Managing corporate tax compliance is an increasingly tedious burden, particularly when calculating and tracking Accumulated Earnings and Profits (E&P) across multiple tax years. As IRS scrutiny intensifies and tax codes evolve, relying on fragmented legacy spreadsheets introduces significant risk of calculation errors and costly penalties.

To address this, organizations must first establish a standardized reporting framework. Leveraging structured E&P statement templates grants tax departments immediate analytical clarity and robust audit-readiness. However, as a crucial stipulation, these templates are only as effective as the data governing them; they must be carefully tailored to account for complex variables such as Section 312 adjustments, net operating losses, and tax-exempt income.

In this guide, we will explore the essential components of a reliable E&P template, discuss best practices for data integration, and outline how to streamline your corporate distribution reporting to ensure seamless compliance.

Accumulated Earnings and Profits Statement Template

Download: .PDF

Download: .PDF

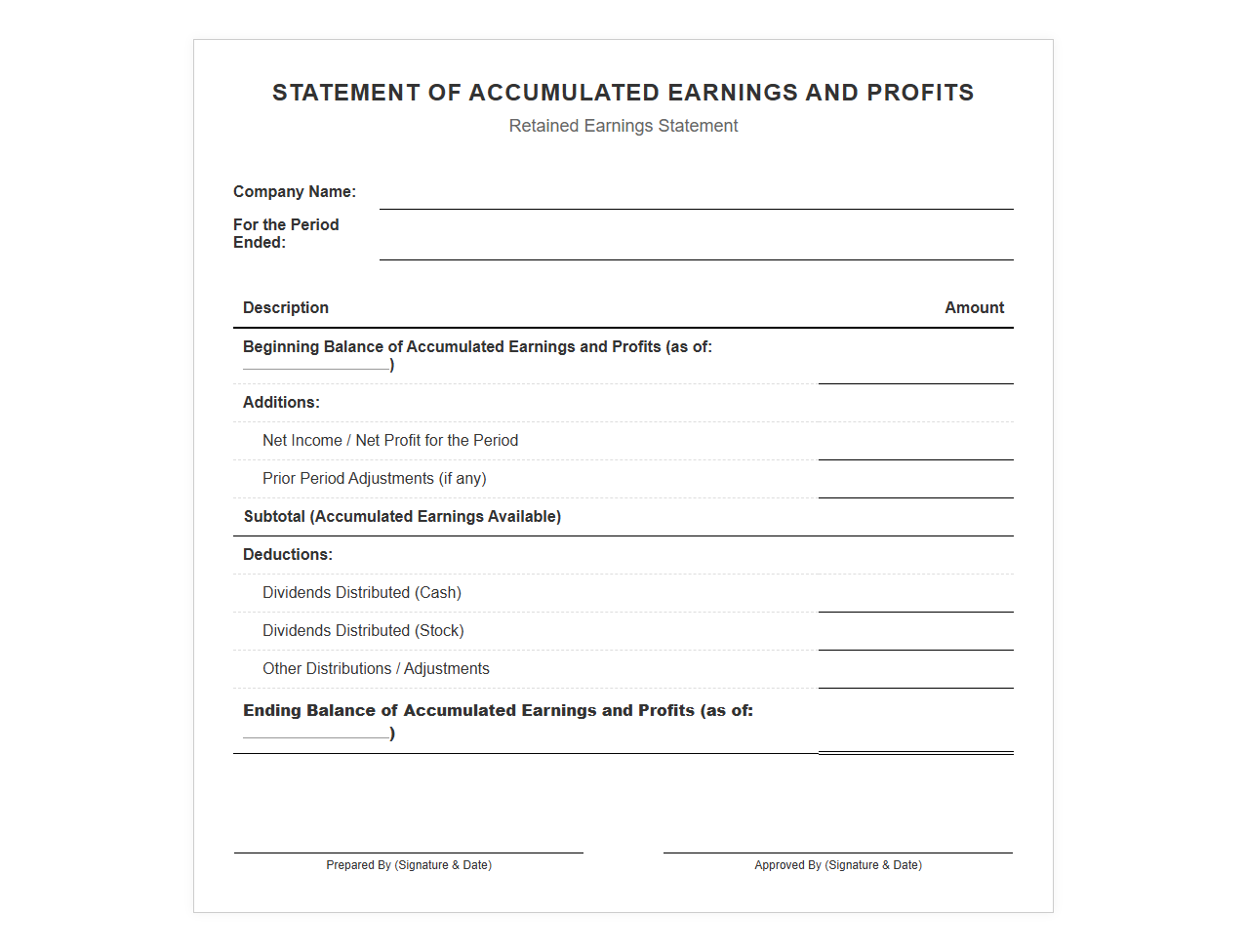

Retained Earnings and Accumulated Profits Statement Template

Download: .PDF

Download: .PDF

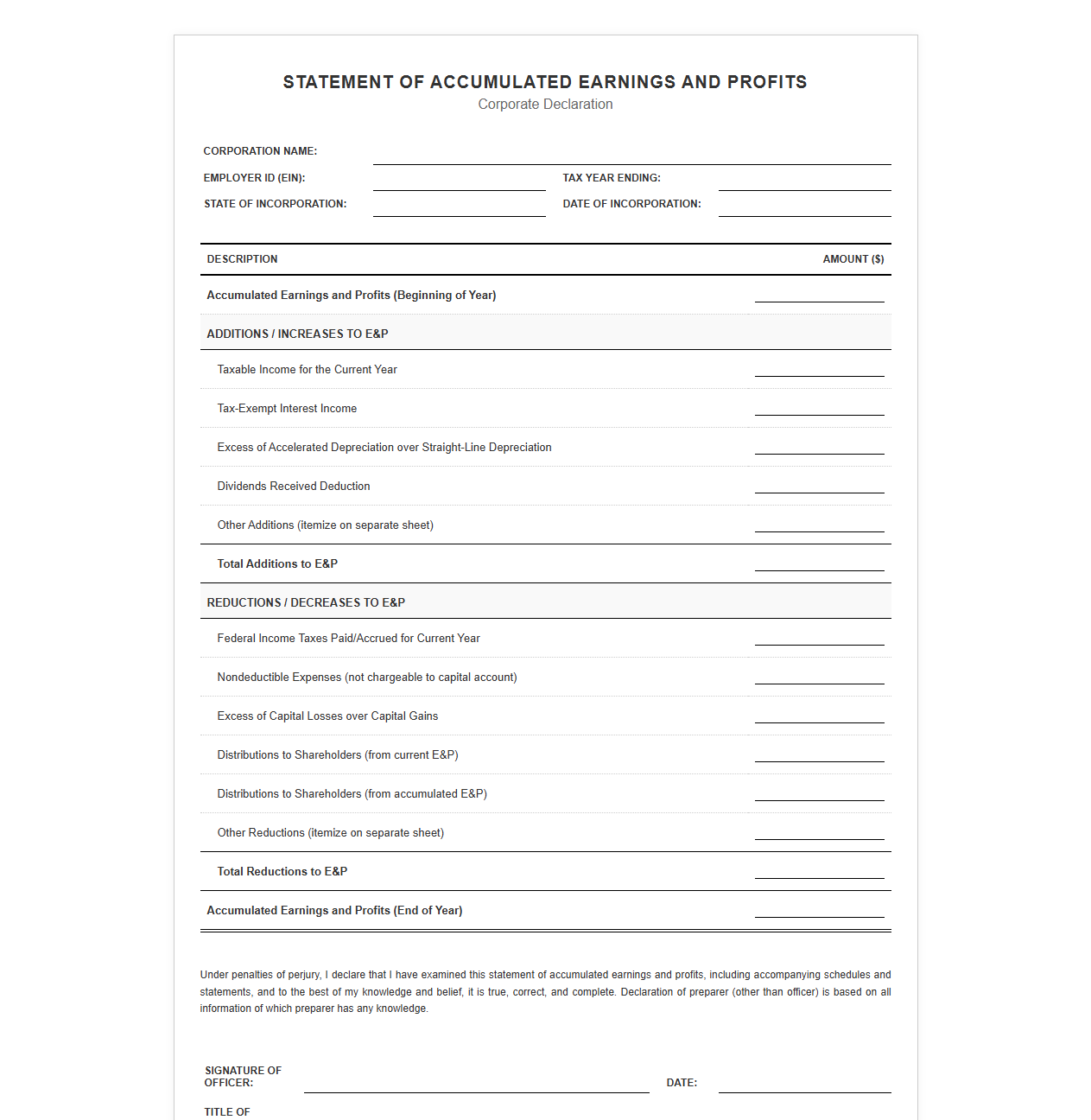

Corporate Accumulated Earnings and Profits Declaration

Download: .PDF

Download: .PDF

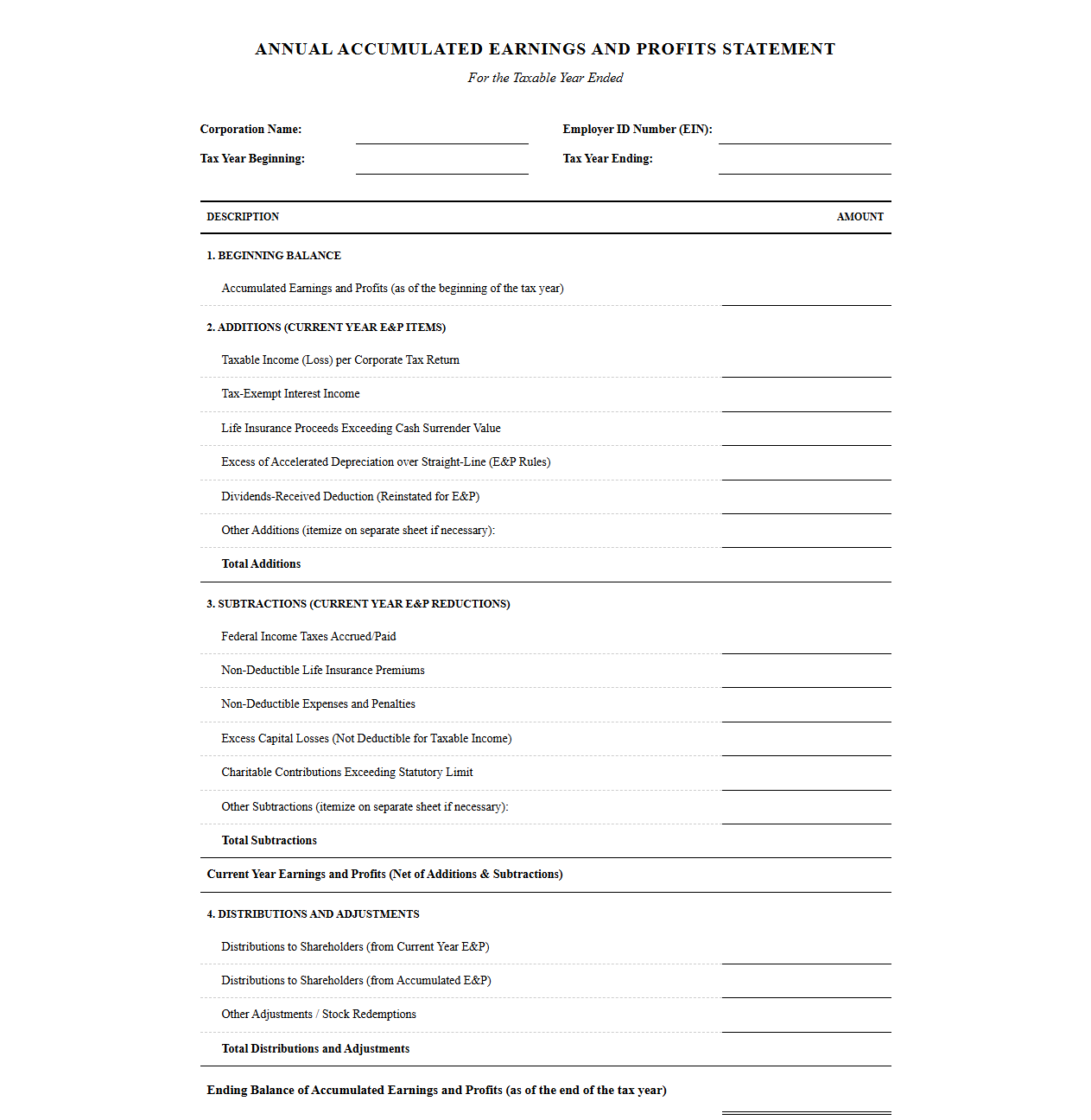

Annual Accumulated Earnings and Profits Statement

Download: .PDF

Download: .PDF

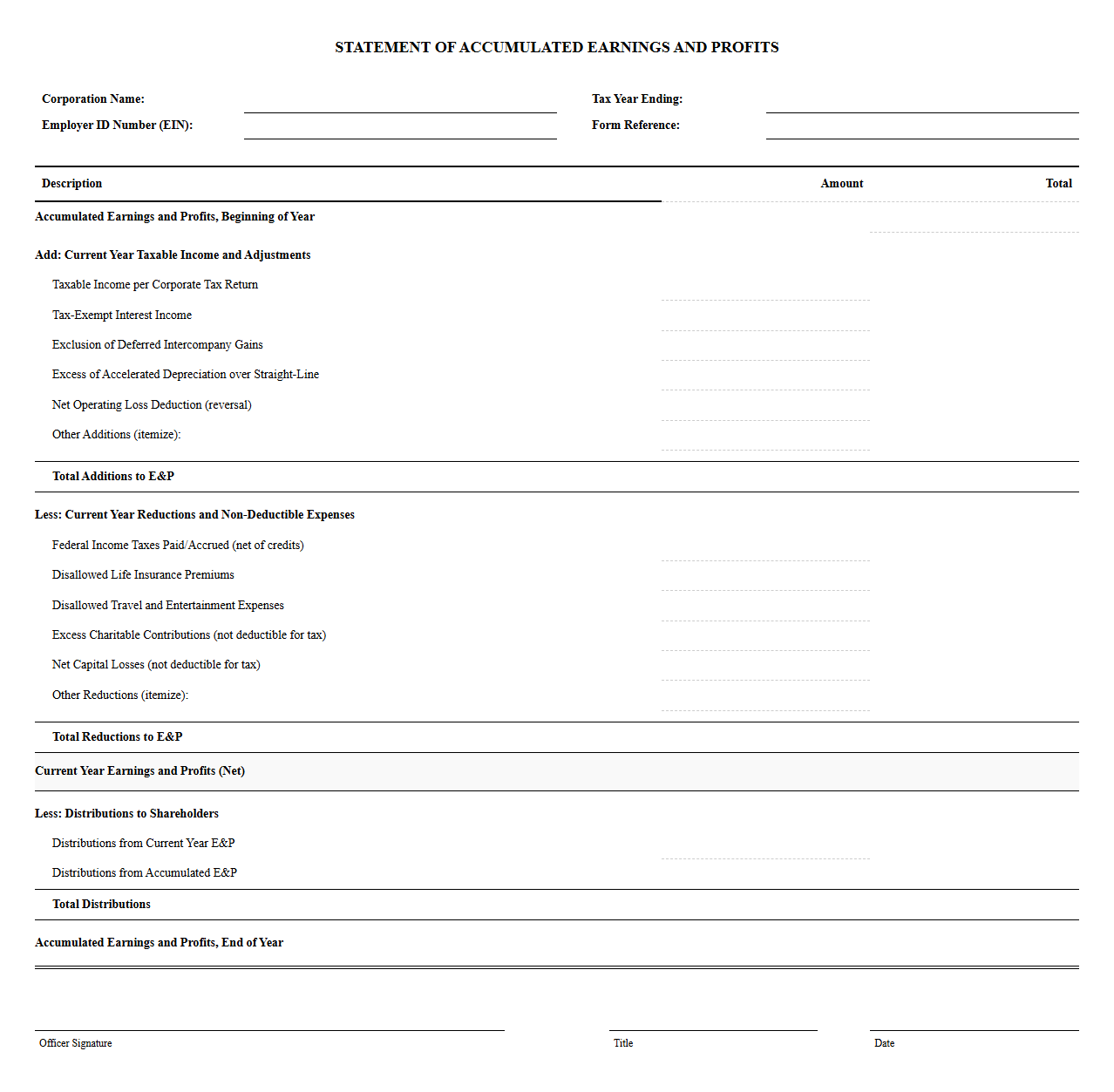

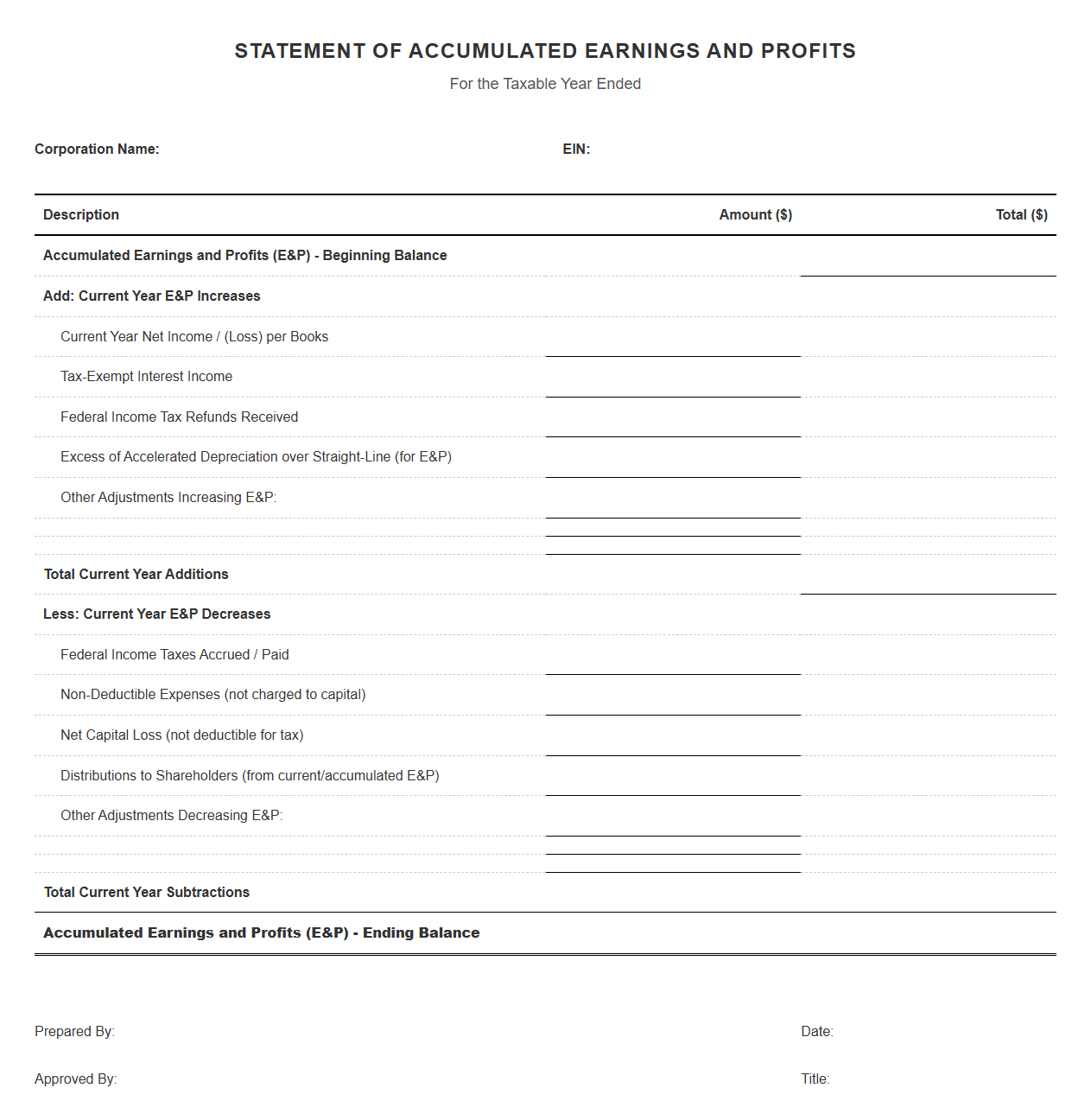

Statement of Accumulated Earnings and Profits

Download: .PDF

Download: .PDF

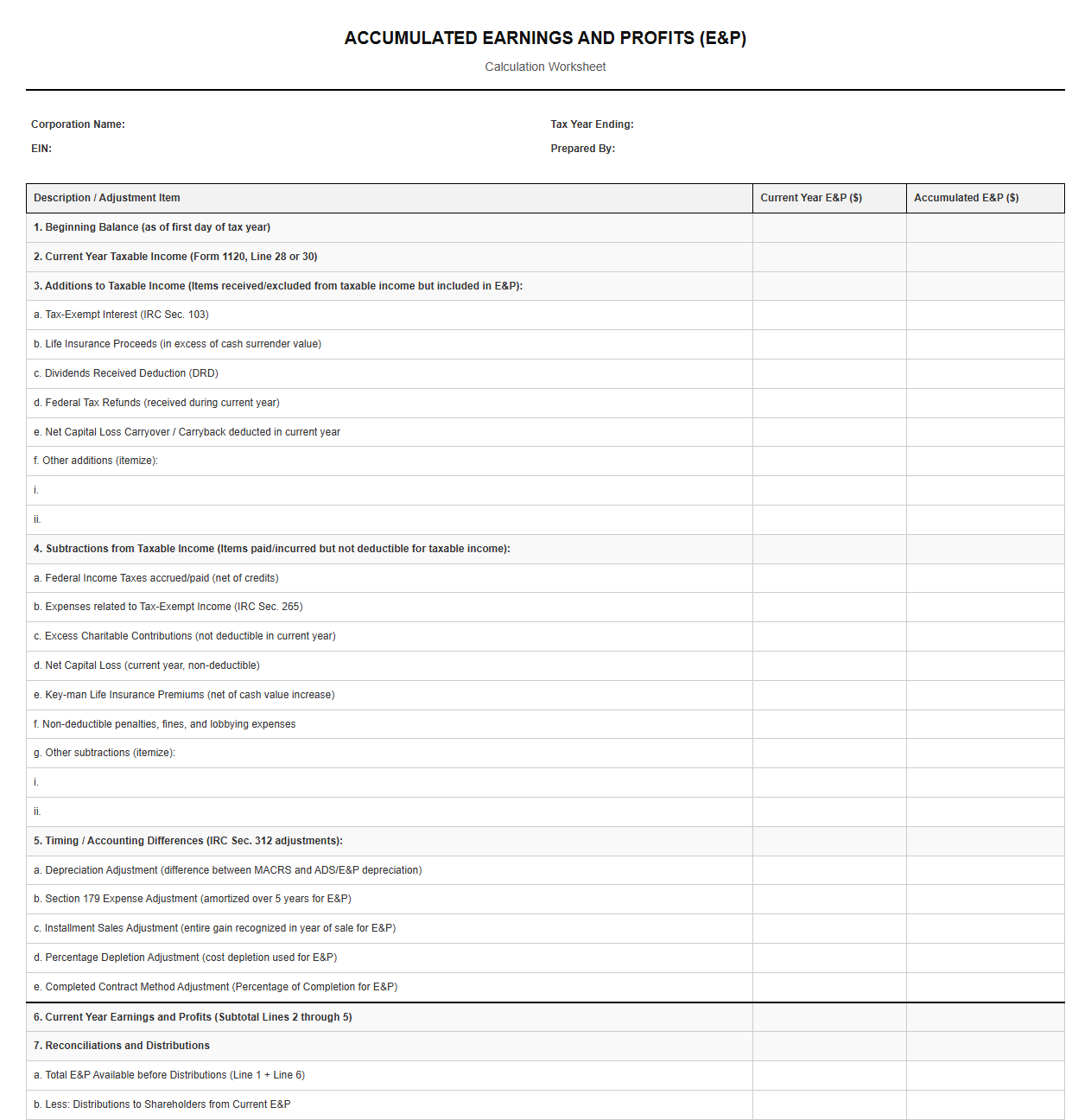

Accumulated Earnings and Profits Calculation Worksheet

Download: .PDF

Download: .PDF

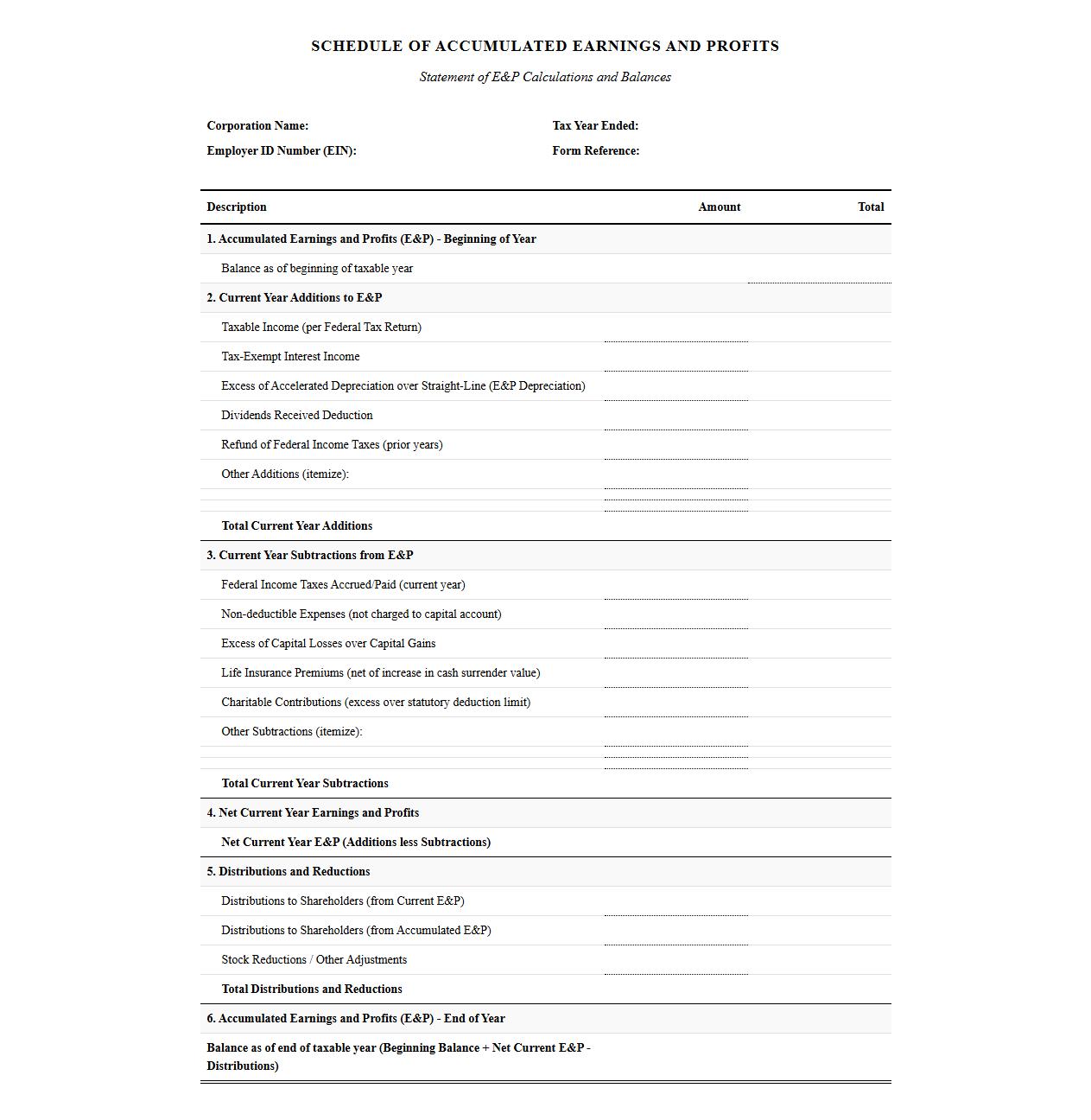

Schedule of Accumulated Earnings and Profits Template

Download: .PDF

Download: .PDF

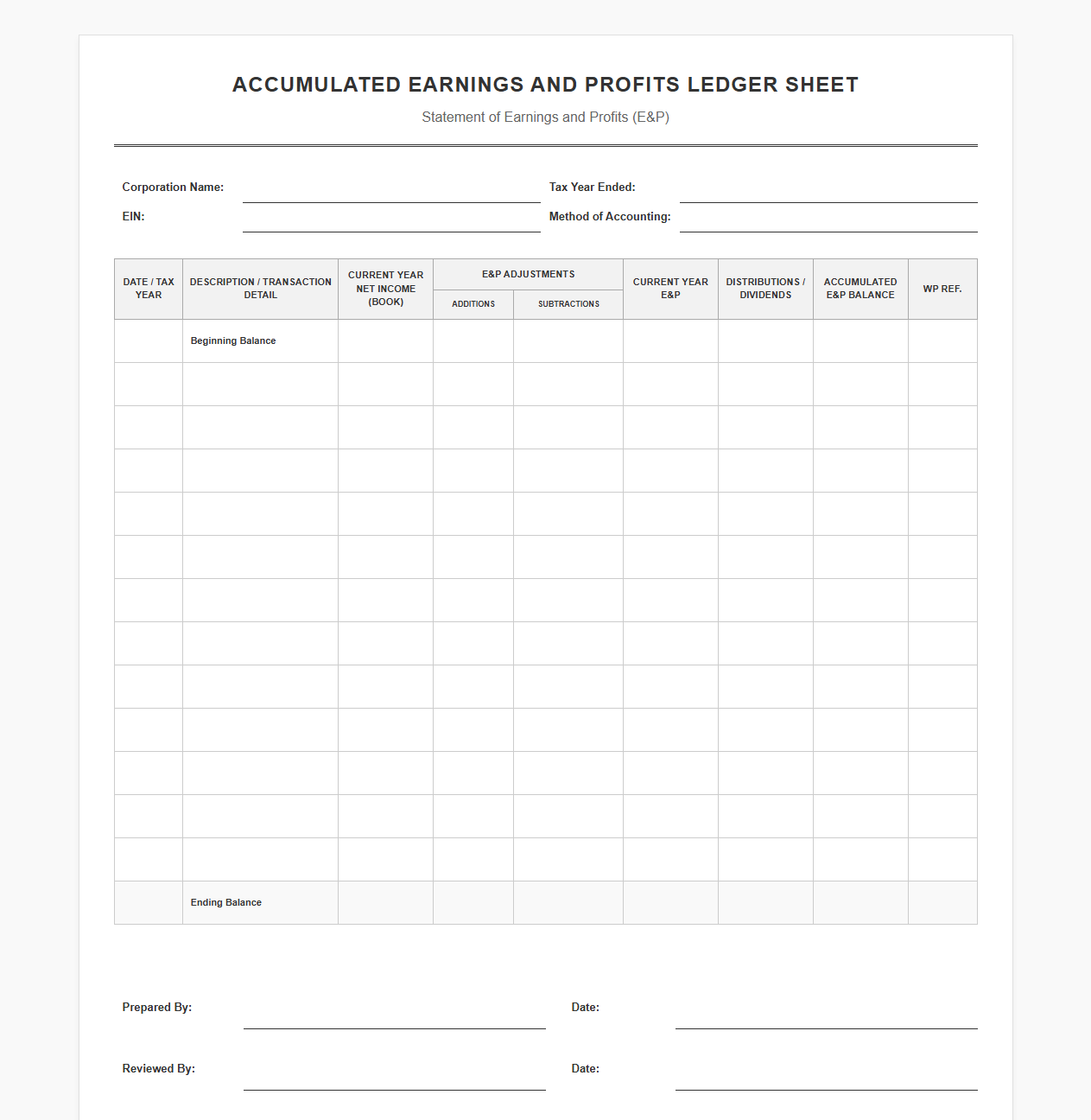

Accumulated Earnings and Profits Ledger Sheet

Download: .PDF

Download: .PDF

Navigating Corporate Tax Compliance and Accumulated E&P

Corporate tax compliance is an intricate maze of shifting regulations, complex calculations, and rigorous reporting standards. Among the most critical yet challenging obligations for corporate tax departments is the accurate measurement of Accumulated Earnings and Profits (E&P). This metric represents a corporation's economic capacity to pay dividends to its shareholders. Maintaining a precise, historical log of E&P is vital for strategic financial planning, as it dictates the taxability of corporate distributions and prevents severe regulatory penalties. Failing to monitor this metric can lead to disastrous tax consequences for both the corporation and its investors.

Decoding Accumulated Earnings and Profits (E&P)

Accumulated Earnings and Profits (E&P) is a federal tax concept that measures a corporation's economic ability to make distributions to its shareholders. Unlike book retained earnings, which are calculated under Generally Accepted Accounting Principles (GAAP) to reflect financial performance, E&P is strictly a tax accounting metric. While retained earnings focus on reporting profitability to public markets and creditors, E&P reflects the actual liquid funds available for non-liquidating distributions.

Distinguishing between these two metrics is critical because E&P directly determines whether a distribution is taxed as an ordinary dividend, a tax-free return of capital, or a capital gain. When corporate distributions exceed E&P, shareholders receive a return of capital, reducing their stock basis. Without a precise, continuous calculation of E&P, corporations risk mischaracterizing these transactions, leading to incorrect tax reporting and potential litigation.

The Strategic Value of E&P Statement Templates

Standardizing the tracking of Accumulated E&P through dedicated templates transforms how corporate tax teams operate. Manual tracking in disparate spreadsheets is highly vulnerable to user error, formula breaks, and version control issues. Implementing a standardized E&P statement template addresses these vulnerabilities systematically.

- Streamlines the aggregation of financial data from multiple accounting systems and tax software.

- Reduces manual calculation errors by locking complex tax formulas and validation rules.

- Establishes a uniform framework that ensures corporate audit readiness during internal or external reviews.

- Facilitates historical data preservation, making it easier to trace E&P adjustments across multiple decades.

Core Components of a Standard E&P Statement

To construct an accurate Accumulated E&P template, tax teams must systematically apply specific adjustments to reconcile taxable income with economic reality. This process requires a clear division of calculations, starting with taxable income as the baseline.

- Baseline Taxable Income: The initial starting point taken from the federal corporate tax return (Form 1120).

- Permanent Differences: Adjustments for items that are recognized for tax purposes but not economic purposes, or vice versa, such as tax-exempt interest income and non-deductible life insurance premiums.

- Temporary Differences: Adjustments to align differing depreciation methods, amortization timelines, and installment sale recognition between tax accounting and E&P rules.

- Direct E&P Adjustments: Specific statutory adjustments, including federal income taxes paid and disallowed entertainment expenses, which directly reduce current E&P.

Mitigating Compliance Risks and Audit Triggers

Mischaracterizing corporate distributions is a major red flag for the Internal Revenue Service (IRS). When a corporation misclassifies a taxable dividend as a return of capital due to inaccurate E&P calculations, it triggers severe compliance risks, including back taxes, interest, and accuracy-related penalties.

By establishing a standardized and repeatable process, corporate tax departments can proactively identify discrepancies before filing, significantly lowering the likelihood of triggering a comprehensive corporate tax audit.

Best Practices for Implementing E&P Templates

To maximize the utility of E&P templates, corporate finance teams must transition from an annual, reactive calculation model to a proactive, ongoing process. Integrating E&P tracking into monthly or quarterly closing workflows ensures that leadership always has access to real-time data for distribution planning.

Additionally, organizations should establish strict access controls over the template to maintain data integrity. Only designated tax professionals should have the authority to modify underlying formulas, while regular audits of the template's inputs should be scheduled to align with the latest tax code updates and legislative changes.

Achieving Seamless Corporate Tax Management

Maintaining accurate, historical E&P records is not merely a compliance check-the-box exercise; it is a foundational pillar of proactive corporate financial management. By utilizing structured, technology-driven templates, organizations secure a single source of truth that simplifies distribution planning and protects the company from regulatory exposure.

"Adopting a structured methodology for tracking Accumulated E&P safeguards corporate assets, provides clarity to shareholders, and ensures the organization remains resilient under rigorous regulatory scrutiny."

Investing in reliable E&P tracking tools and standardized templates equips tax leaders with the clarity needed to make confident, strategic decisions that support long-term corporate growth and flawless tax compliance.

Leave a comment