Reconciling contra accounts is a notorious bottleneck for finance departments, where minor balance discrepancies can quickly delay month-end closing and compromise financial integrity. Before addressing these errors, organizations must first confront the limitations of traditional ledger frameworks, which often fail to capture the nuanced, offsetting relationship between primary assets and their contra counterparts.

Transitioning to standardized statement templates grants accounting teams immediate structural clarity, significantly reducing the time spent hunting down variance errors. To leverage these templates effectively, however, it is critical to stipulate that their success depends on consistent ledger hygiene and precise data mapping.

Whether you are balancing Accumulated Depreciation against fixed assets or adjusting the Allowance for Doubtful Accounts, utilizing dedicated templates provides concrete proof of financial accuracy. Below, we outline the exact architecture of diverse contra accounts and provide customizable templates to streamline your reconciliation workflow.

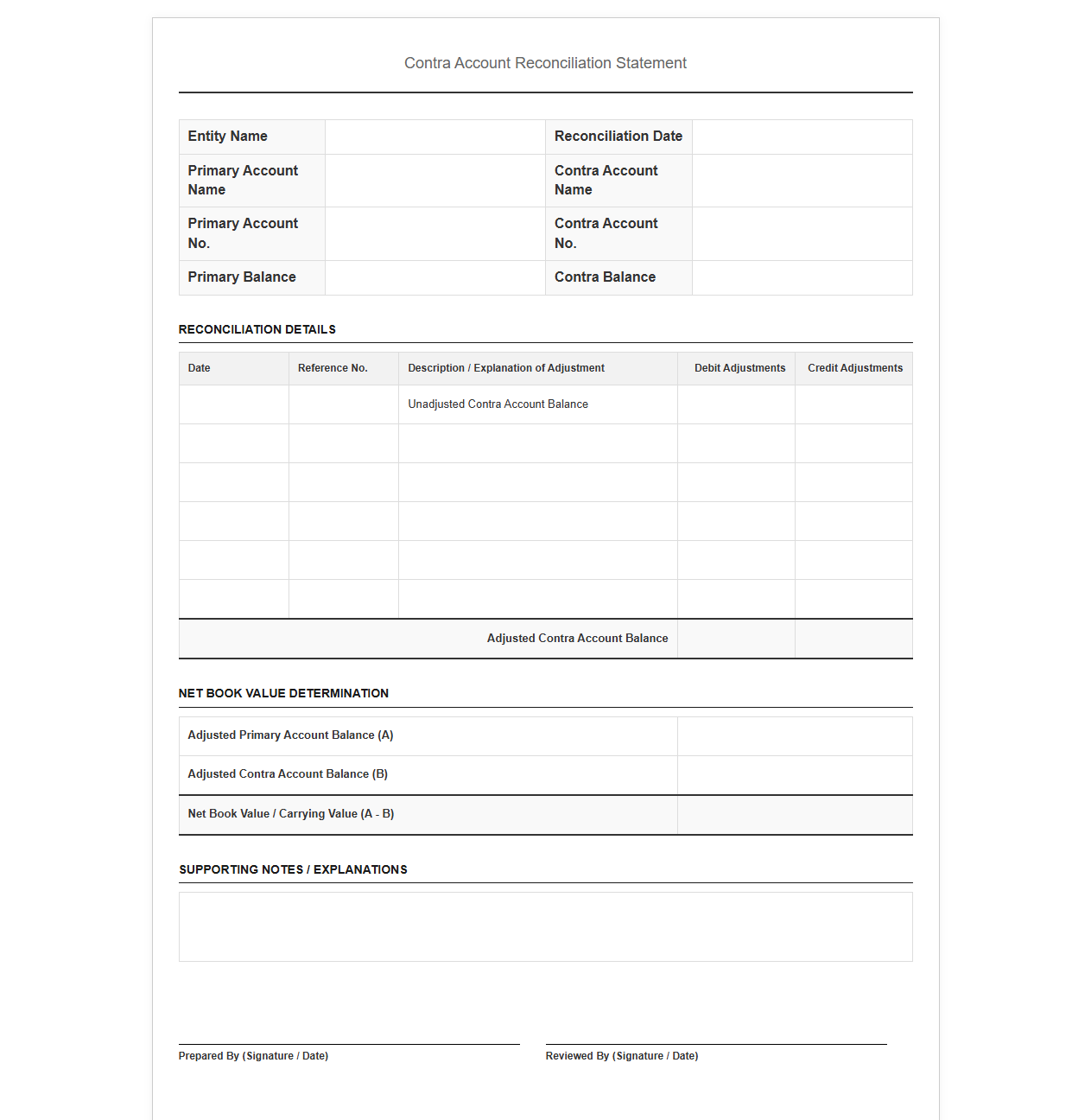

Contra Account Reconciliation Statement Template

Download: .PDF

Download: .PDF

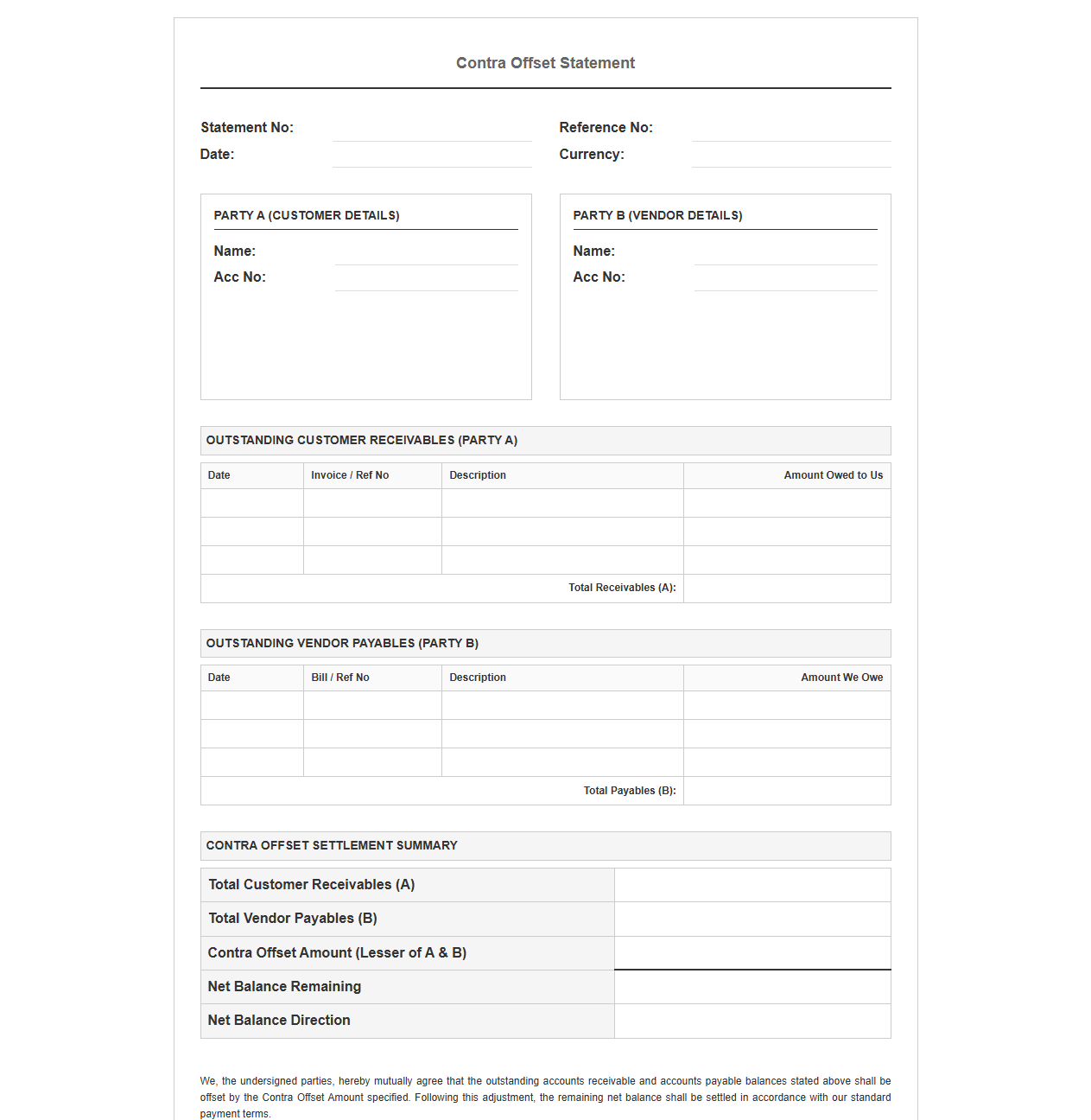

Customer and Vendor Contra Offset Statement

Download: .PDF

Download: .PDF

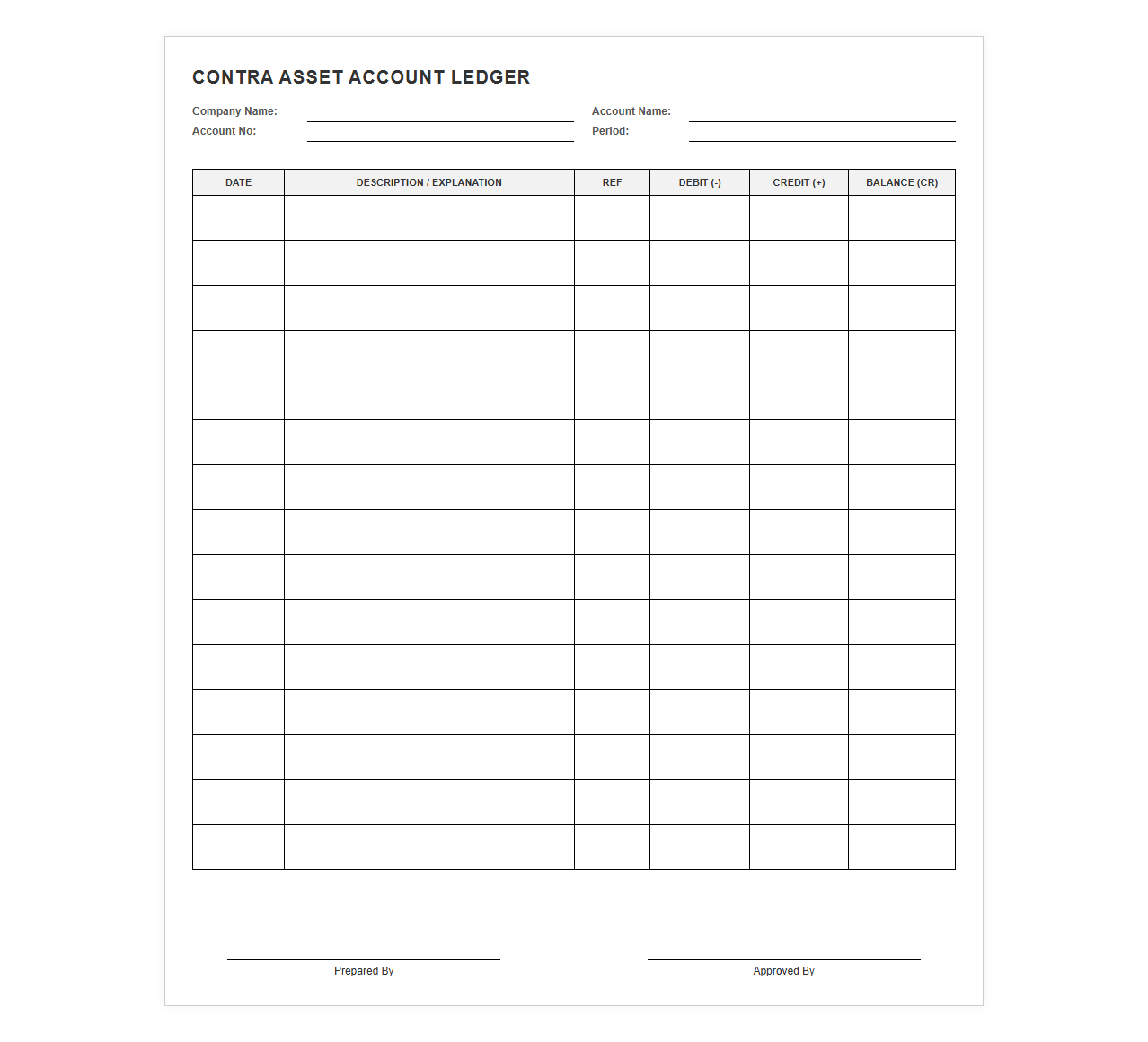

Contra Asset Account Ledger Statement Template

Download: .PDF

Download: .PDF

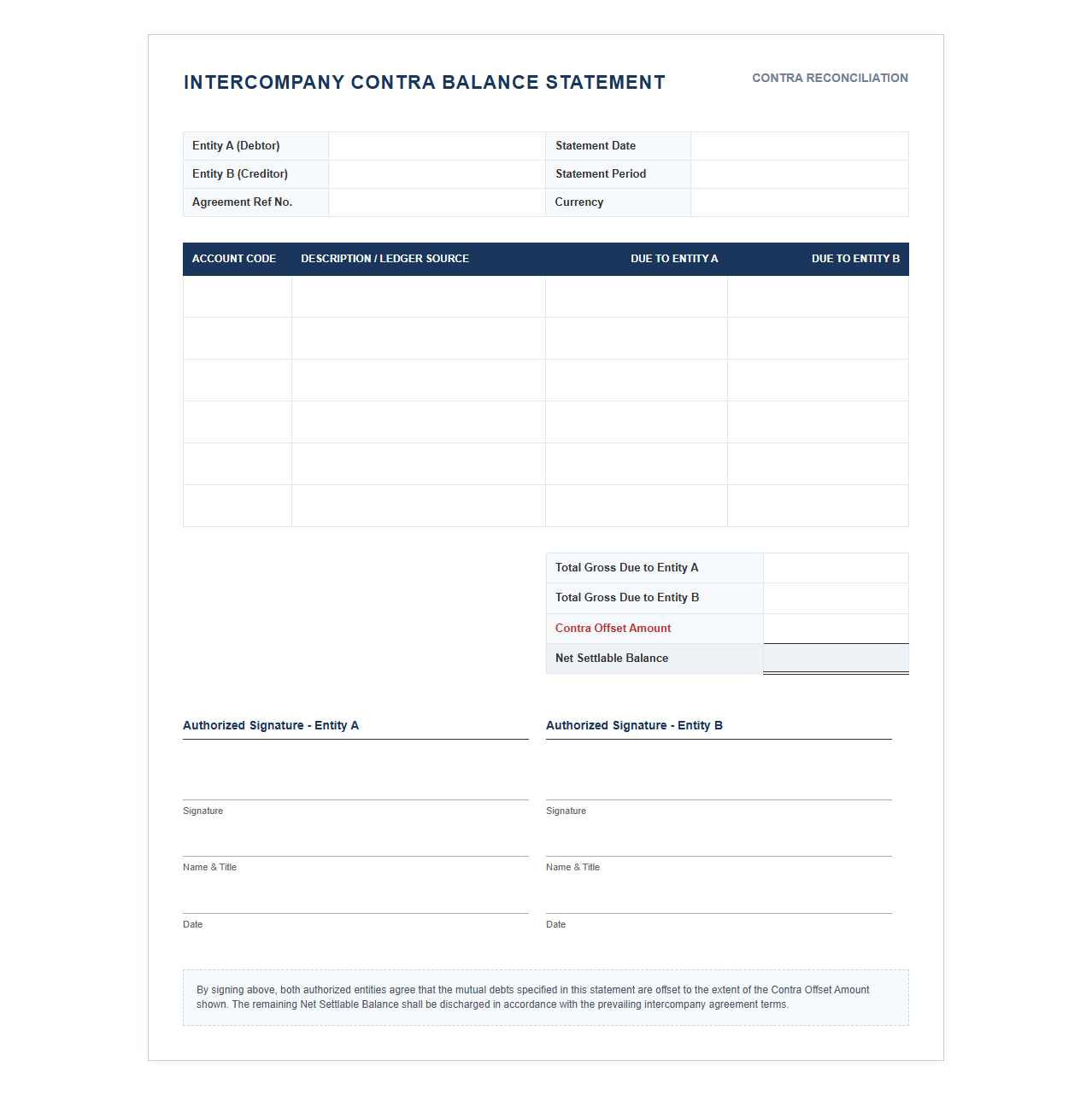

Intercompany Contra Balance Statement Document

Download: .PDF

Download: .PDF

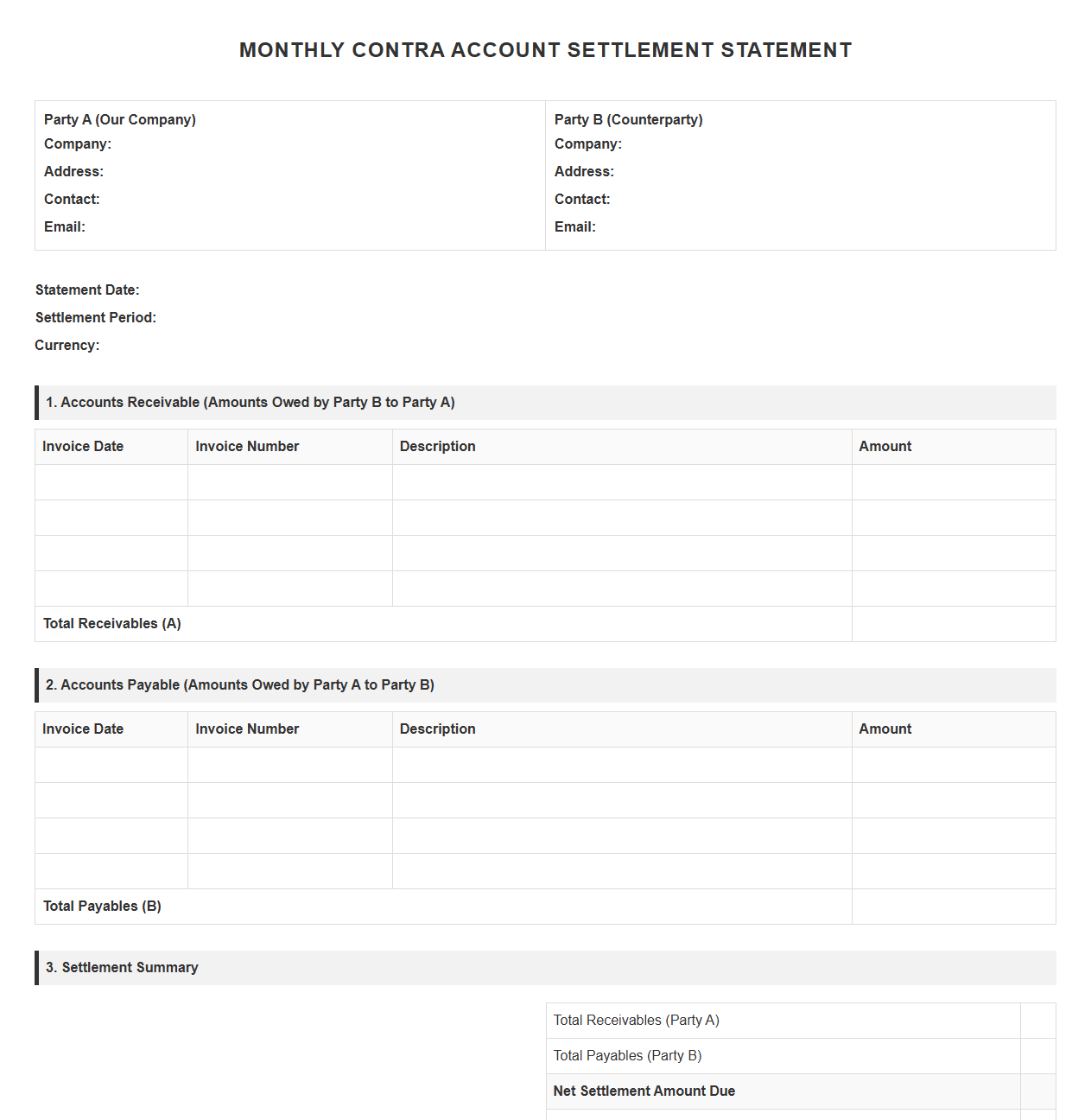

Monthly Contra Account Settlement Statement Template

Download: .PDF

Download: .PDF

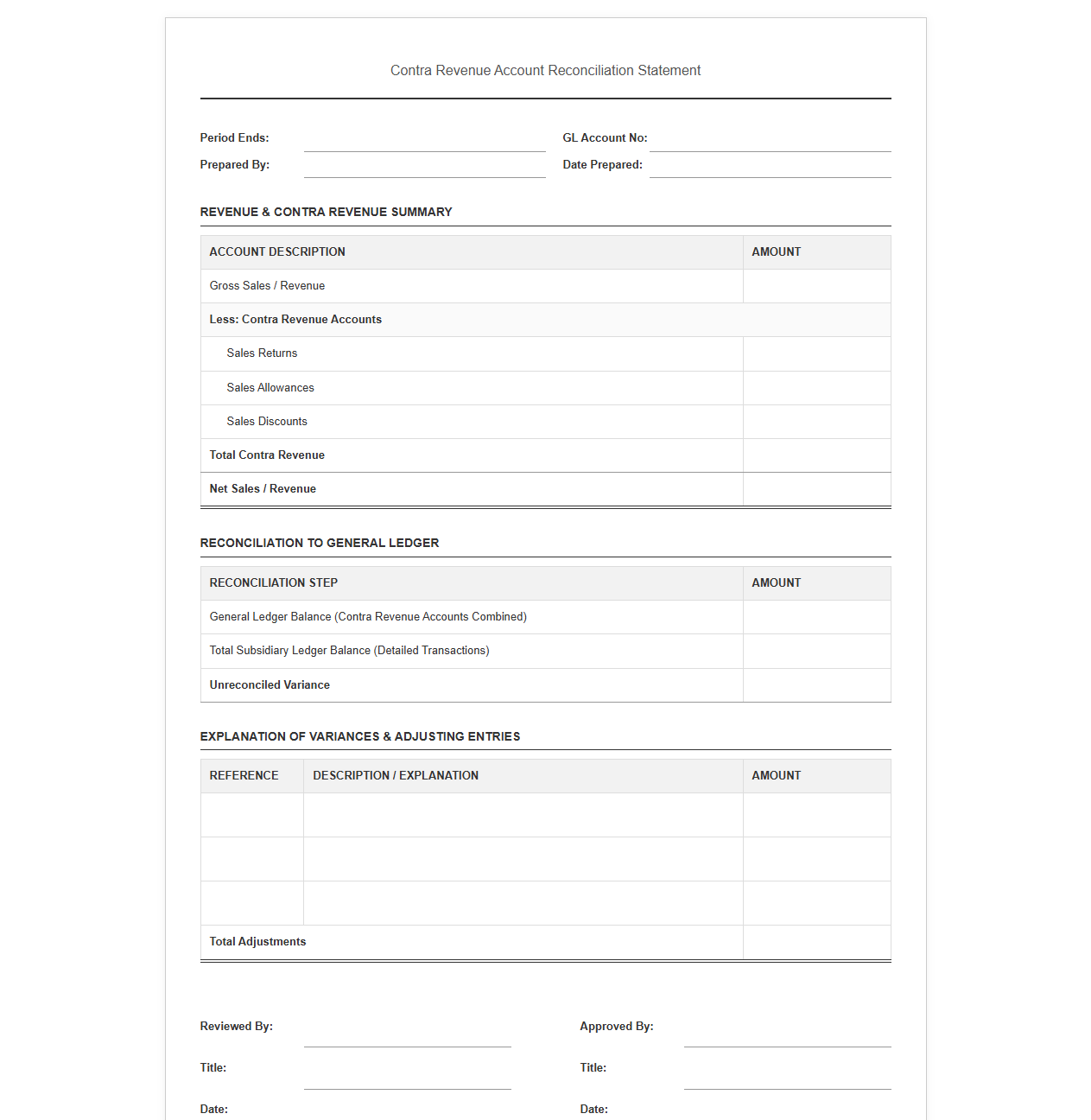

Contra Revenue Account Reconciliation Statement

Download: .PDF

Download: .PDF

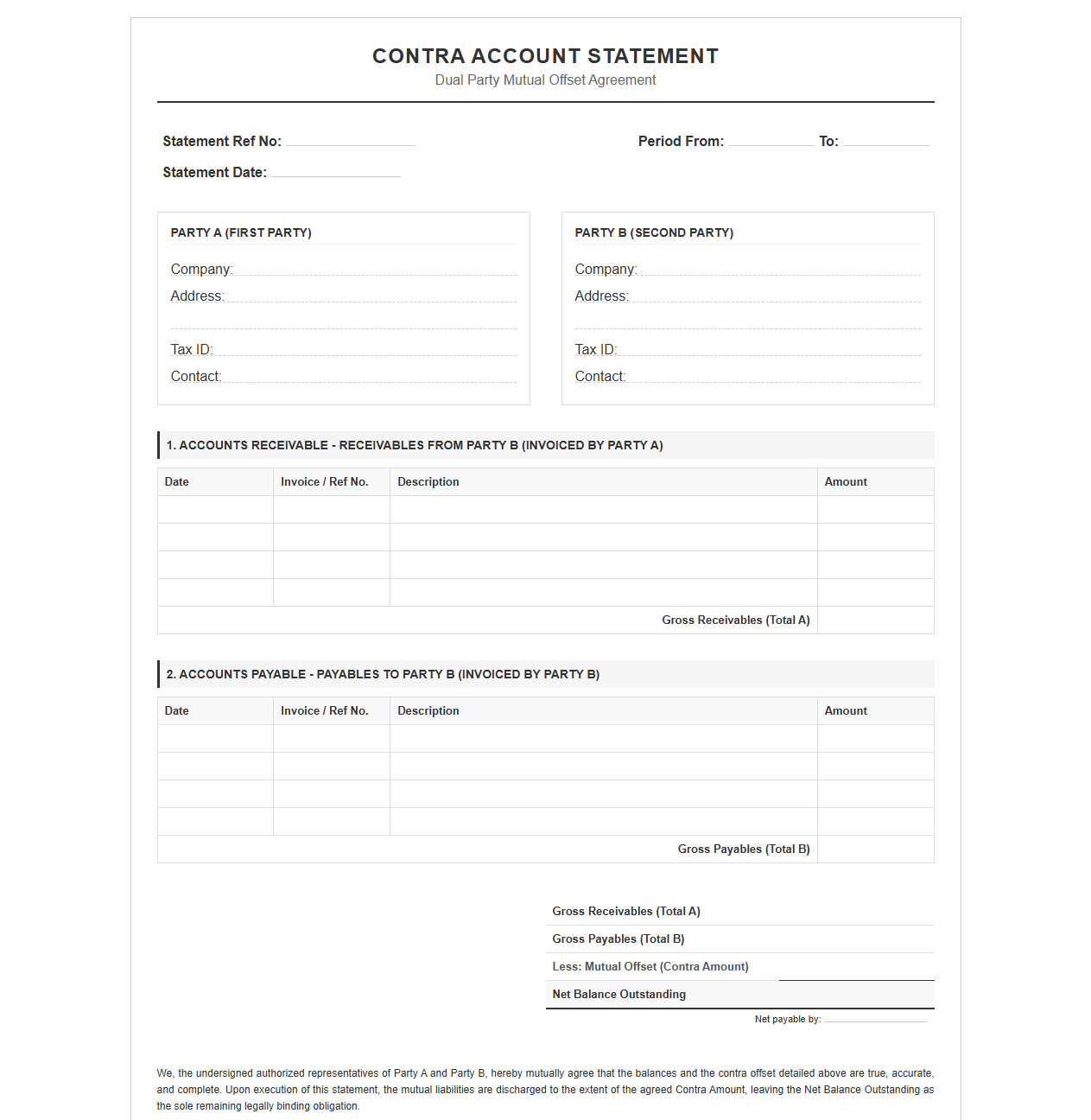

Dual Party Contra Account Statement Format

Download: .PDF

Download: .PDF

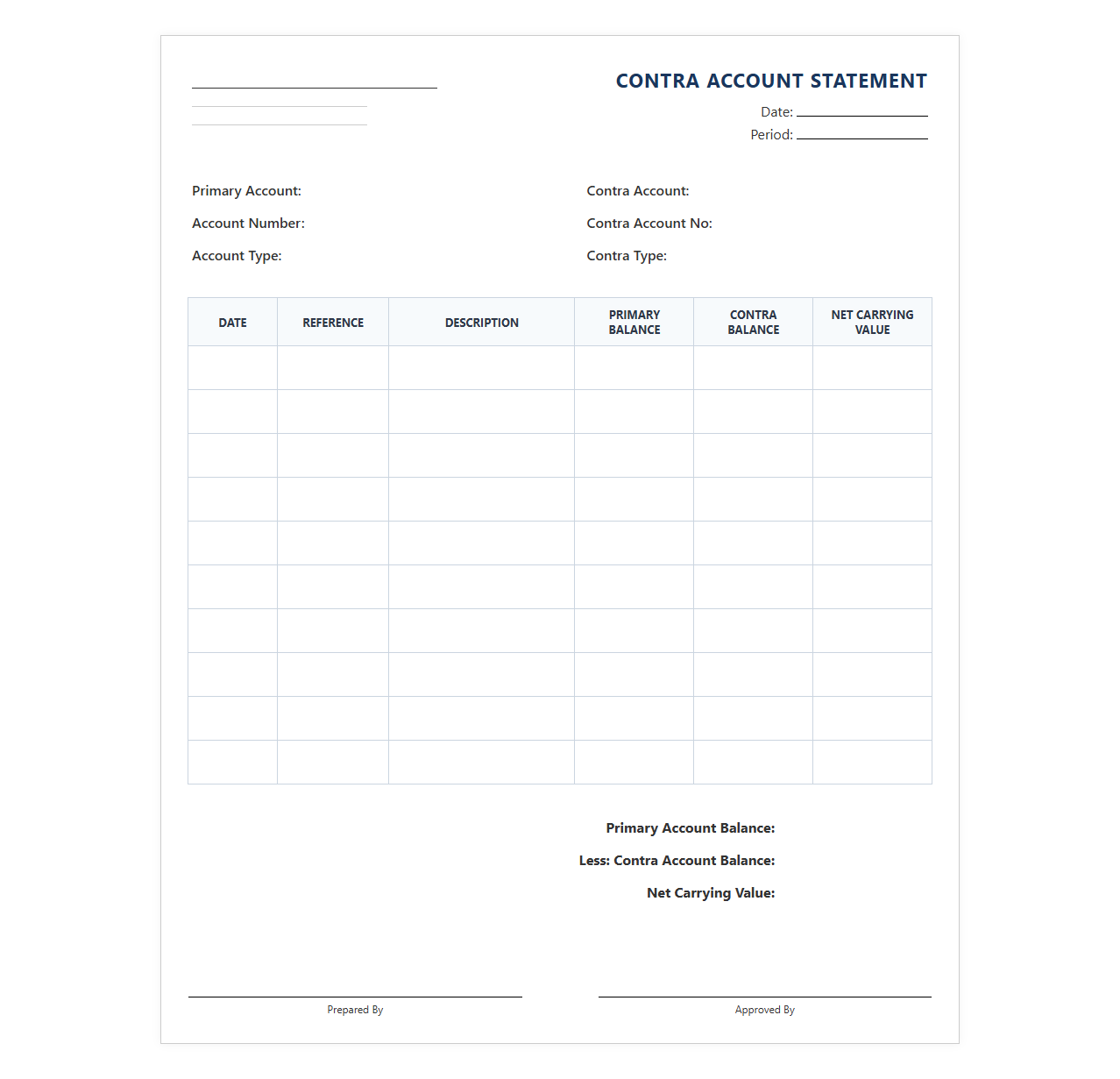

Contra Ledger Account Balance Statement Template

Download: .PDF

Download: .PDF

Understanding Contra Accounts and Common Balance Discrepancies

Contra accounts are specialized ledger accounts designed to offset a primary companion account on the balance sheet or income statement. Unlike standard accounts, a contra account carries a normal balance that is the opposite of its companion. For example, a contra asset account (such as Allowance for Doubtful Accounts) carries a normal credit balance to reduce the gross value of Accounts Receivable. Similarly, a contra liability account carries a normal debit balance, while a contra equity account (like Treasury Stock) reduces overall owner equity with a normal debit balance.

Balance discrepancies naturally emerge during the standard reconciliation cycle. These mismatches are frequently caused by timing differences between the recording of primary transactions and their corresponding offset entries. In addition, manual classification errors, systemic data feed drops, and unaligned ledger postings frequently lead to variances that require systematic investigation.

Systematic Audit Steps for Locating Discrepancies

To identify the root cause of discrepancies within contra account balances, finance teams should implement a structured audit process. This structured approach ensures every ledger entry is accounted for and matches the master schedule.

- Verify the trial balance totals against the subsidiary ledgers to confirm that the base assets or liabilities match their associated contra schedules.

- Perform systematic transaction matching, ensuring that every debit or credit to a primary account is accompanied by its corresponding contra entry when required by policy.

- Review the general ledger journal entries for the audit period, flagging any manual overrides or non-standard entries.

- Cross-reference physical asset registers or amortization tables with the system-generated depreciation schedules to catch rounding errors.

- Trace credit memos and return authorizations directly to the sales returns clearing accounts to verify posting dates.

Statement Template: Adjusting Allowance for Doubtful Accounts

Notification and Reconciliation Communication

The following template serves as a formal internal record and email communication to notify stakeholders of the adjustments required to correct discrepancies in the accounts receivable contra accounts.

To: Corporate Controller

From: Senior Accounting Analyst

Subject: Reconciliation Adjustment: Allowance for Doubtful Accounts (GL-1205)

We have completed the monthly reconciliation for Accounts Receivable and identified a discrepancy between the aging schedule and the contra asset balance. To bring the accounts into alignment, we must adjust the balance to reflect the correct valuation of realizable receivables.

Formal Adjustment Voucher

Please review the details of the adjustment below. The correction will update the allowance to match our verified historical write-off ratios.

Voucher ID: AR-ADJ-2026-04

Adjustment Type: Allowance for Doubtful Accounts Alignment

Account Impacted: 1205-00 (Contra Asset)

Offset Account: 5120-00 (Bad Debt Expense)

Statement Template: Rectifying Accumulated Depreciation Mismatches

Fixed Asset Register Reconciliation

This statement details the variance found between the physical fixed asset register and the corresponding accumulated depreciation ledger balance. Below is the formal reconciliation schedule used to document the correction.

| Asset Category | Register Accumulated Balance | General Ledger Balance | Required Adjustment |

|---|---|---|---|

| Machinery and Equipment | $145,200 | $148,000 | -$2,800 |

| Office Furniture | $34,100 | $33,500 | +$600 |

Statement Template: Aligning Sales Returns and Allowances

Revenue Contra Account Reconciliation Memo

This template is used to authorize the adjustments made to correct mismatches in the Sales Returns and Allowances contra revenue account.

This memo serves to document the alignment of the Sales Returns and Allowances account with actual processed customer credits. During the reconciliation of the sub-ledger, we discovered a lag in the processing of physical returned inventory versus issued credit memos. An adjusting entry is required to reflect accurate net sales for the period.

Justification of Adjustments

Failure to make this adjustment would lead to an overstatement of net revenue. By executing this adjustment, we ensure compliance with matching principles and prevent discrepancies in future audits.

Standard Journal Entries for Contra Account Adjustments

The following table outlines the exact journal entries required to resolve balance discrepancies within standard contra accounts. Each entry is structured to ensure proper debit and credit alignments.

| Discrepancy Scenario | Account Code | Account Name | Debit | Credit |

|---|---|---|---|---|

| Understated Allowance for Doubtful Accounts | 51201205 |

Bad Debt Expense Allowance for Doubtful Accounts (Contra Asset) |

$1,500 | - |

| - | - | - | - | $1,500 |

| Overstated Accumulated Depreciation | 15906230 |

Accumulated Depreciation (Contra Asset) Depreciation Expense |

$2,800 | - |

| - | - | - | - | $2,800 |

Proactive Controls to Prevent Future Contra Account Errors

To reduce the occurrence of reconciliation discrepancies, organizations should establish robust, systemic controls. Implementing standardized verification processes minimizes human error and guarantees report integrity.

- Automate the monthly depreciation calculations through integrated fixed asset management software.

- Implement dual-authorization workflows for any manual journal entries affecting contra accounts.

- Establish a weekly matching protocol for returns processing and customer credits.

- Conduct quarterly training sessions on contra account behavior for new accounting personnel.

Leave a comment