Navigating IRS disputes is notoriously stressful for taxpayers, but for tax professionals, establishing clear, legally binding boundaries with anxious clients can be equally challenging. Before resolving complex tax liabilities, practitioners must first secure their professional boundaries under Treasury Department Circular 230 guidelines.

Implementing standardized representation agreements grants practitioners immediate liability protection and safeguards against scope creep. However, these templates must stipulate that professional representation does not guarantee a specific IRS outcome, effectively managing client expectations from day one. For instance, incorporating explicit clauses regarding IRS Form 2848 (Power of Attorney) authorization and installment agreement negotiation terms serves as vital proof of a well-defined engagement.

The following guide explores the essential components of standard tax representation agreements, detailing how to draft protective clauses and leverage templates to streamline your resolution practice.

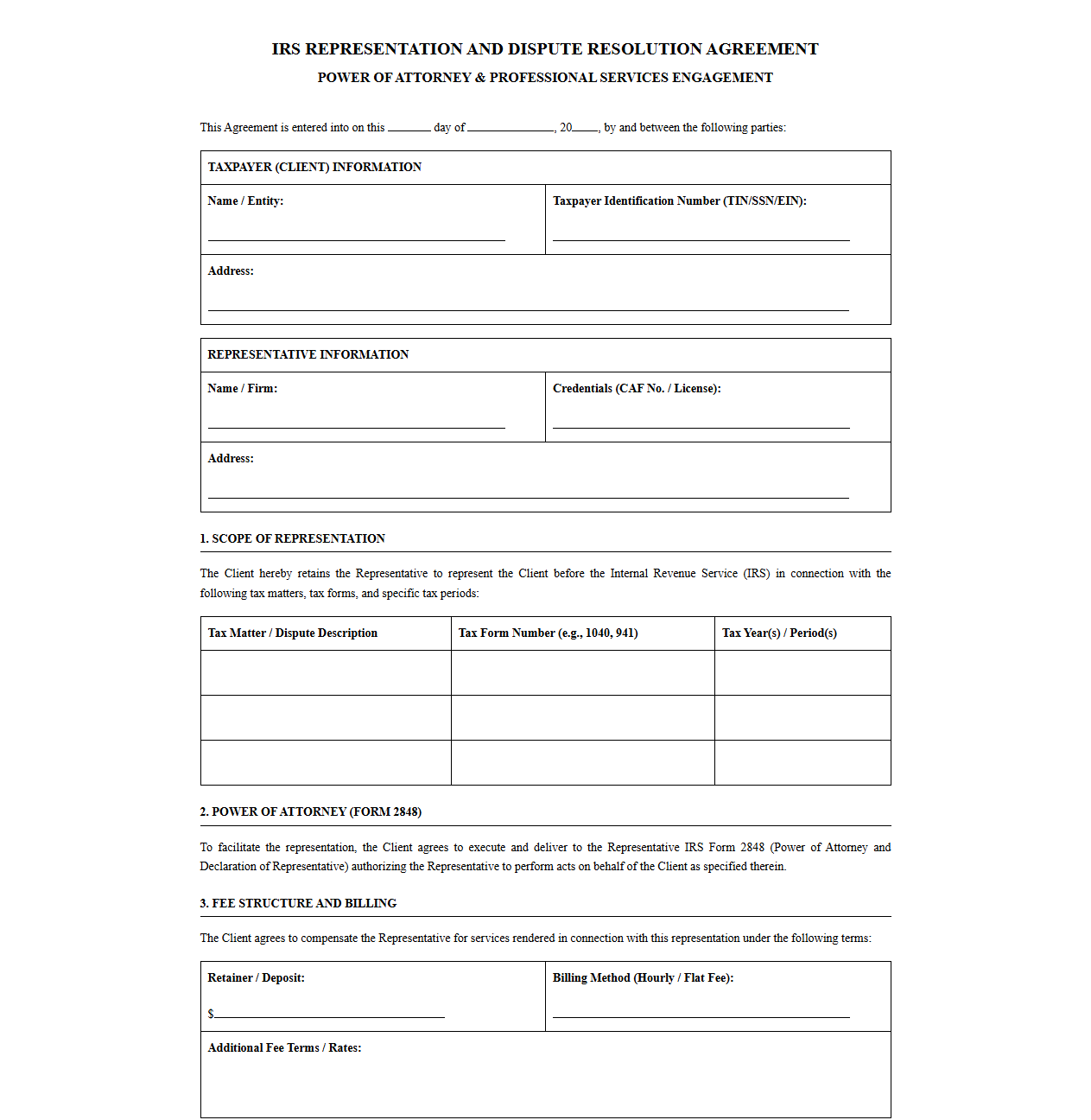

IRS Representation and Tax Dispute Resolution Agreement

Download: .PDF

Download: .PDF

IRS Audit Representation and Dispute Resolution Contract

Download: .PDF

Download: .PDF

Tax Controversy Representation and Dispute Resolution Agreement

Download: .PDF

Download: .PDF

Agreement for IRS Advocacy and Dispute Resolution Services

Download: .PDF

Download: .PDF

IRS Tax Dispute Resolution and Power of Attorney Agreement

Download: .PDF

Download: .PDF

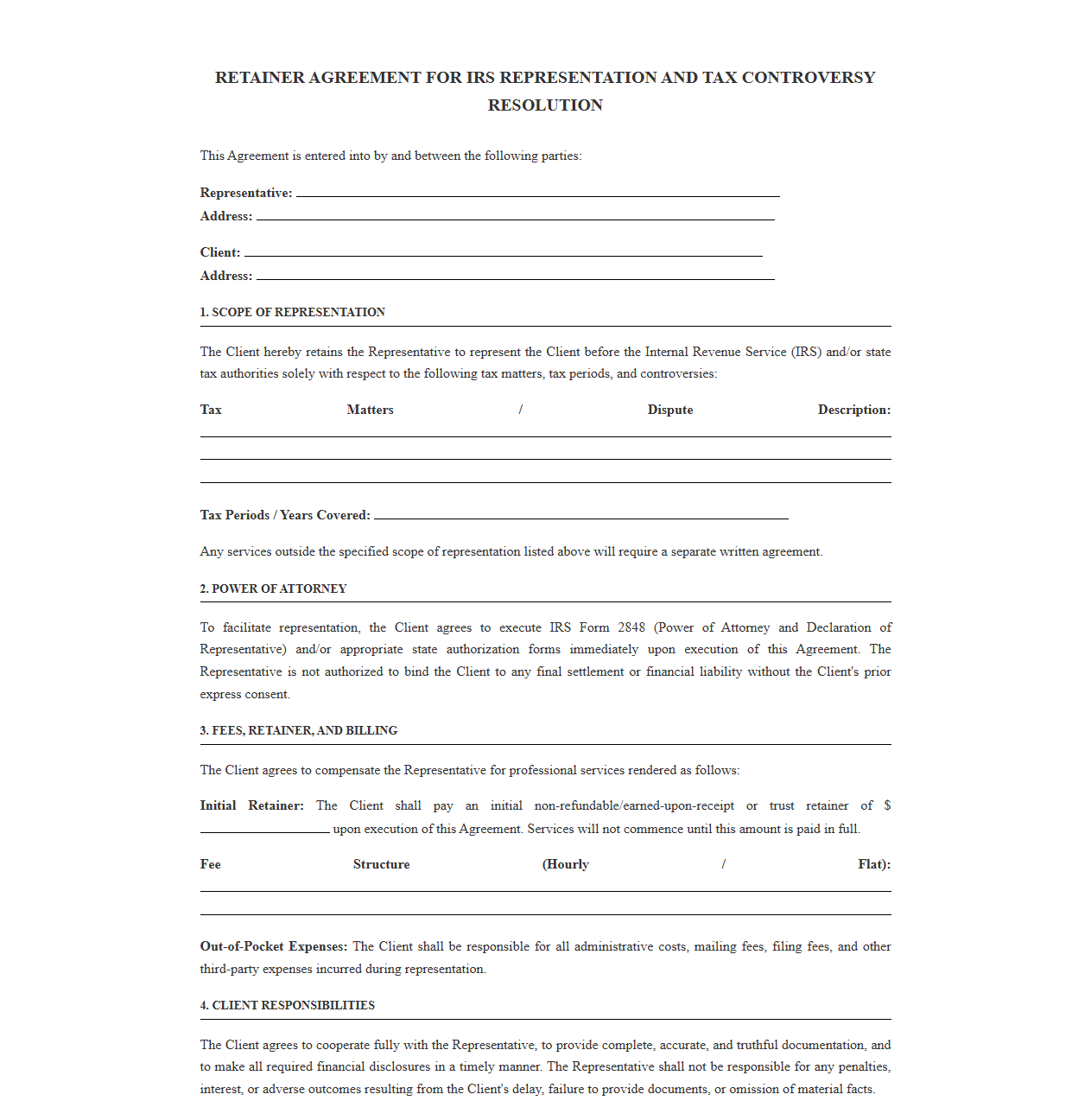

Retainer Agreement for IRS Representation and Tax Controversy

Download: .PDF

Download: .PDF

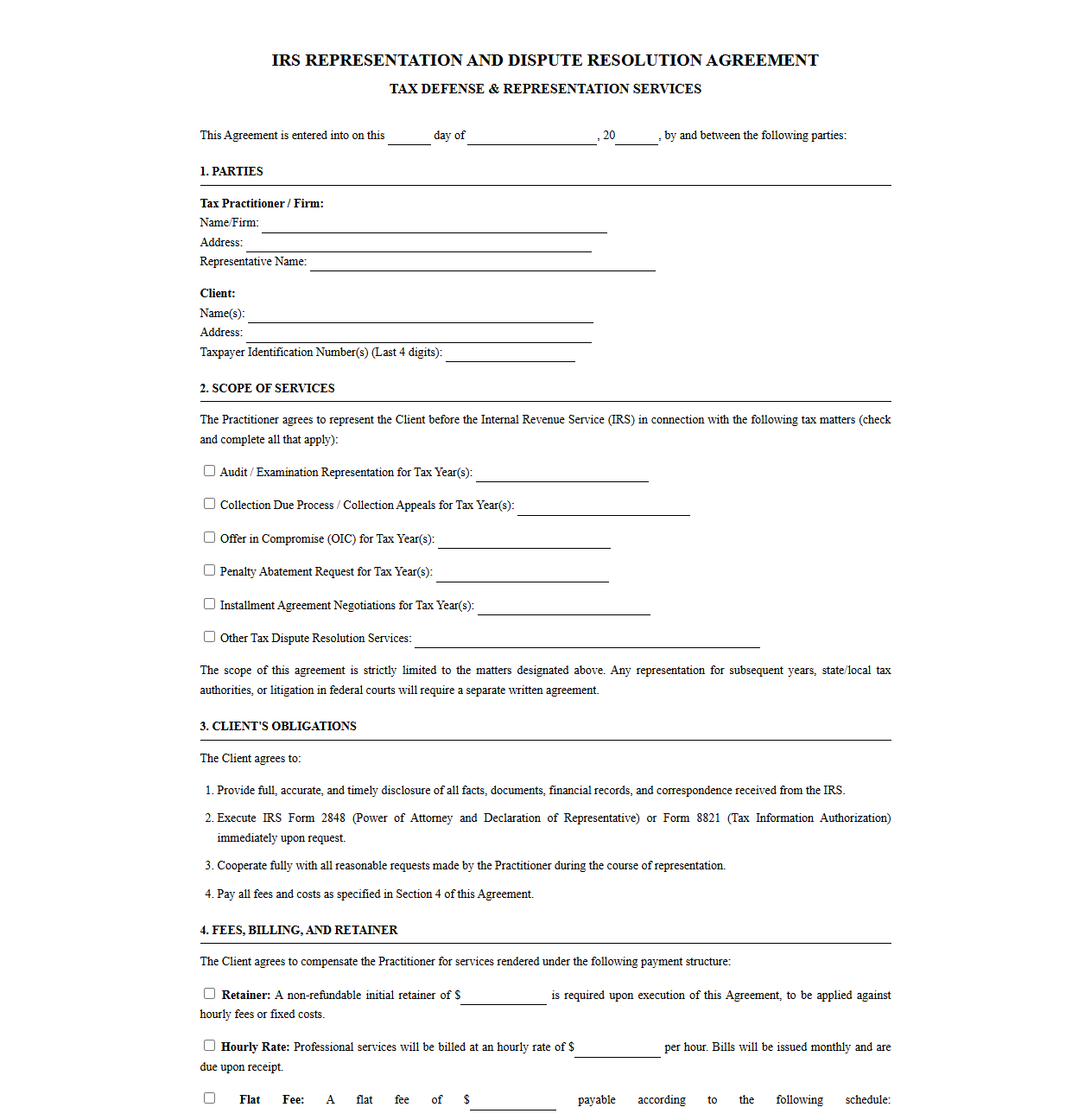

IRS Tax Defense and Dispute Resolution Agreement Template

Download: .PDF

Download: .PDF

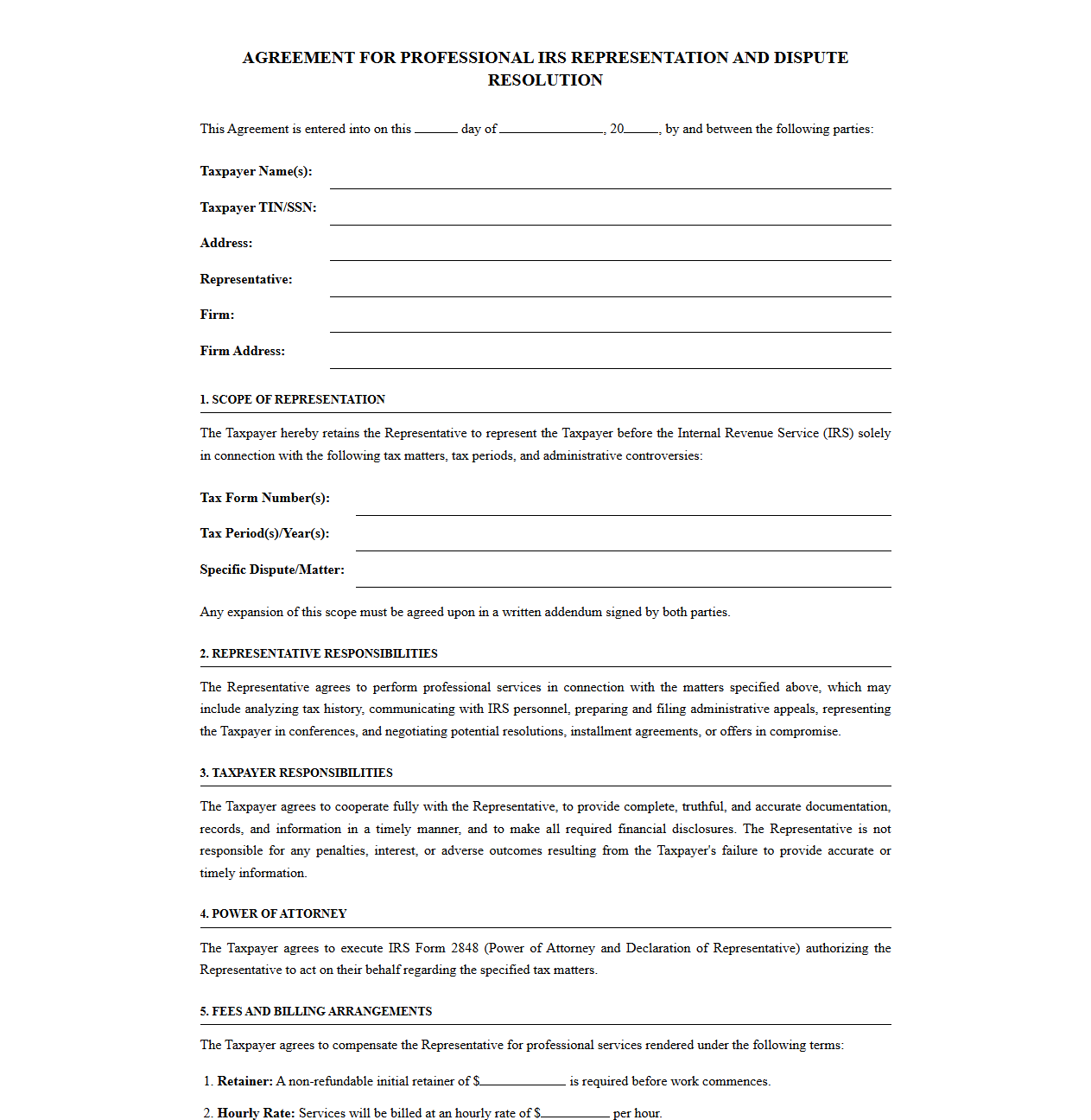

Agreement for Professional IRS Representation and Dispute Resolution

Download: .PDF

Download: .PDF

IRS Tax Settlement and Dispute Resolution Representation Agreement

Download: .PDF

Download: .PDF

Navigating IRS Disputes with Professional Representation

Facing the Internal Revenue Service (IRS) can be an incredibly daunting experience for any taxpayer. The complexities of tax codes, coupled with the aggressive nature of audit procedures, require a deep understanding of tax law. Engaging in these conflicts without a structured plan often leads to unfavorable outcomes. To mitigate these risks, a formal representation agreement is essential. A well-drafted agreement establishes a clear boundary of responsibilities, safeguarding the taxpayer from procedural missteps while protecting the tax professional's liability and operational boundaries during the dispute process.

Establishing Authority: The Power of Attorney Clause

A critical component of any tax representation strategy is the formal designation of authority. Within the contract, referencing and integrating IRS Form 2848 is vital. This specific form, known as the Power of Attorney and Declaration of Representative, legally authorizes a qualified tax professional to act and speak on behalf of the taxpayer before the IRS. By linking this document to the primary agreement, the representative can sign consents, receive confidential tax information, and negotiate directly with IRS agents. Taxpayers can review official guidelines on the IRS website to understand how this delegation of authority shifts the burden of communication away from the taxpayer and onto the practitioner.

Anatomy of a Standard Representation Agreement Template

To ensure a professional tax representation contract stands up to legal scrutiny, it must contain specific foundational clauses. These legal elements protect both parties and provide a clear roadmap for the engagement.

- Identification of Parties: Clearly naming the client and the authorized tax professional or firm.

- Recitals and Background: A brief statement explaining the context of the tax dispute.

- Governing Law: Specification of state laws that will govern the contract interpretation.

- Severability Clause: Ensuring that if one provision is found invalid, the rest of the contract remains in force.

Scope of Service: Defining Boundaries and Expectations

To prevent the dangerous phenomenon known as "scope creep," a representation agreement must explicitly detail the boundaries of the engagement. This means identifying the exact tax years and specific tax forms under examination. For example, representing a client for a 2021 Form 1040 audit does not automatically grant the professional authority or responsibility to handle a 2022 payroll tax issue. Clearly defining these boundaries ensures that the professional is not held liable for uncontracted periods and that the client is fully aware of what services they are paying for.

Fee Structures and Retainer Agreements

Establishing transparent financial expectations is critical to maintaining a healthy professional relationship. Tax professionals typically utilize several distinct compensation models depending on the complexity of the IRS dispute.

- Hourly Rates: Billing based on the actual time spent working on the case, suitable for unpredictable audits.

- Flat Fees: A single set price for a defined project, such as submitting an Offer in Compromise.

- Contingent Fees: Fees based on the outcome of the dispute, though heavily restricted by IRS Circular 230 rules.

In addition to the billing model, retainer provisions should be clearly outlined, specifying how upfront deposits are held in trust and drawn down as work progresses.

Client Responsibilities and Document Submission Protocols

The success of any tax resolution strategy depends heavily on client cooperation. The representation agreement must outline strict expectations regarding the client's duty to provide accurate, complete, and timely financial documentation. Failure to provide requested records can stall negotiations and lead to immediate penalties from the IRS. The agreement should clearly state that withholding information or providing falsified documents constitutes a material breach of contract, releasing the tax professional from further performance.

Termination Protocols and Conflict Resolution

A comprehensive agreement must plan for the end of the professional relationship, whether through successful resolution or premature termination. The protocol should outline how either party can terminate the agreement with written notice, and how outstanding fees will be calculated and settled. Unresolved disputes regarding services or billing should first be addressed through mediation before resorting to litigation. For additional guidance on ethical standards and professional conduct during termination, practitioners can consult the AICPA guidelines to ensure compliance with professional responsibilities.

Leave a comment