Financial executives and accounting teams frequently battle the high-stakes fallout of reporting inaccuracies, where a single spreadsheet formula error can trigger compliance penalties and severely erode investor confidence. Before addressing these errors directly, we must first recognize how the growing complexity of modern regulatory standards has made manual ledger reconciliation virtually obsolete.

Implementing structured net earnings statement templates grants organizations immediate transactional clarity, saving critical hours during year-end audits. Note, however, that while these structured frameworks drastically reduce input errors, they are designed as foundational tools and should not replace qualified CPA oversight. For instance, utilizing pre-formatted cells prevents common missteps like misclassifying operating expenses or miscalculating depreciation.

In this article, we will explore how to deploy these standardized templates to systematically eliminate reporting discrepancies, establish robust internal controls, and restore absolute integrity to your corporate financial statements.

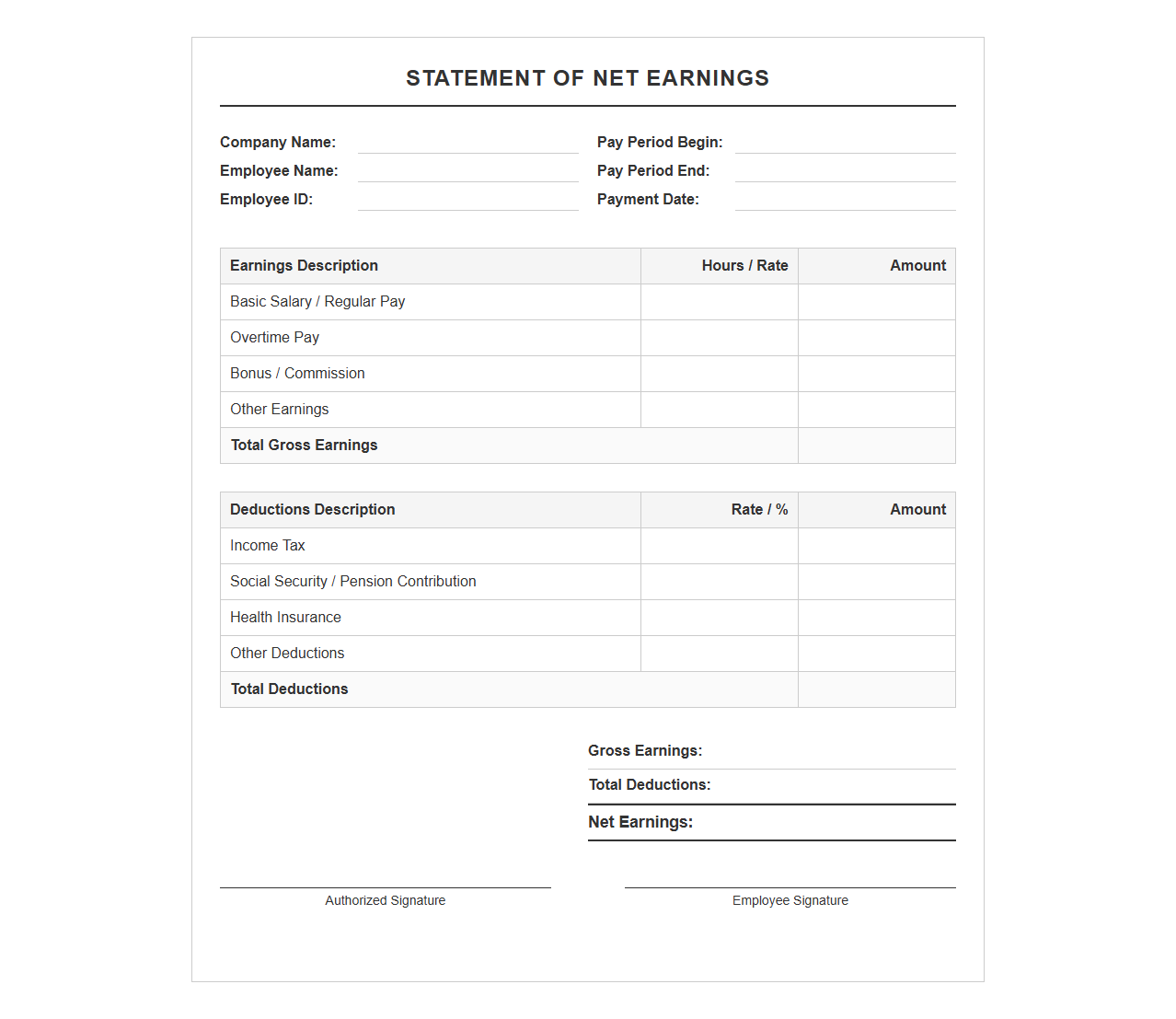

Net Earnings Statement Template

Download: .PDF

Download: .PDF

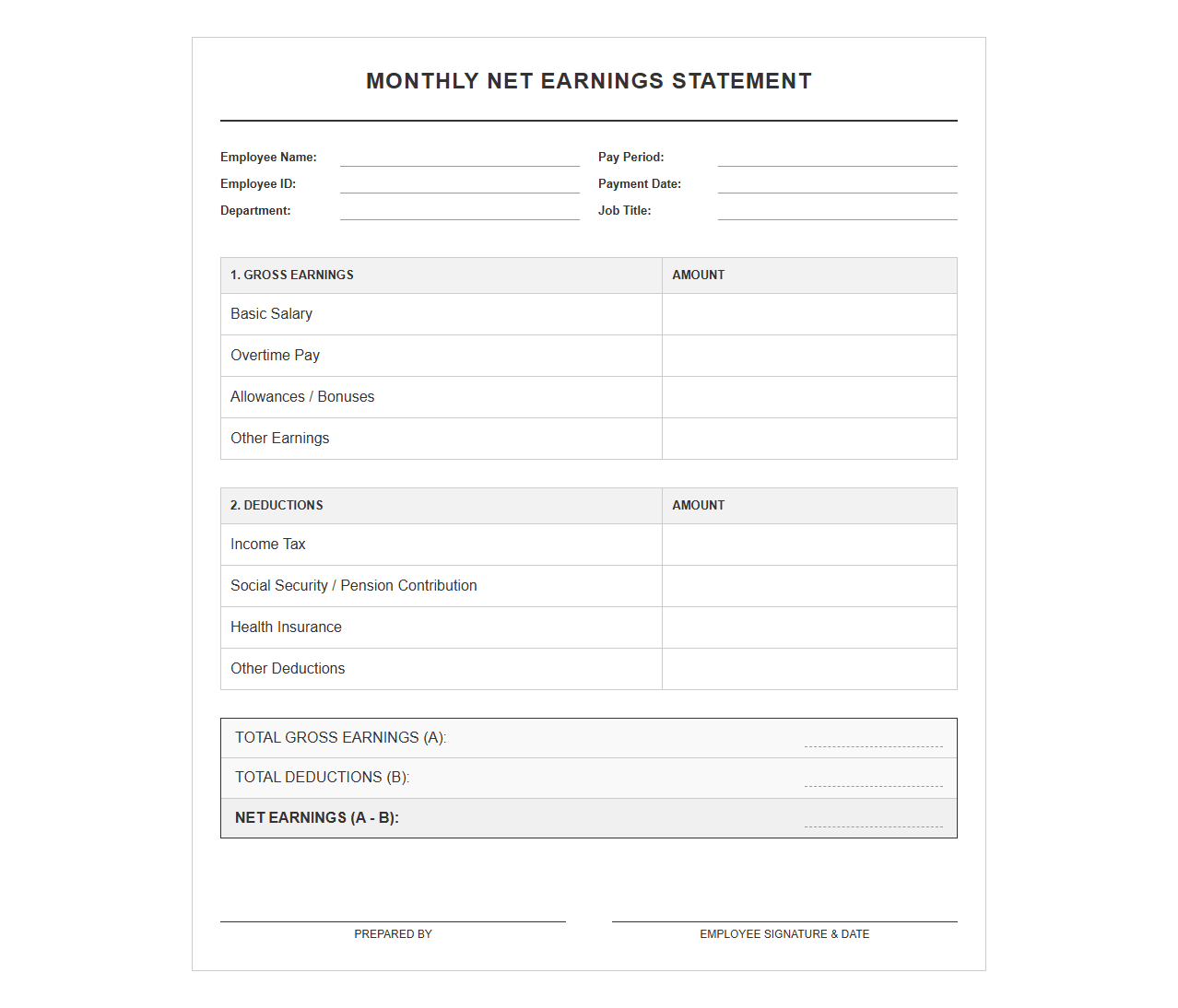

Monthly Net Earnings Statement Form

Download: .PDF

Download: .PDF

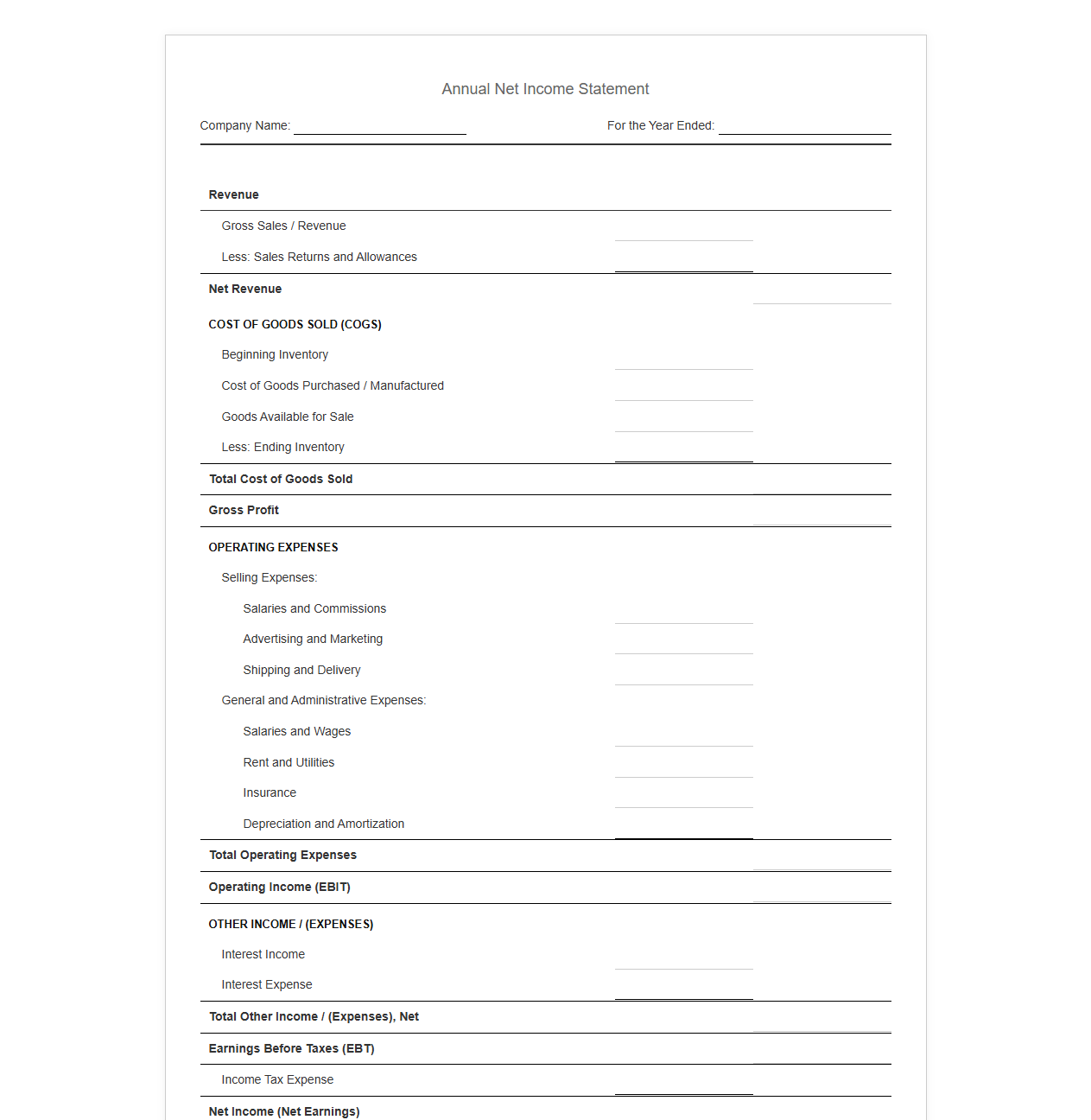

Annual Net Income Statement Template

Download: .PDF

Download: .PDF

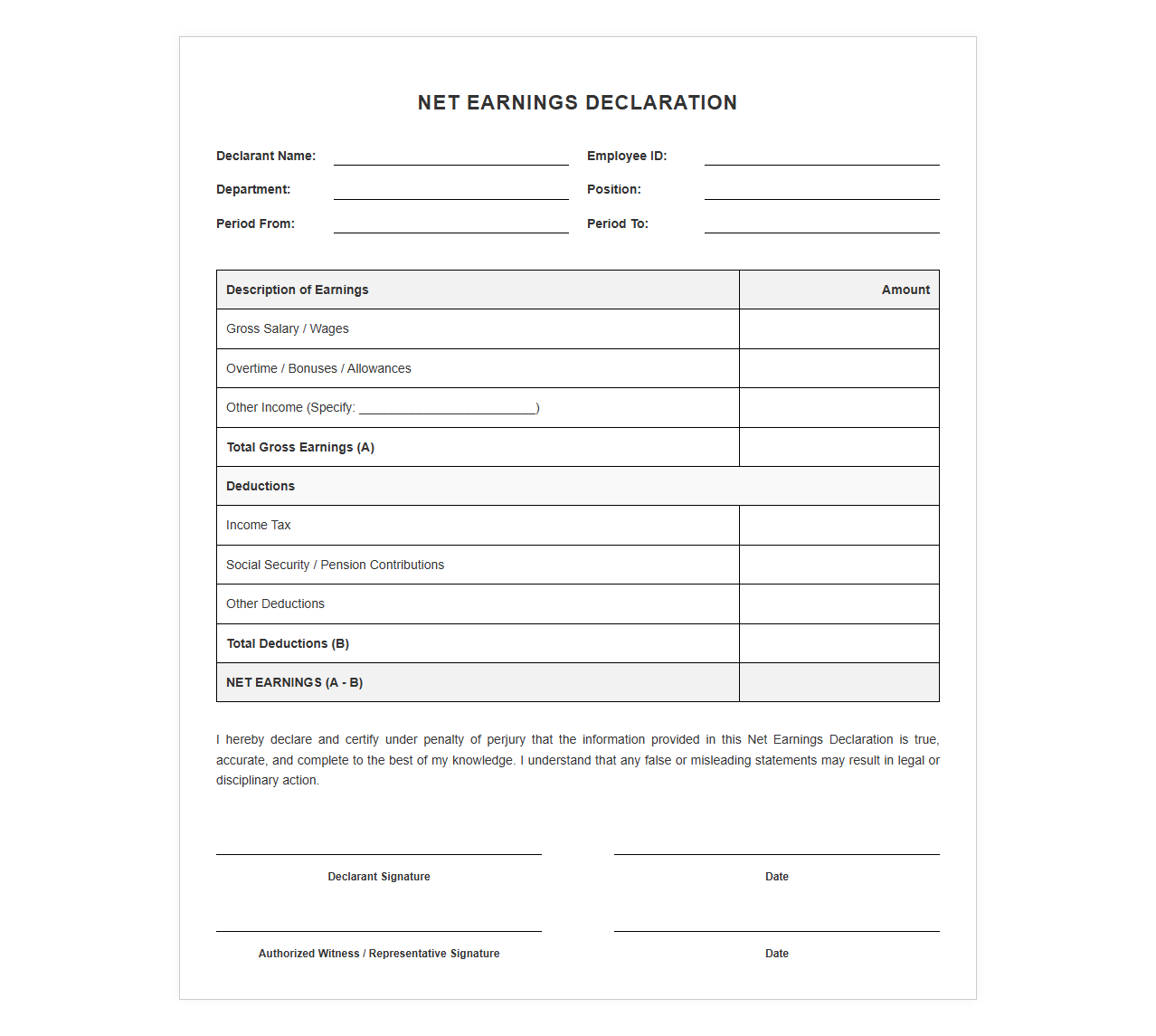

Net Earnings Declaration Template

Download: .PDF

Download: .PDF

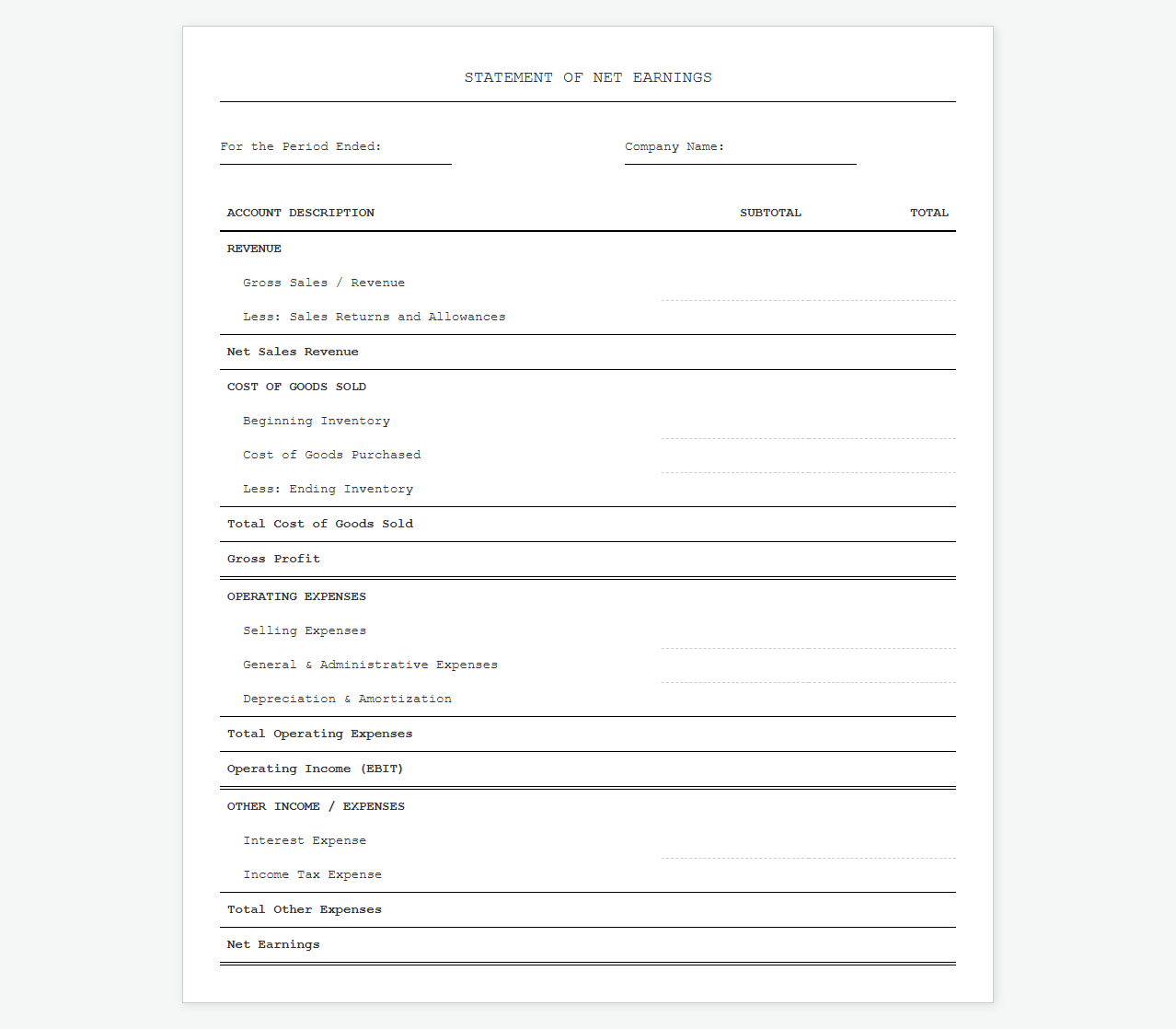

Statement of Net Earnings Spreadsheet

Download: .PDF

Download: .PDF

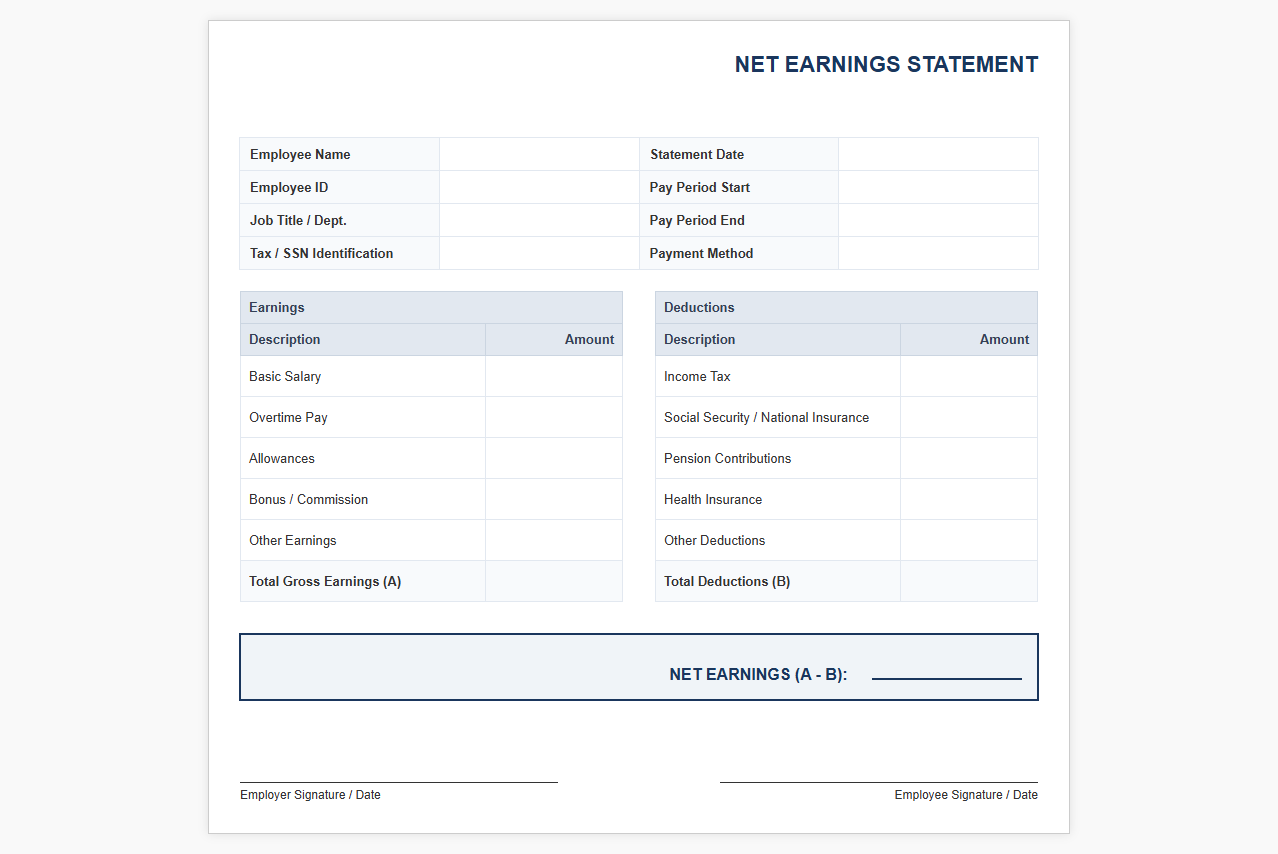

Employee Net Earnings Statement Format

Download: .PDF

Download: .PDF

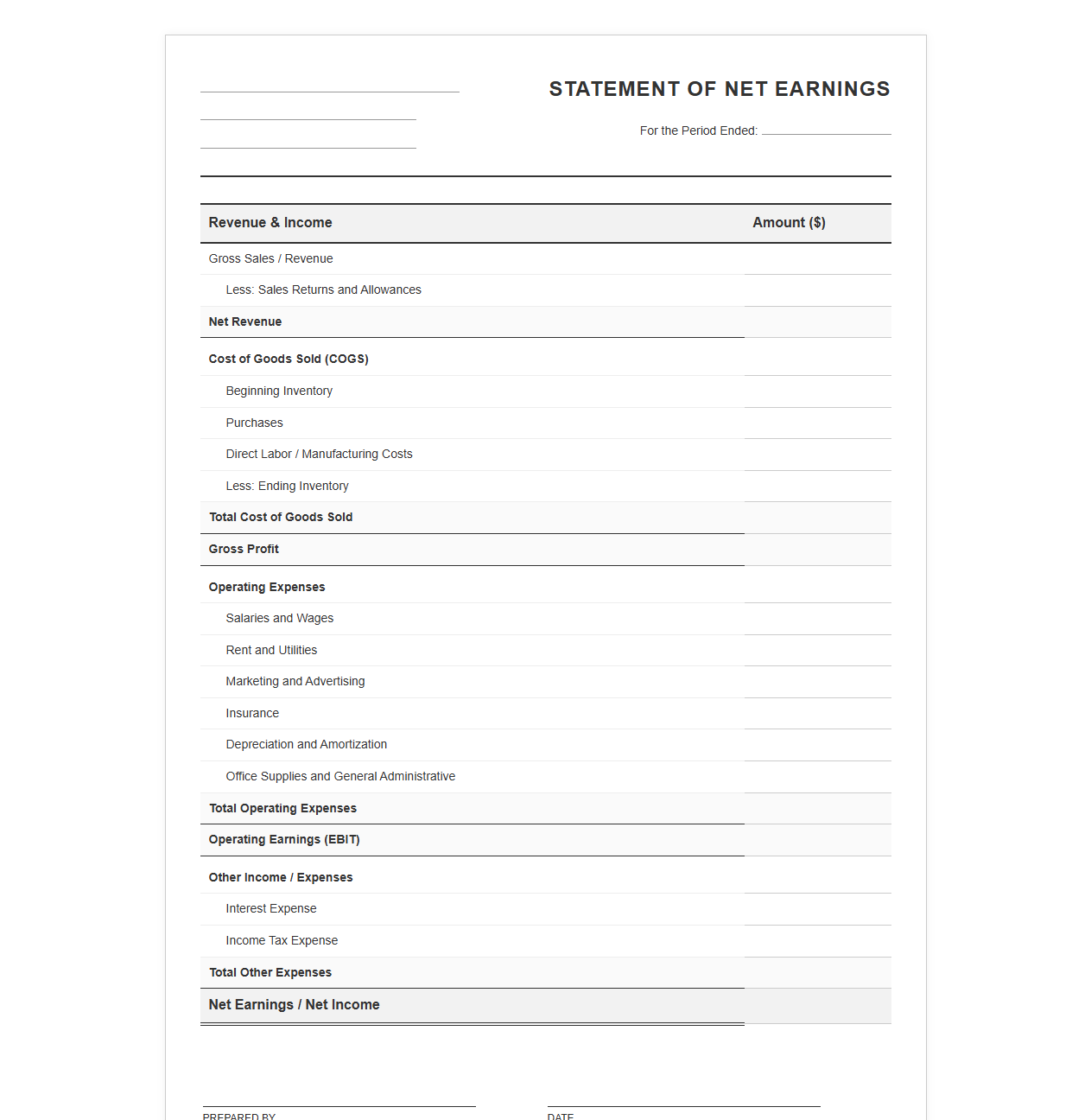

Business Net Earnings Statement Template

Download: .PDF

Download: .PDF

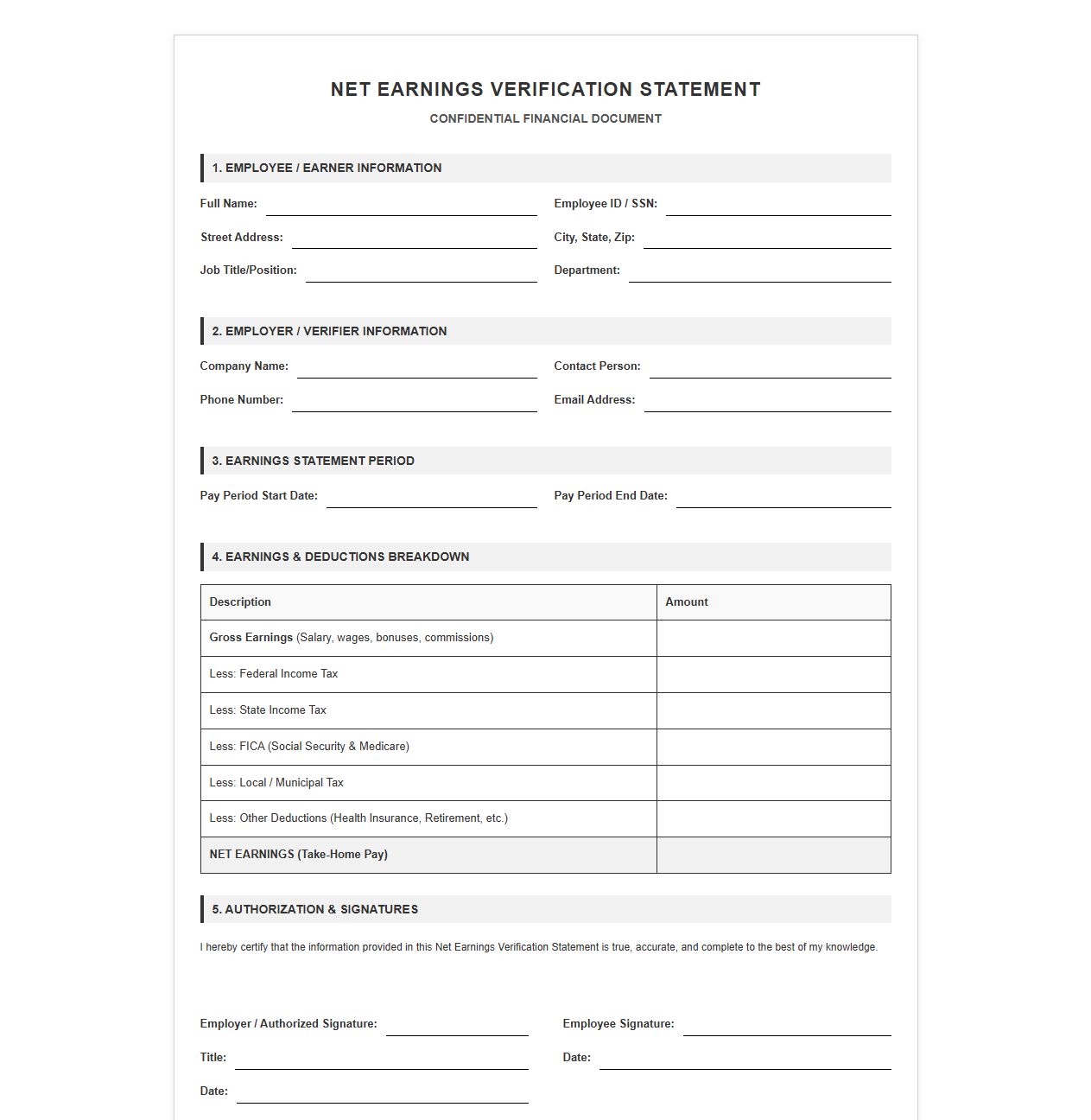

Net Earnings Verification Statement Form

Download: .PDF

Download: .PDF

The High Cost of Financial Reporting Discrepancies

In the high-stakes arena of corporate accounting, a single decimal point out of place can trigger a catastrophic chain reaction. Financial reporting errors are more than mere administrative oversights; they represent a fundamental threat to corporate viability. When public companies publish inaccurate books, the immediate fallout often involves severe regulatory fines, costly restatements, and a plummeting share price.

Beyond the immediate balance sheet impact, the erosion of stakeholder trust is the most damaging consequence. Investors, lenders, and board members rely on these statements to make critical capital allocation decisions. Once that trust is fractured by reporting discrepancies, rebuilding credibility can take years of painstaking oversight and restructured governance.

Demystifying the Net Earnings Statement

The net earnings statement, often referred to as the income statement, serves as a company's financial scorecard over a specific reporting period. It tracks how revenue is transformed into net income, illustrating the operational efficiency of the enterprise.

Core Components of the Statement

An accurate statement must cleanly delineate several key layers. It begins with gross revenue, from which the cost of goods sold is subtracted to reveal gross profit. From there, operating expenses, depreciation, amortization, interest, and taxes are systematically deducted to arrive at the net income-the final bottom line that dictates shareholder value.

The Vital Need for Structural Consistency

Without structural consistency, historical comparison becomes virtually impossible. If expenses are categorized differently from one quarter to the next, financial analysts cannot accurately identify margin trends or assess long-term operational health. Standardized formatting ensures that external analysts and internal decision-makers are always comparing apples to apples.

Root Causes of Mathematical and Categorization Errors

Despite the advancement of financial technology, errors frequently slip into earnings reports. These inaccuracies generally stem from two primary sources: manual human oversight and disconnected software systems.

- Manual Data Entry Blunders: Simple transposition errors, where digits are accidentally reversed, can quietly compromise entire spreadsheets.

- Misclassification of Expenses: Erroneously categorizing capital expenditures as immediate operating expenses artificially deflates current-period earnings.

- Broken Spreadsheet Formulas: Over-reliance on legacy, unmanaged spreadsheets often leads to broken cell references and circular logic.

- System Integration Gaps: Discrepancies often emerge when data is migrated between disparate platforms without proper reconciliation protocols.

The Power of Structured Templates as a Safeguard

Transitioning from ad-hoc reporting methods to standardized, structured templates is one of the most effective ways to eliminate calculation anomalies. These frameworks establish rigid mathematical rules that cannot be easily altered or bypassed by individual users.

Implementing standardized templates ensures that formulaic integrity is locked down at the institutional level, removing the risk of localized spreadsheet corruption.

By automating the aggregation of sub-ledgers and enforcing standardized taxonomies, structured templates serve as an active defense mechanism. They prevent users from manually overwriting cells, thereby maintaining mathematical consistency across every reporting cycle.

A Step-by-Step Guide to Resolving Discrepancies

- Isolate the variance by running a comparative analysis between the current draft and the trial balance using the template's built-in

RECONCILEfunction. - Trace the flagged discrepancy back to its source transaction ledger to verify if the root cause is a duplicate entry or a missing input.

- Correct the erroneous entry directly within the master data feed rather than patching the final report sheet, maintaining data lineage.

- Re-import the corrected dataset into the structured template and execute the

VALIDATE_MATHscript to ensure all formulas calculate correctly. - Lock the finalized version of the report, applying a unique

VERSION_IDto prevent unauthorized post-audit modifications.

Proactive Auditing and Continuous Quality Assurance

Preventing reporting errors requires a shift from reactive troubleshooting to continuous, proactive quality control. Relying solely on year-end audits is no longer sufficient in a fast-paced corporate landscape.

Implementing a Robust Internal Audit Framework

Establish a regular cadence of internal audits to catch anomalies before they reach external eyes. This systematic approach relies on clear validation procedures and shared accountability.

- Conduct monthly random sampling of ledger entries against source invoices to ensure transactional accuracy.

- Utilize automated data validation scripts to flag unusual variances or unexpected accounting treatments instantly.

- Enforce a mandatory peer-review protocol where a secondary analyst must sign off on all template overrides.

Future-Proofing Compliance and Financial Transparency

Adopting structured net earnings statements is not merely an exercise in error reduction; it is a strategic investment in the organization's future. By embedding standardization directly into the reporting infrastructure, companies establish a foundation for uncompromising compliance and operational agility.

This rigorous approach significantly cuts down external audit times, as auditors can easily trace and verify the underlying formulas. A transparent, error-free financial presentation is the most powerful tool a corporation has to secure investor confidence and pave the way for sustainable market growth.

Leave a comment