Navigating a dual-status tax year is notoriously complex, often leaving international taxpayers and their advisors struggling to reconcile overlapping resident and nonresident tax rules within a single calendar year. Before diving into the preparation process, it is critical to understand the IRS's intricate hybrid reporting framework, which demands splitting the tax year into two distinct residency periods with entirely different tax treatments.

Utilizing standardized tax return templates grants practitioners an immediate advantage, transforming a chaotic, manual compliance puzzle into a streamlined, repeatable workflow. However, we must stipulate that while these templates provide essential structural clarity, they serve as a foundation rather than a one-size-fits-all solution; individual treaty benefits and visa specifics must still be analyzed case-by-case. For example, a standard filing requires precisely coordinating a Form 1040 for the resident portion of the year with a clearly marked Form 1040-NR serving as the dual-status statement.

In this article, we will dissect the core mechanics of dual-status filings, analyze essential template structures, and outline a step-by-step methodology for executing these complex returns with absolute accuracy.

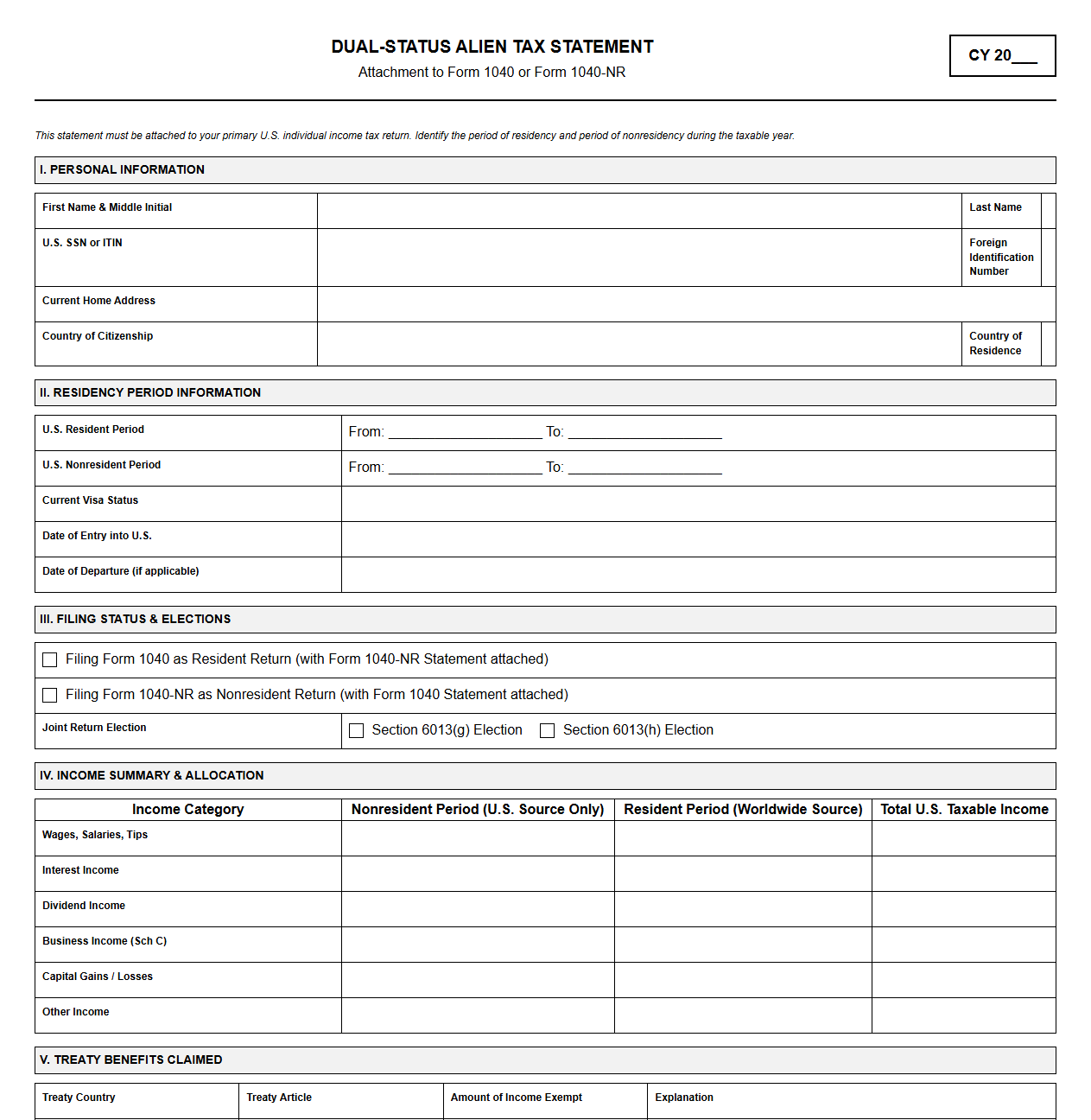

Dual-Status Alien Tax Return Template

Download: .PDF

Download: .PDF

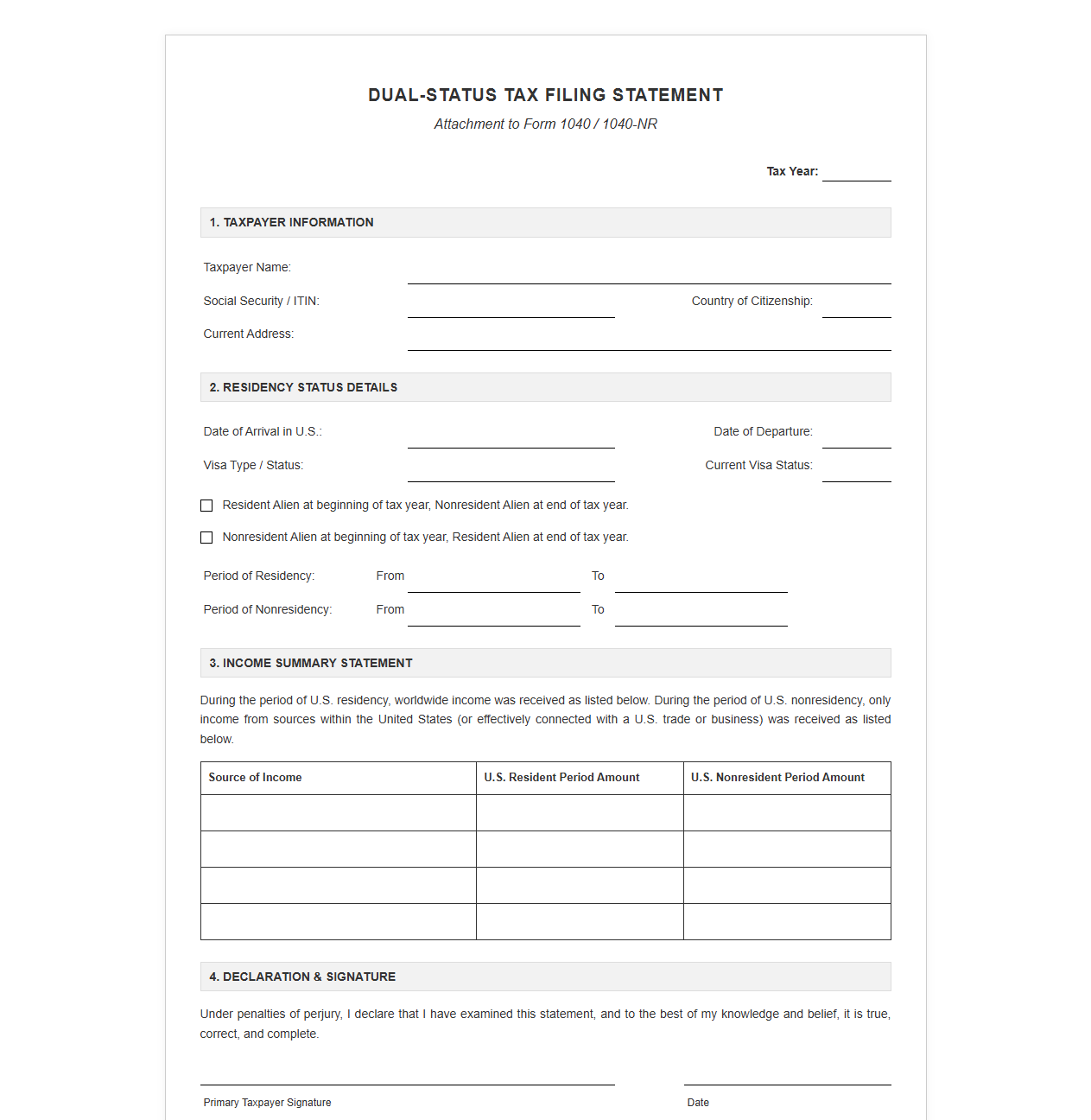

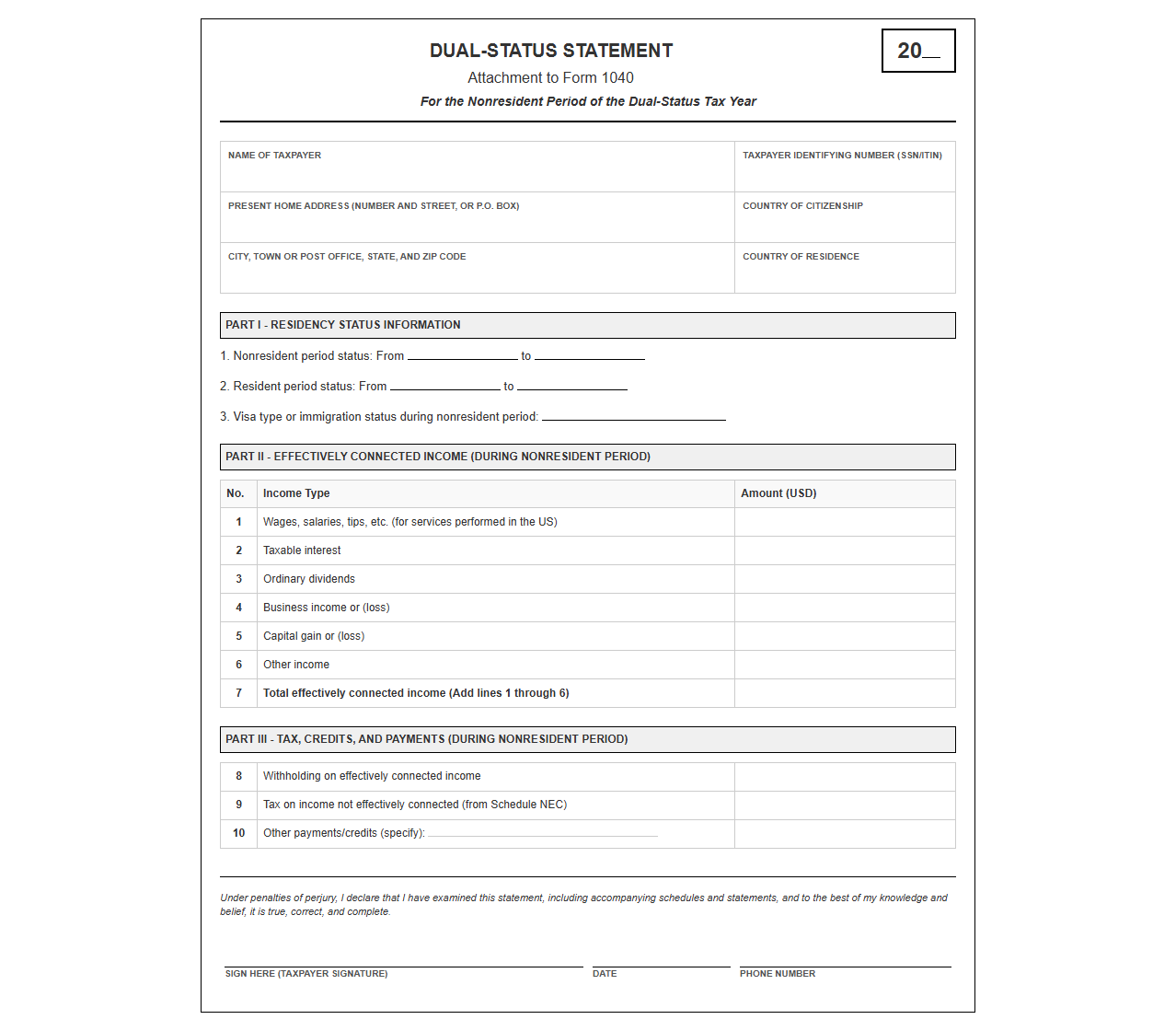

Dual-Status Tax Filing Statement Template

Download: .PDF

Download: .PDF

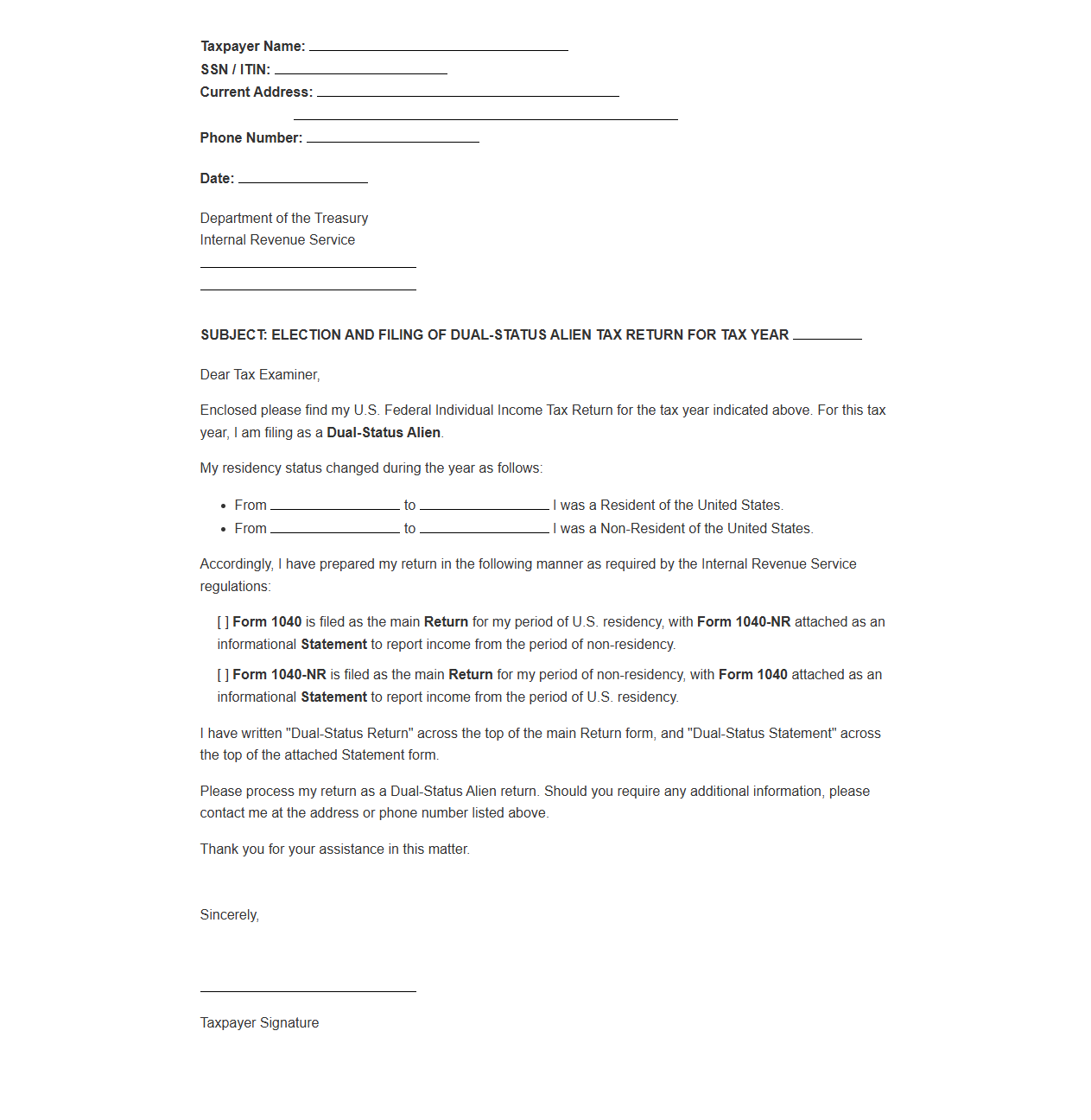

U.S. Dual-Status Alien Return Cover Letter Template

Download: .PDF

Download: .PDF

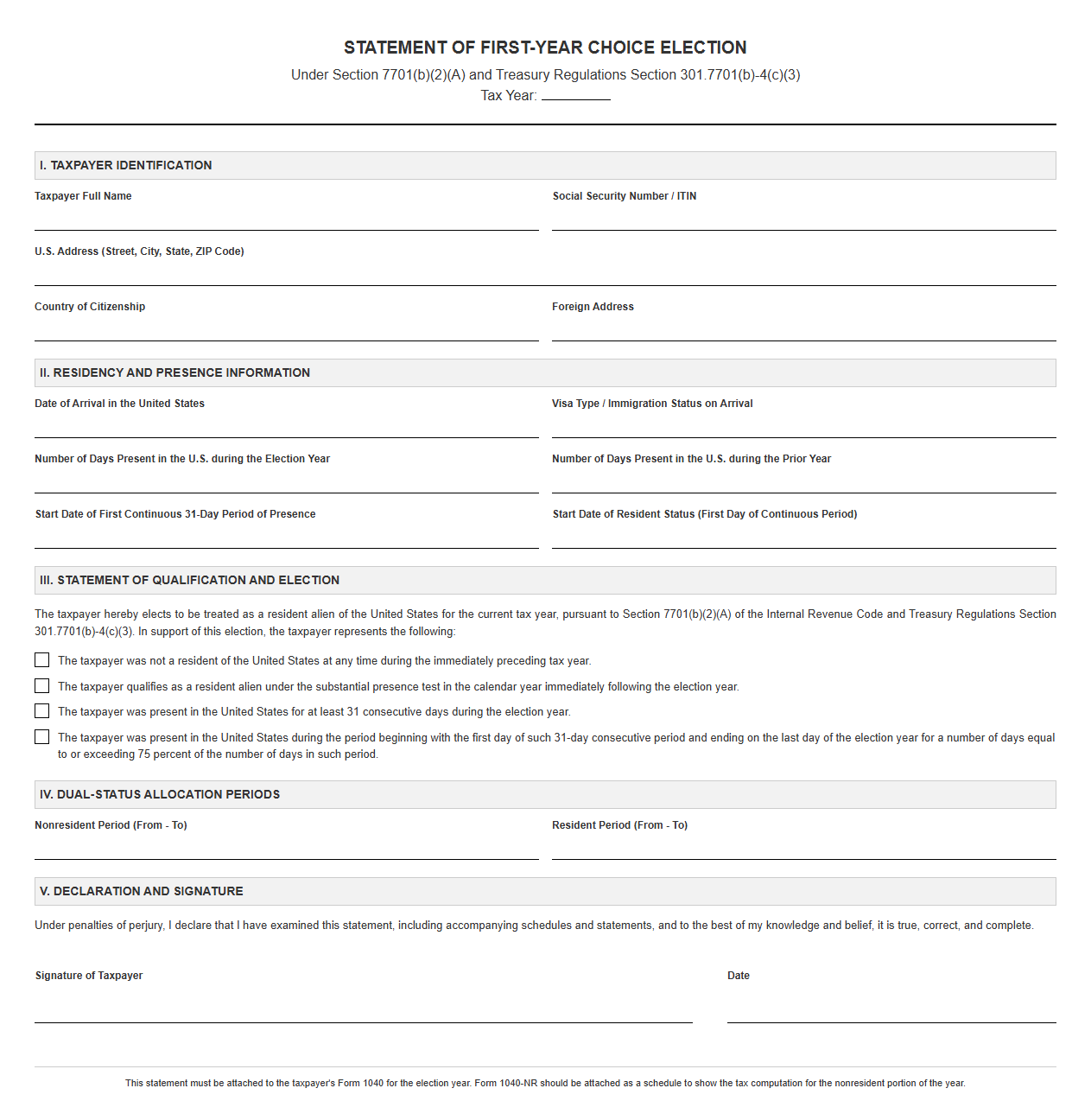

First-Year Choice Dual-Status Return Template

Download: .PDF

Download: .PDF

Dual-Status Alien Form 1040NR Attachment Template

Download: .PDF

Download: .PDF

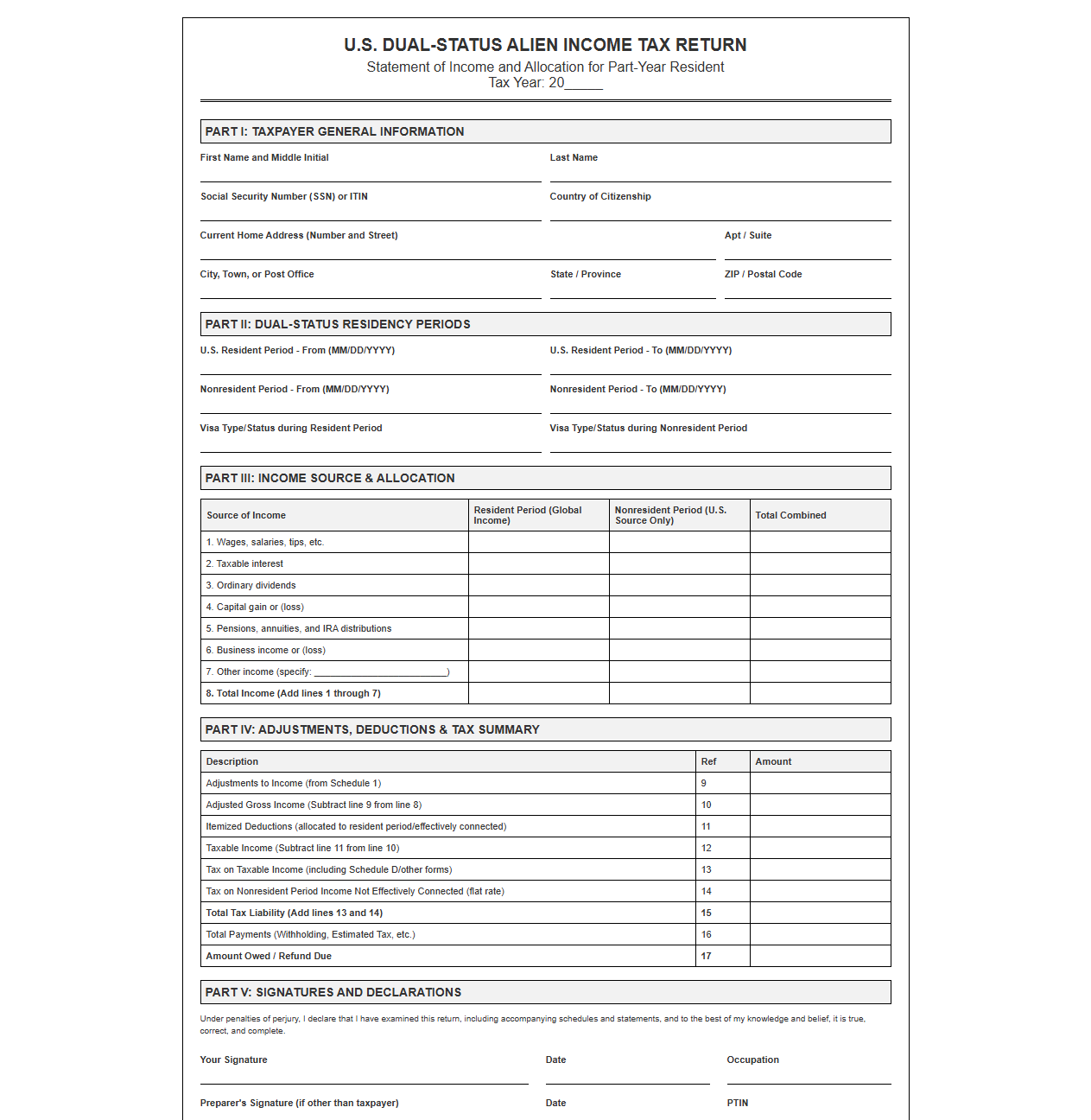

Part-Year Resident Dual-Status Alien Return Template

Download: .PDF

Download: .PDF

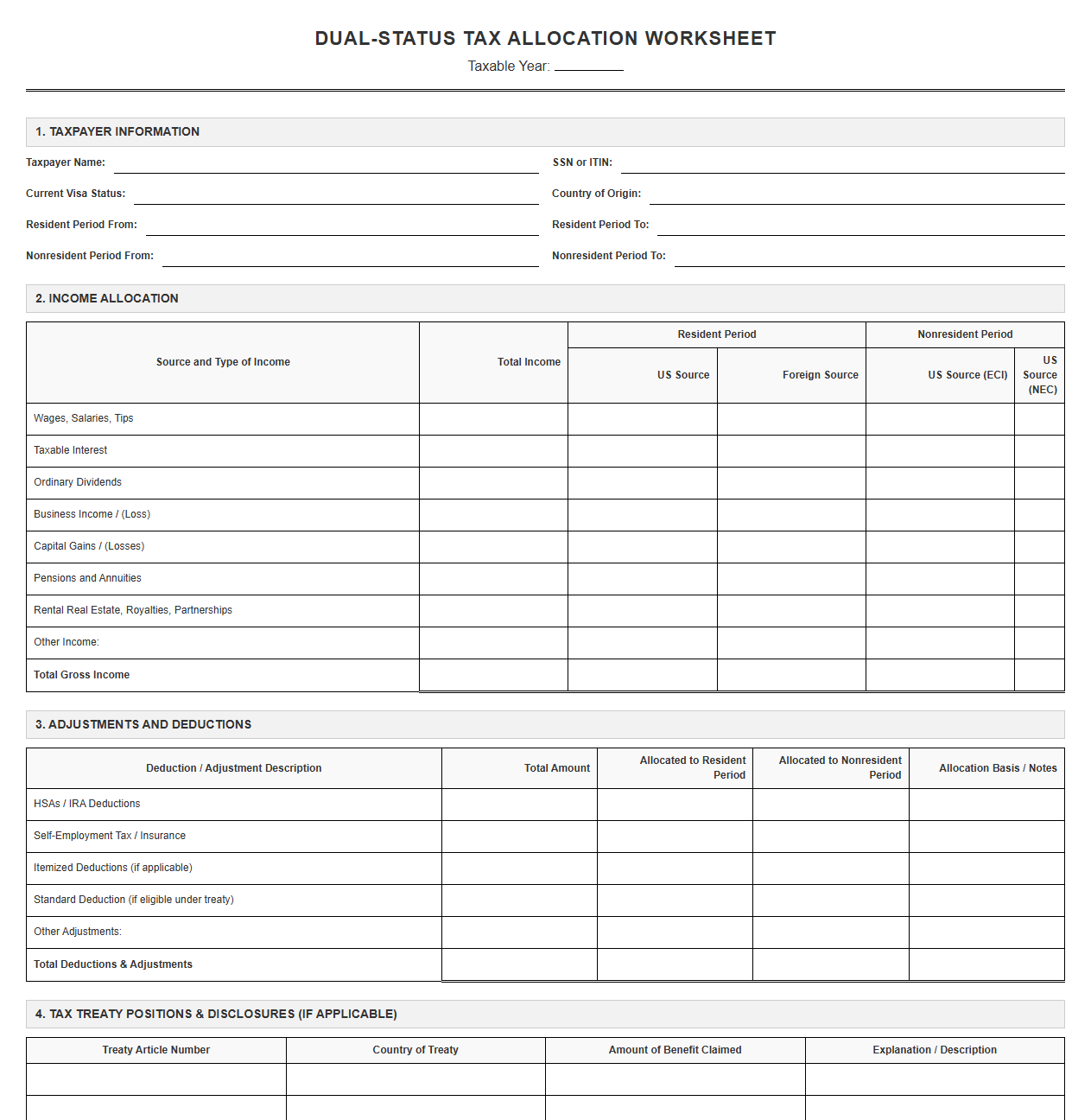

Dual-Status Tax Allocation Worksheet Template

Download: .PDF

Download: .PDF

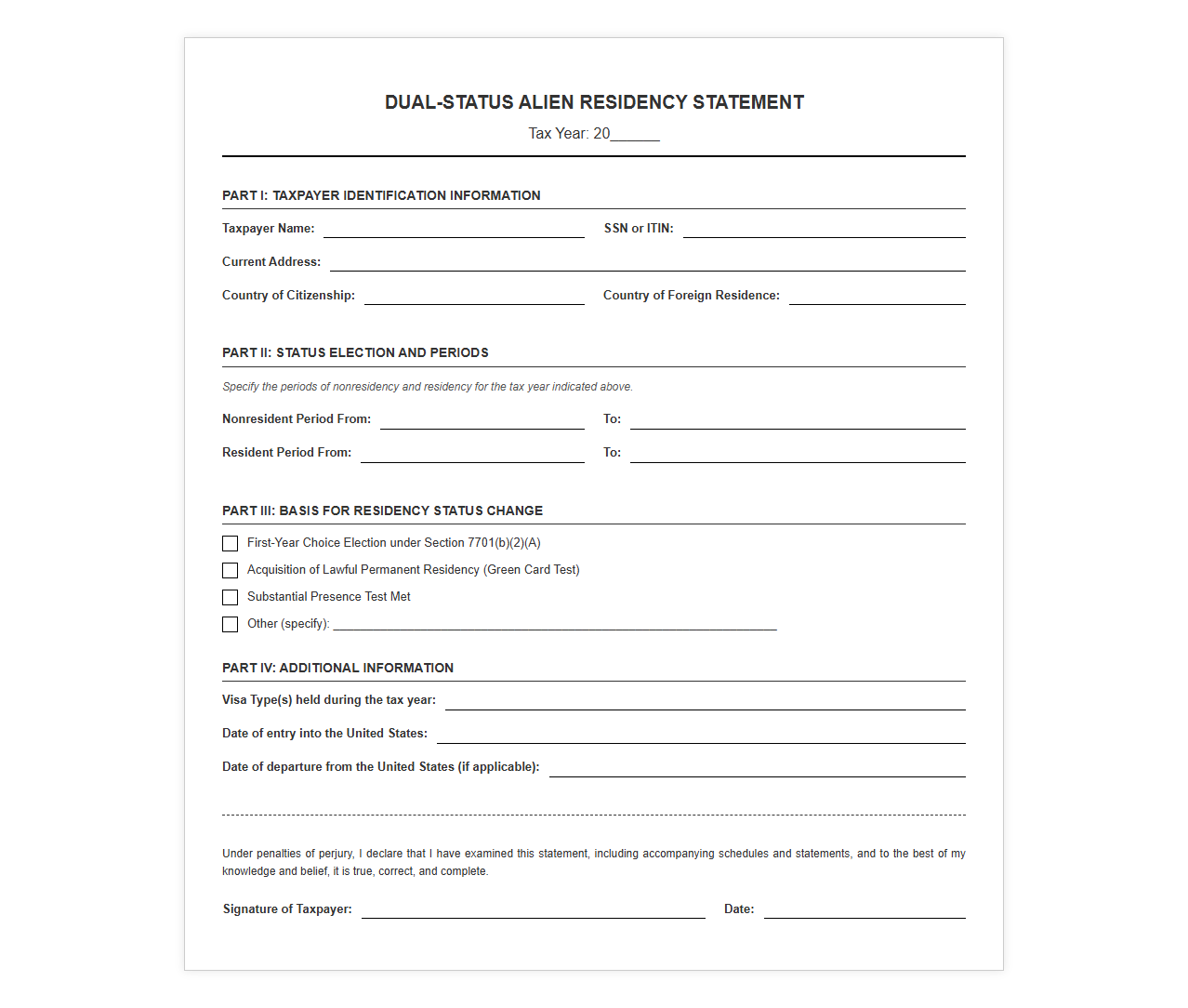

Dual-Status Alien Residency Statement Template

Download: .PDF

Download: .PDF

Demystifying the Dual-Status Alien Tax Status

Navigating the United States tax system can be challenging, but the complexity increases significantly for individuals classified as a dual-status alien. This unique tax designation applies to individuals who transition from being a nonresident alien to a resident alien, or vice versa, within a single calendar year. Because you hold both statuses during the same tax period, your tax year is effectively split into two distinct segments, each governed by an entirely different set of rules.

These filings are uniquely complex because they require you to apply separate income sourcing rules and calculation methods for each portion of the year. During your resident period, you are taxed on your worldwide income, whereas during your nonresident period, you are only taxed on income derived from U.S. sources. Merging these two distinct regimes into a single, cohesive tax return requires meticulous record-keeping and a deep understanding of tax residency transition rules.

Pinpointing Your Residency Transition Date

Determining the exact date you transition from one tax status to the other is the foundation of your dual-status tax return. This transition date determines when your worldwide income becomes subject to U.S. taxation.

Applying the Substantial Presence Test

To establish residency based on physical presence, the IRS uses a specific formula to measure your days in the United States over a three-year period. You become a resident alien on the first day you are physically present in the U.S. during the calendar year that you meet the Substantial Presence Test.

The calculation formula requires that the sum of your qualifying days equals or exceeds 183 days, calculated as follows:

Current Year Days + (1/3 * Prior Year Days) + (1/6 * Year Before That) >= 183 days

Electing the First-Year Choice

If you do not meet the Substantial Presence Test in your transition year but will meet it in the following year, you may be eligible to make the First-Year Choice. This allows you to elect to be treated as a dual-status resident for the portion of the transition year after you arrived in the U.S.

To qualify, you must be physically present in the U.S. for at least 31 consecutive days during the transition year, and present in the U.S. for at least 75% of the days from the start of that 31-day period to the end of the year.

The Dual-Return Architecture: Form 1040 vs. Form 1040-NR

A dual-status tax filing does not mean you file two separate tax returns that are processed independently. Instead, it requires a dual-return architecture where one form serves as your primary return and the other serves as an informational attachment (often referred to as a "statement"). The role of each form depends entirely on your residency status on the last day of the tax year.

- Resident at Year-End: If you are a U.S. resident on December 31, you must file Form 1040 as your primary tax return. You must then attach Form 1040-NR as a statement to report the income earned during the nonresident portion of the year.

- Nonresident at Year-End: If you are a nonresident on December 31, you must file Form 1040-NR as your primary tax return. You then attach a statement (which can be Form 1040) showing the income and deductions attributable to your resident portion of the year.

Crucial Tax Restrictions and Forfeitures

Taxpayers filing as dual-status aliens face strict limitations. The IRS disallows several valuable tax breaks and filing statuses that are normally available to full-year residents.

For example, dual-status taxpayers cannot claim the standard deduction, meaning you must itemize your deductions if you wish to write off qualified personal expenses. Furthermore, you are generally prohibited from choosing the "Married Filing Jointly" status, which often forces married couples to file separate returns at higher tax brackets.

IRS Warning: A dual-status taxpayer cannot claim the standard deduction. Your itemized deductions cannot exceed your income for the period of residency. Additionally, you cannot file as Married Filing Jointly unless you make a special, permanent election to be treated as a full-year resident, which subjects your worldwide income for the entire year to U.S. tax.

Step-by-Step Template: Reporting the Resident Period Income

During the portion of the year when you are considered a U.S. resident alien, you are subject to the same tax rules as a U.S. citizen. Use the following structured approach to report your finances for this specific period:

- Identify Worldwide Income: Gather documentation for all income earned globally during your resident period, including foreign wages, foreign investment income, and U.S.-sourced earnings.

- Prorate Allowable Deductions: Calculate deductions that can be directly attributed to your period of residency, such as home mortgage interest, state taxes paid, or charitable contributions made during this timeframe.

- Apply Applicable Tax Credits: Claim eligible credits, such as the Child Tax Credit or Child and Dependent Care Credit, ensuring they are calculated only on income and expenses relevant to your residency period.

- Translate Foreign Currency: Convert all foreign income earned during this period into U.S. dollars using the prevailing treasury exchange rates on the dates the income was received.

Step-by-Step Template: Reporting the Nonresident Period Income

For the portion of the year when you were a nonresident alien, you are taxed only on income from sources within the United States. This income is divided into two categories: Effectively Connected Income (ECI) and Fixed, Determinable, Annual, Alterable, Periodical (FDAP) income.

Use the following table to determine how to source and report different types of income during your nonresident window:

| Income Type | Sourcing Rules | Tax Rate & Reporting |

|---|---|---|

| Wages for U.S. Services | Sourced where the work was physically performed. | Taxed at graduated rates as Effectively Connected Income (ECI). |

| U.S. Dividends | Sourced by the location of the paying corporation. | Taxed at a flat 30% (FDAP) or lower tax treaty rate. |

| Foreign Wages | Sourced outside the U.S. (where work was performed). | Not subject to U.S. taxation during the nonresident period. |

| U.S. Real Estate Income | Sourced where the property is physically located. | Taxed at 30% flat unless an election is made to treat as ECI. |

Final Assembly, Signing, and Mailing Protocols

Once you have prepared both returns, you must physically assemble them according to strict IRS guidelines to prevent processing errors and delays.

If you are a resident at the end of the year, place your completed Form 1040 on top. Fill out your personal details and complete the calculations. On the top of the first page of your Form 1040-NR statement, clearly write or type the words "Dual-Status Statement" in bold letters. Staple this statement to the back of your Form 1040. You must sign and date the Form 1040. The attached statement does not require a separate signature, but it must clearly show your name, address, and Taxpayer Identification Number (TIN).

Leave a comment