Dissolving a business partnership is often fraught with administrative stress, particularly when trying to untangle shared liabilities and satisfy final tax obligations without triggering costly audits. Before distributing remaining assets, partners must first establish a clear, legally compliant paper trail that accurately accounts for every capital account and outstanding debt.

Utilizing structured templates grants partners the exact administrative blueprint needed to accelerate this winding-up process, reducing friction and safeguarding individual financial interests. However, it is important to stipulate that while these templates streamline the preparation of crucial documents-such as the final IRS Form 1065, Schedule K-1 distributions, and asset allocation worksheets-they function as organizational aids rather than a replacement for bespoke legal counsel.

In this guide, we will explore the essential dissolution templates required for a clean break, detailing how to deploy them to ensure a seamless, legally compliant wind-up.

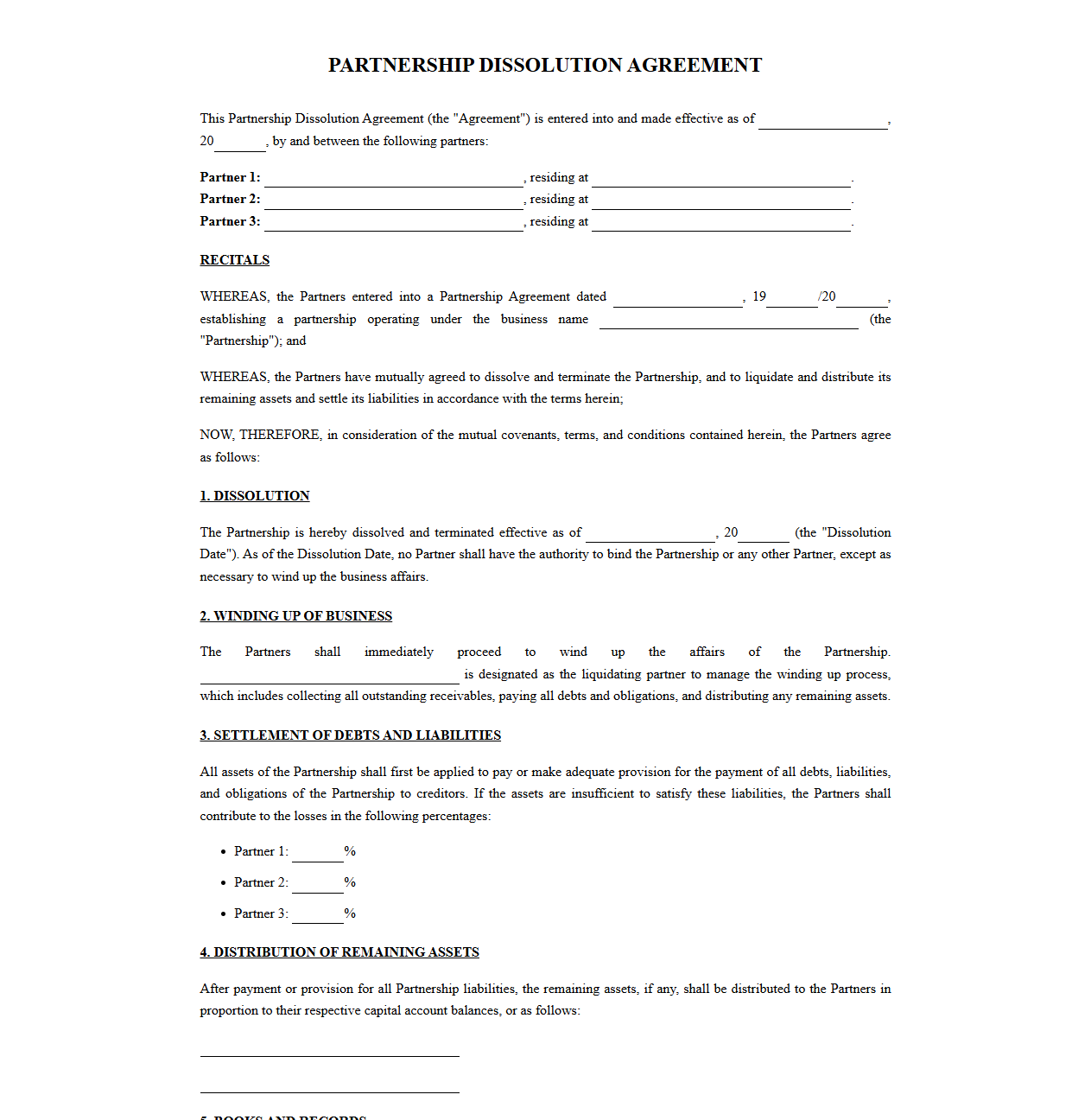

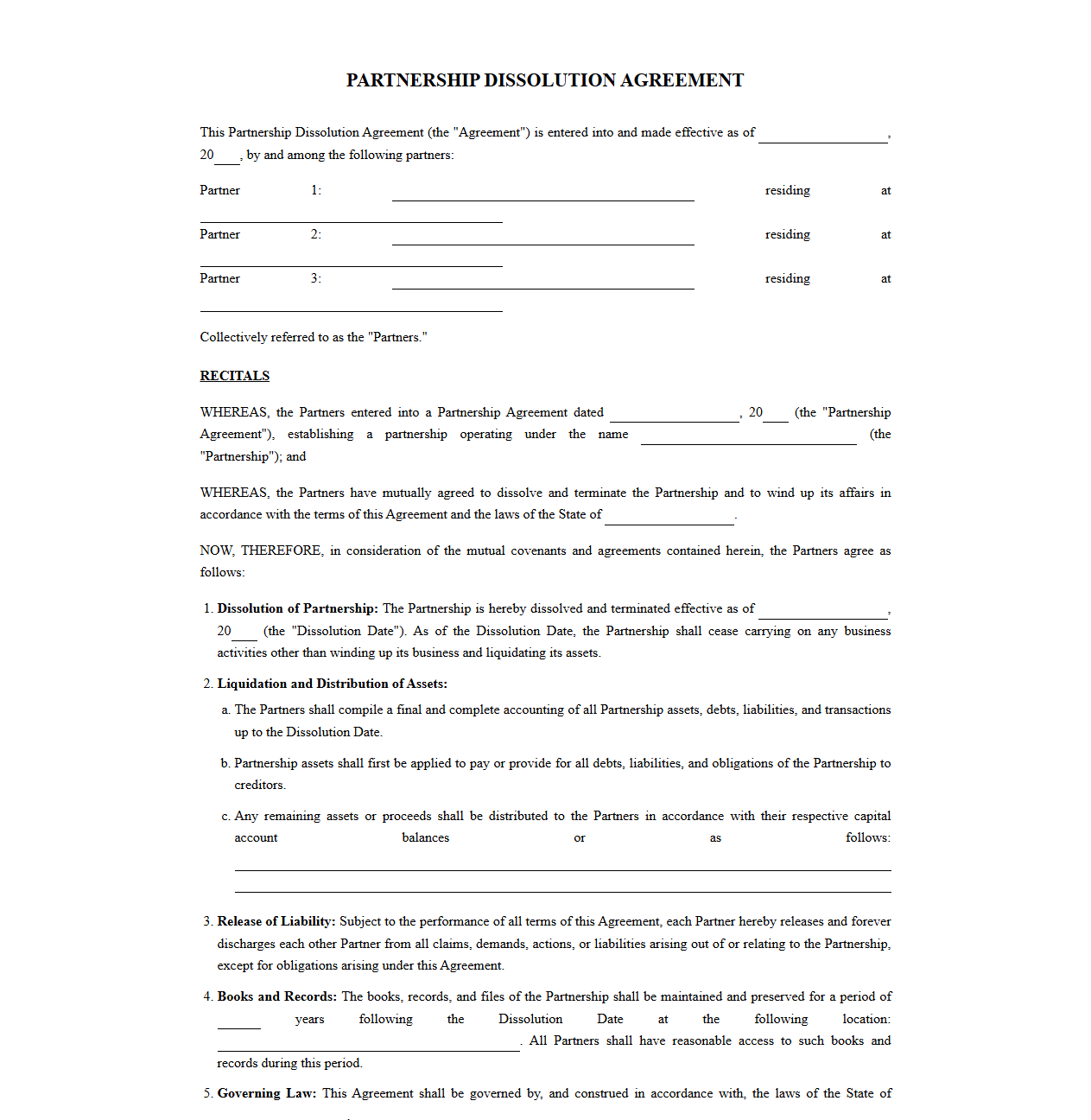

Partnership Dissolution Agreement Template

Download: .PDF

Download: .PDF

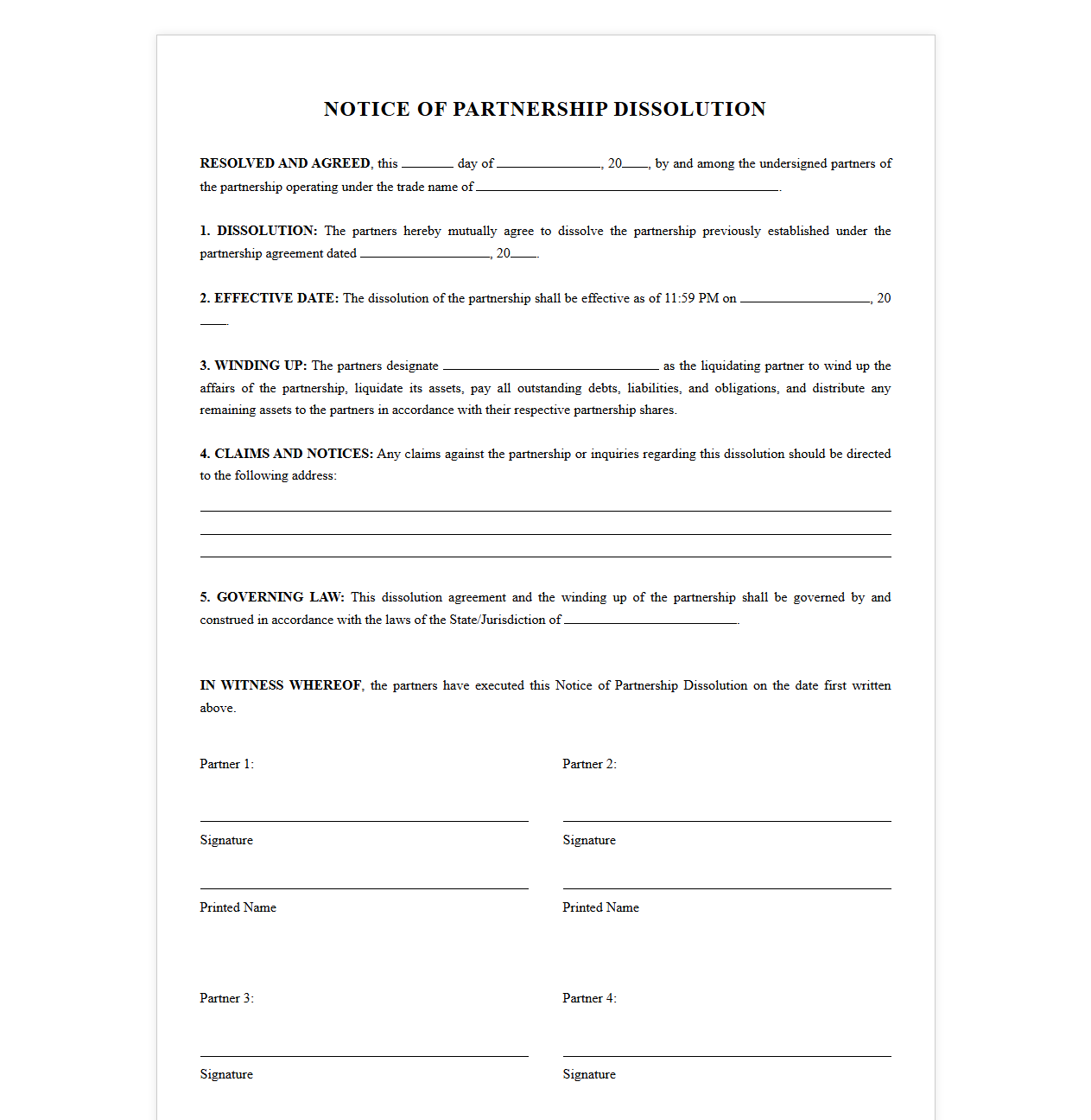

Notice of Partnership Dissolution Form

Download: .PDF

Download: .PDF

Partnership Termination Agreement Document

Download: .PDF

Download: .PDF

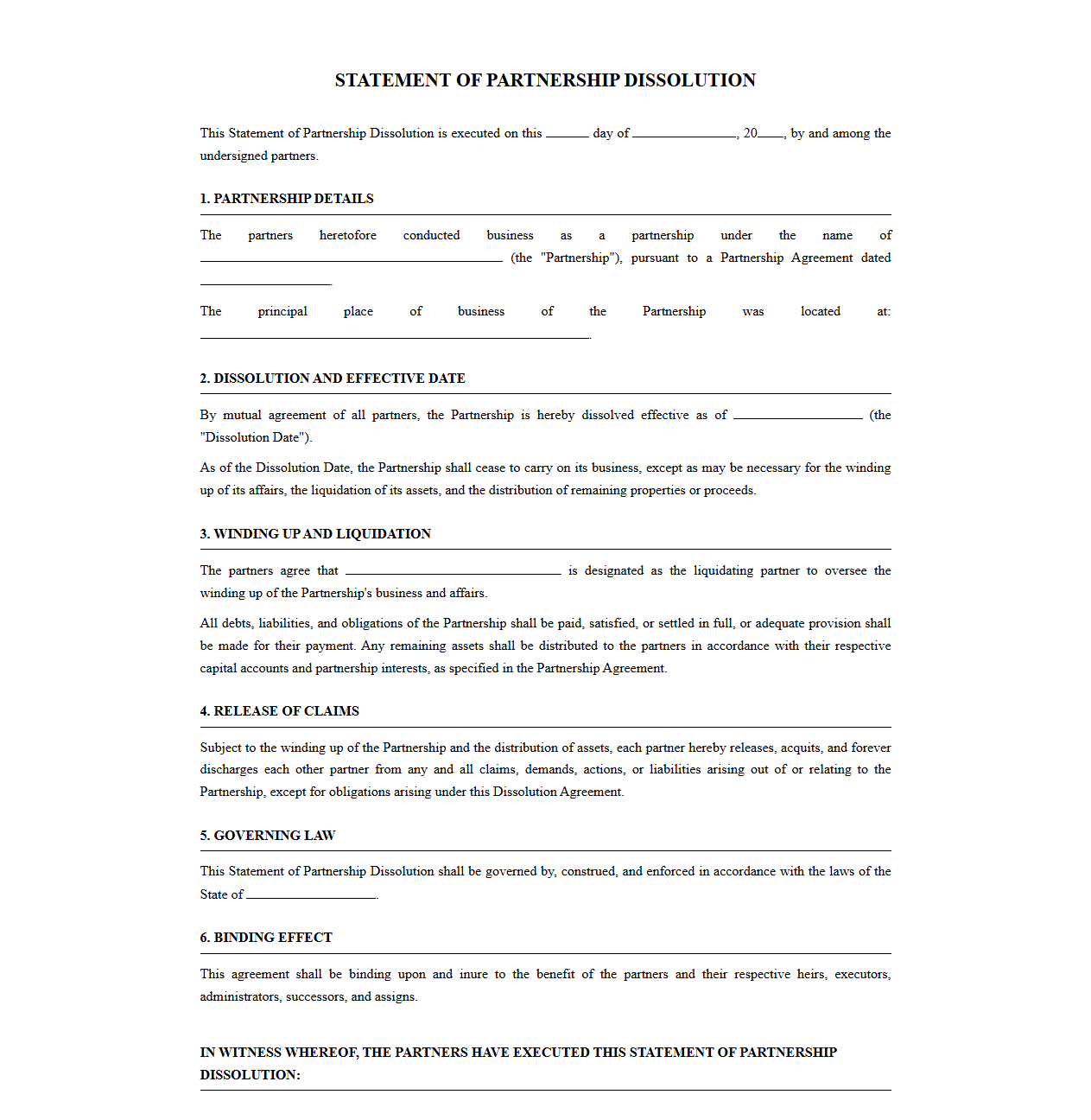

Statement of Partnership Dissolution Template

Download: .PDF

Download: .PDF

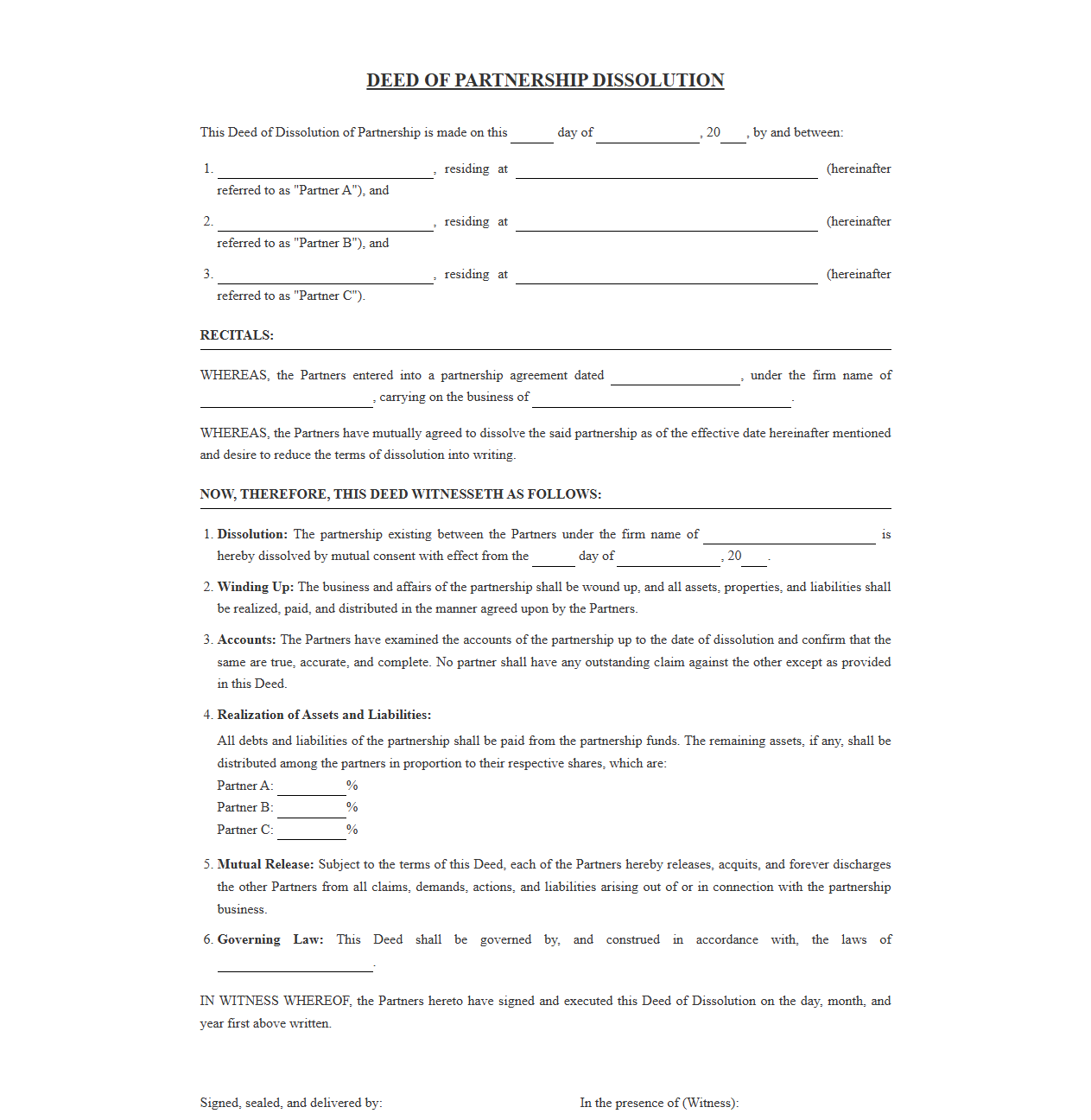

Partnership Dissolution Deed Template

Download: .PDF

Download: .PDF

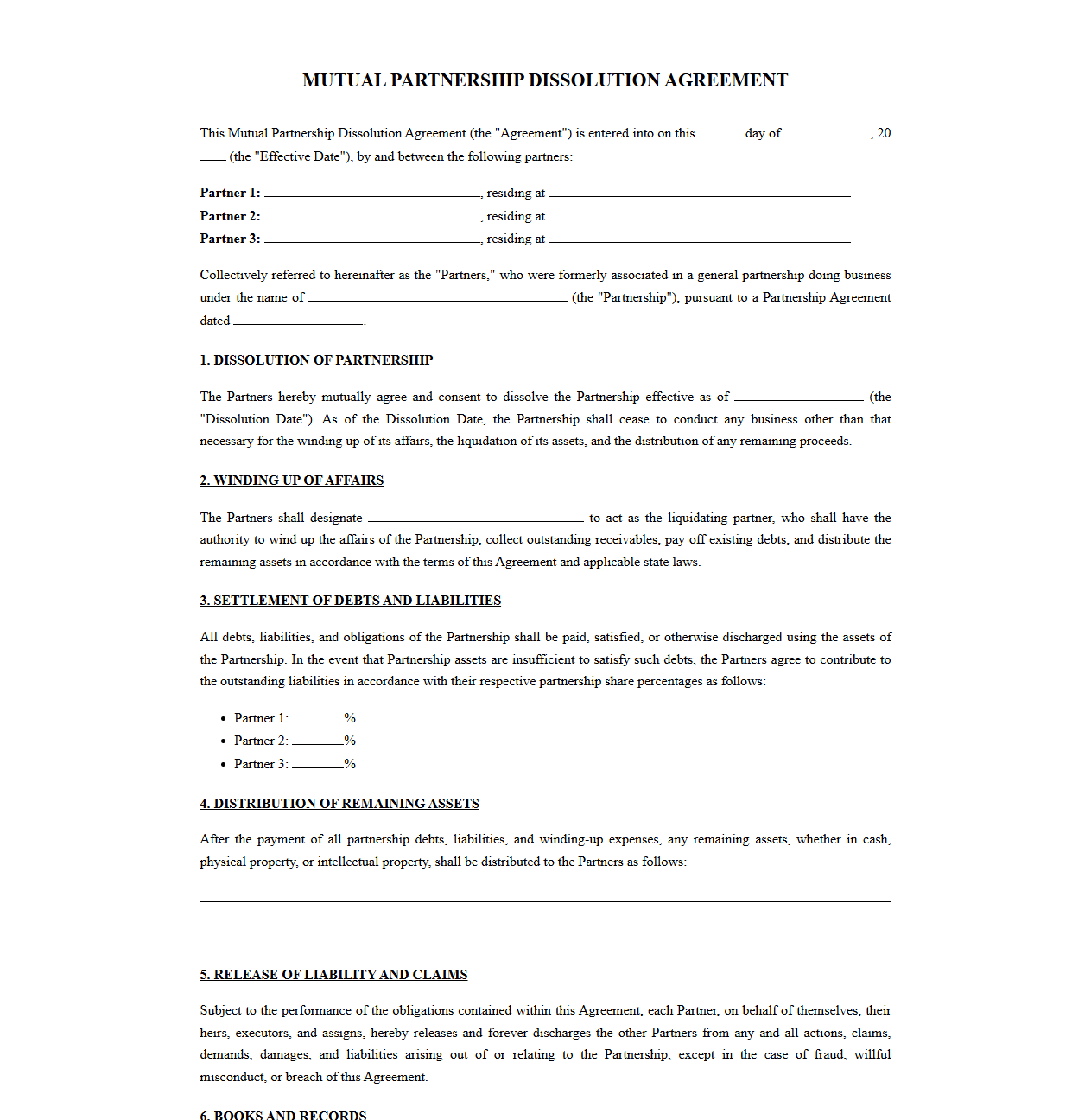

Mutual Partnership Dissolution Agreement Form

Download: .PDF

Download: .PDF

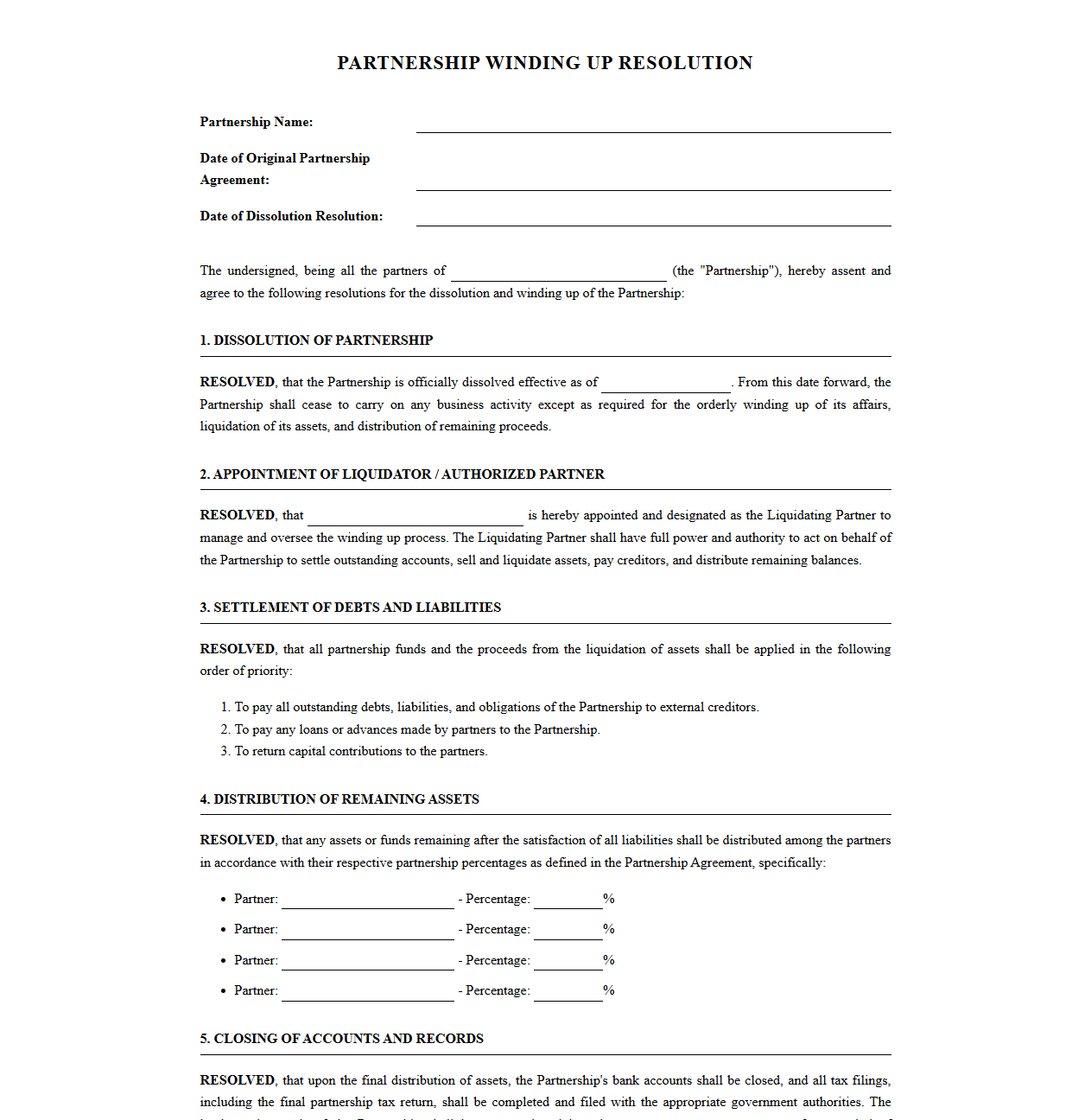

Partnership Winding Up Resolution Template

Download: .PDF

Download: .PDF

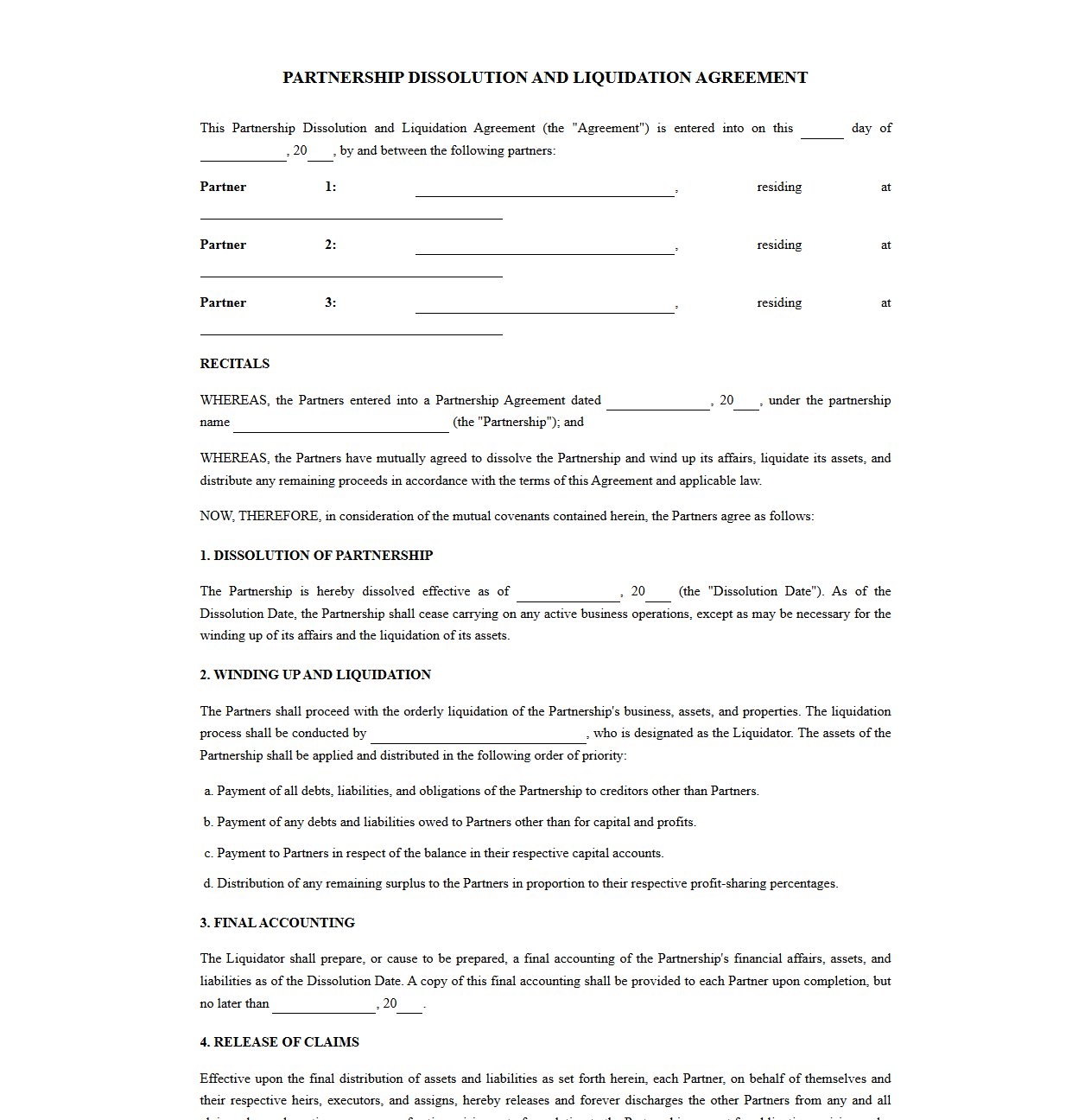

Partnership Dissolution and Liquidation Agreement

Download: .PDF

Download: .PDF

Navigating the Final Chapter: Understanding Partnership Dissolution Returns

Closing the doors of a business is a significant milestone that requires careful administrative closure. A partnership dissolution return is the final tax filing submitted to the IRS when a partnership officially winds up its operations. This return is not just a formality; it is a legal requirement that formally notifies tax authorities that the business entity is no longer active. By executing this process correctly, partners ensure a clean break, protecting themselves from future liabilities, unresolved tax obligations, and potential audits. Properly winding down the business ensures that all parties can move forward with absolute peace of mind.

Crucial Tax Forms and Schedules for Business Winding-Up

To formally dissolve a partnership, specific tax documents must be prepared and filed with the IRS. The central document in this process is Form 1065 (U.S. Return of Partnership Income).

- Form 1065: This is the main partnership return where all final income, deductions, gains, and losses are reported for the short tax year.

- Schedule K-1: This is the critical form distributed to each partner, reporting their final distributive share of the partnership's economic activity.

- Schedule L, M-1, and M-2: These schedules show the final balance sheets and reconciliation of partner capital accounts, which must align perfectly upon dissolution.

The Step-by-Step Checklist for a Seamless Dissolution Process

A successful business wind-down requires a systematic approach. Partners should follow this chronological checklist to ensure all financial and legal bases are covered before submitting the final tax return:

- Settle outstanding debts: Pay off all creditors, suppliers, and outstanding loans using available business funds.

- Liquidate business assets: Sell off inventory, equipment, and real estate, or distribute them directly to the partners as agreed.

- Prepare final financial statements: Generate accurate balance sheets and income statements that reflect zero remaining balances.

- Distribute remaining capital: Return any leftover cash or assets to the partners based on their capital account balances.

- File the final tax return: Submit Form 1065 and issue the final Schedule K-1s within the required federal timeline.

Reconciling Capital Accounts and Distributing Remaining Assets

Before a partnership can officially close its books, the partner capital accounts must be reconciled to zero. This process ensures that all partners receive an equitable distribution of the remaining assets, strictly in accordance with the rules established in the partnership agreement. Each partner's capital account is adjusted for final profits, losses, and distributions. Once these reconciliations are complete, any remaining cash or physical assets are distributed, bringing the capital account balances of all partners to exactly zero.

Marking the Return as Final: Filing Best Practices

When filing the final Form 1065, you must explicitly notify the IRS that this is the last tax return the partnership will ever file. Failing to do so can result in the IRS expecting future returns and assessing late-filing penalties.

To properly execute this, you must check the "Final Return" box in Box G on page 1 of Form 1065, and additionally check the "Final K-1" box at the top of each partner's Schedule K-1.

The timeline for submission is also critical: the final return is generally due by the 15th day of the third month following the date the partnership officially dissolved.

Common Pitfalls to Avoid During Partnership Dissolution

Even experienced business owners can make critical mistakes during the winding-up phase. Avoiding these common pitfalls will save time and prevent future legal headaches:

- Ignoring state-level dissolution: Many partners forget to file formal articles of dissolution with their state's Secretary of State, leaving the entity open to state taxes and annual fees.

- Failing to cancel the EIN: The business's Employer Identification Number must be closed with the IRS to prevent unauthorized use or identity theft.

- Neglecting final payroll taxes: If the partnership had employees, all final payroll tax returns must be filed and outstanding payroll taxes paid in full.

Streamlining the Process with Essential Dissolution Return Templates

Navigating the administrative steps of winding up a business can feel overwhelming, but you do not have to build your system from scratch. Utilizing professional resources can make the transition smooth and error-free. We recommend using our complimentary dissolution templates and checklists to organize your financial data, track steps, and coordinate efficiently with your tax professional. Taking advantage of these tools ensures total compliance and guarantees that no detail is overlooked during this final transition.

Leave a comment