ ] Specific Contingency Reserve (e.g., litigation, key customer loss)

3. DETAILED DESCRIPTION OF PROJECTED NEED

Provide a detailed narrative of the specific, definite, and feasible plan:

[Insert detailed narrative here. Reference feasibility studies, blueprints,

or vendor quotes where applicable.]

4. FINANCIAL ALLOCATION AND ESTIMATED COSTS

- Estimated Capital Expenditure: $_________________

- Source of Estimate: [e.g., Third-party contractor bid, historical cost analysis]

- Expected Completion Date: [Date]

5. RESOLUTION LINKAGE

This statement is supported by Board of Directors Resolution No. [____],

adopted on [Date of Board Meeting].

Standardized Bardahl Formula Worksheet Template

The Bardahl Formula is the mathematically accepted method for calculating a corporation's working capital needs for one operating cycle. The calculation compares the corporation's current liquid assets against its working capital needs to determine if there is an excess accumulation of earnings.

| Step | Calculation Description | Formula / Input Value | Resulting Percentage / Value |

|---|---|---|---|

| 1 | Inventory Cycle | Average Inventory / Cost of Goods Sold | [_____] % of Year |

| 2 | Accounts Receivable Cycle | Average Receivables / Annual Net Sales | [_____] % of Year |

| 3 | Operating Cycle | Step 1 % + Step 2 % | [_____] % of Year |

| 4 | Credit Cycle (Reduction) | Average Accounts Payable / Annual Purchases | [_____] % of Year |

| 5 | Net Operating Cycle | Step 3 % - Step 4 % | [_____] % of Year |

| 6 | Total Working Capital Needed | Step 5 % x Total Operating Expenses (less depreciation) | $ [________________] |

IRS Response Cover Letter and Protest Document Format

When responding to an IRS inquiry regarding Section 531, the defense must present the Bardahl calculations, board resolutions, and statements of business needs as a cohesive, structured package. The cover letter must be professional, authoritative, and direct.

[Company Letterhead]

Date: [Insert Date]

Internal Revenue Service

Attn: [Examiner Name / Office Address]RE: Response to Notice of Proposed Assessment - Section 531 Accumulated Earnings Tax

Taxpayer: [Company Name]

EIN: [XX-XXXXXXX]

Tax Year(s): [Insert Tax Years under audit]Dear Examiner,

On behalf of [Company Name], we are writing to respectfully protest the proposed assessment of the Accumulated Earnings Tax under Section 531. The earnings retained by the corporation for the tax years under examination do not exceed the reasonable needs of the business as defined under Section 537.

Enclosed with this response is a comprehensive evidentiary packet proving that all retained capital is earmarked for specific, definite, and feasible business operations. This includes our completed Bardahl Formula Worksheet (proving our necessary operating cycle reserves), Board of Directors Resolutions, and formal Statements of Business Needs documenting our active capital improvement projects.

Please contact the undersigned at [Phone Number] if you require additional information or to schedule a conference to discuss this matter.

Sincerely,

[Signature]

[Name, Title / Authorized Representative]

Organizing the Supporting Documentation Index

A professional, organized submission increases the credibility of the corporation's defense and simplifies the examiner's review. Supporting evidence must be indexed in a logical, chronological, and thematic order to correspond directly with the Statements of Business Needs.

- Executive Summary: A narrative explanation of the business history, market conditions, and primary reasons for earnings retention.

- Calculations and Financial Analyses: Signed Bardahl Formula worksheets and comparative balance sheets showing working capital cycles.

- Corporate Governance Records: Chronological board meeting minutes and signed resolutions authorizing capital allocations.

- Third-Party Feasibility Studies: Appraisals, architectural plans, market analysis reports, and official vendor bids.

- Contractual Commitments: Executed purchase agreements, construction contracts, or joint venture letters of intent.

- Tax Return Reconciliations: Copies of Form 1120 schedules demonstrating historical patterns of dividend payouts or reinvestments.

Guidelines for Contemporaneous Recordkeeping and Annual Reviews

Corporate officers and tax professionals must realize that defensive documentation cannot be created retroactively during an audit. Corporate resolutions, Bardahl calculations, and business expansion plans must be reviewed, recalculated, and approved annually. Every year, prior to the close of the corporate taxable year, the board of directors must formally update their resolutions to reflect any changes in business plans or economic conditions. Maintaining this continuous, contemporaneous defense posture is the only reliable way to protect corporate capital from unexpected Section 531 tax liabilities.

Leave a comment