Manufacturing executives and financial controllers constantly battle fluctuating material prices and unpredictable variance, both of which quietly erode product profit margins. Before addressing these external market shifts, however, organizations must first establish a unified internal baseline for tracking raw inputs. Transitioning to a standardized Direct Materials Ledger template grants operations teams immediate control and cost predictability, whether they are managing volatile raw commodities like structural steel, industrial resins, or silicon chips.

Please note: While these templates drastically simplify variance analysis, they are intended to establish foundational logic rather than replace enterprise-grade ERP ledger systems.

Below, we will explore how to structure these templates effectively, calculate key material price variances, and implement a repeatable framework to eliminate costly manual accounting errors across your production lines.

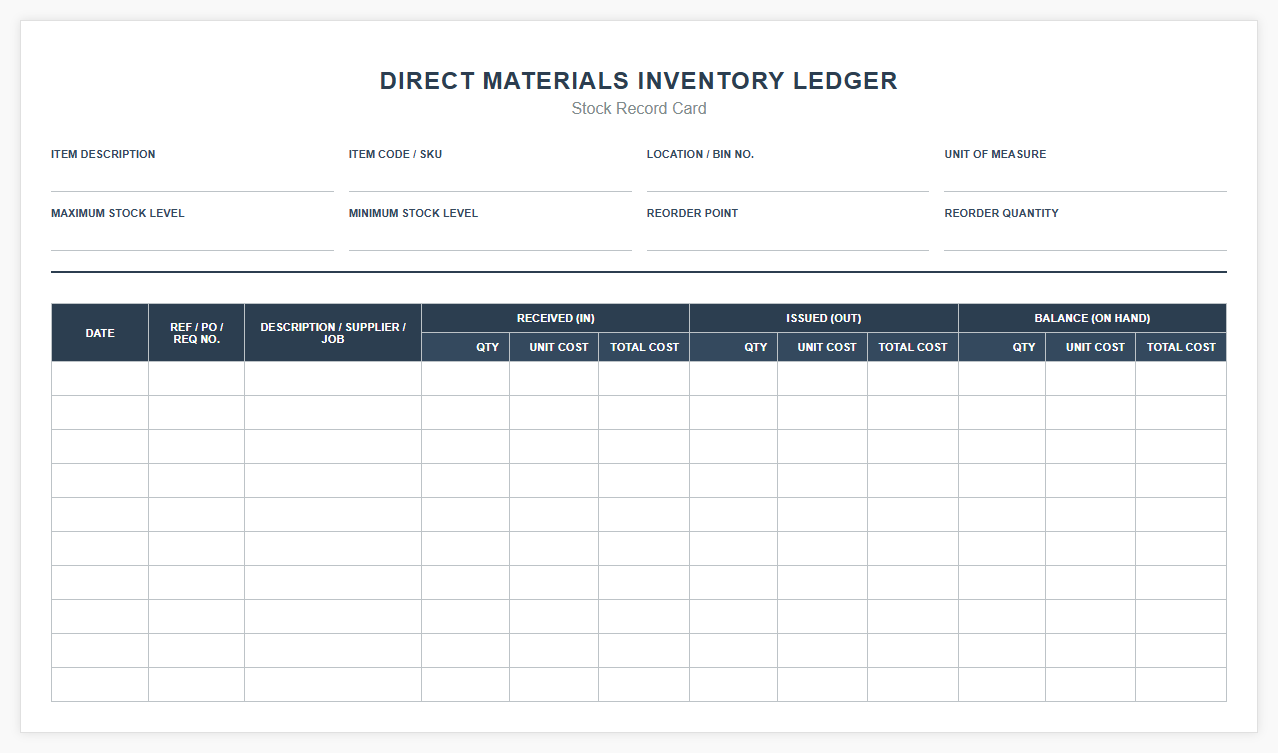

Direct Materials Inventory Ledger Spreadsheet

Download: .PDF

Download: .PDF

Manufacturing Raw Materials Cost Ledger Template

Download: .PDF

Download: .PDF

Bill of Materials Cost Tracking Ledger

![]() Download: .PDF

Download: .PDF

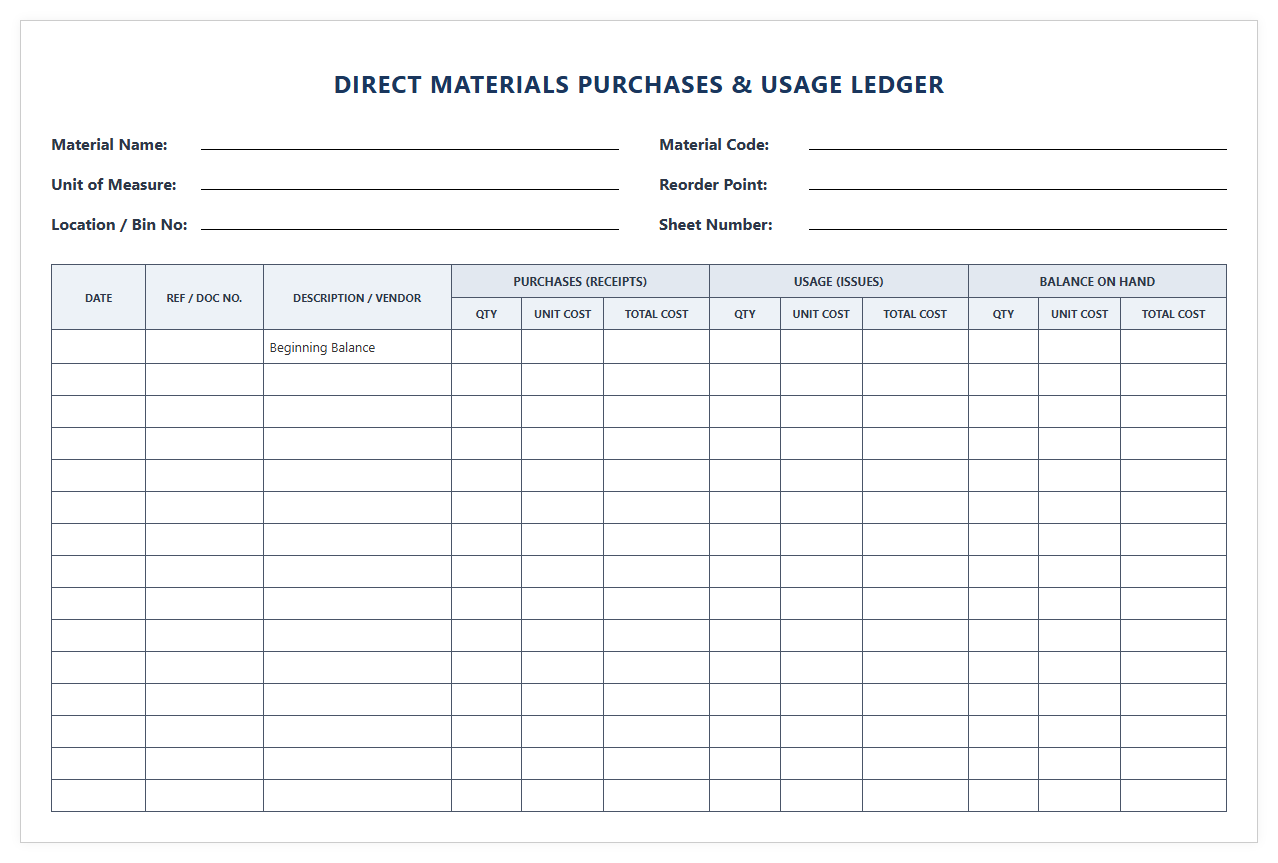

Direct Material Purchases and Usage Ledger

Download: .PDF

Download: .PDF

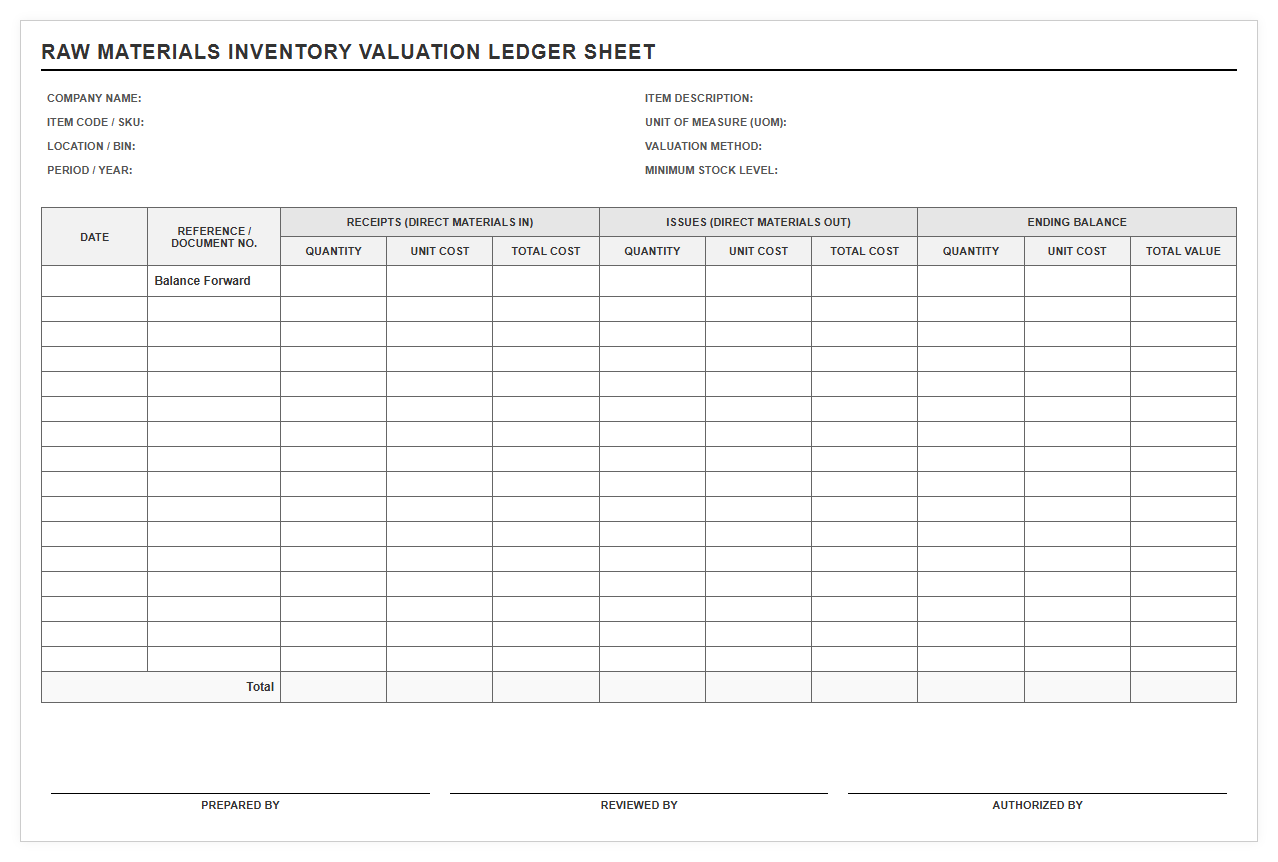

Raw Materials Inventory Valuation Ledger Sheet

Download: .PDF

Download: .PDF

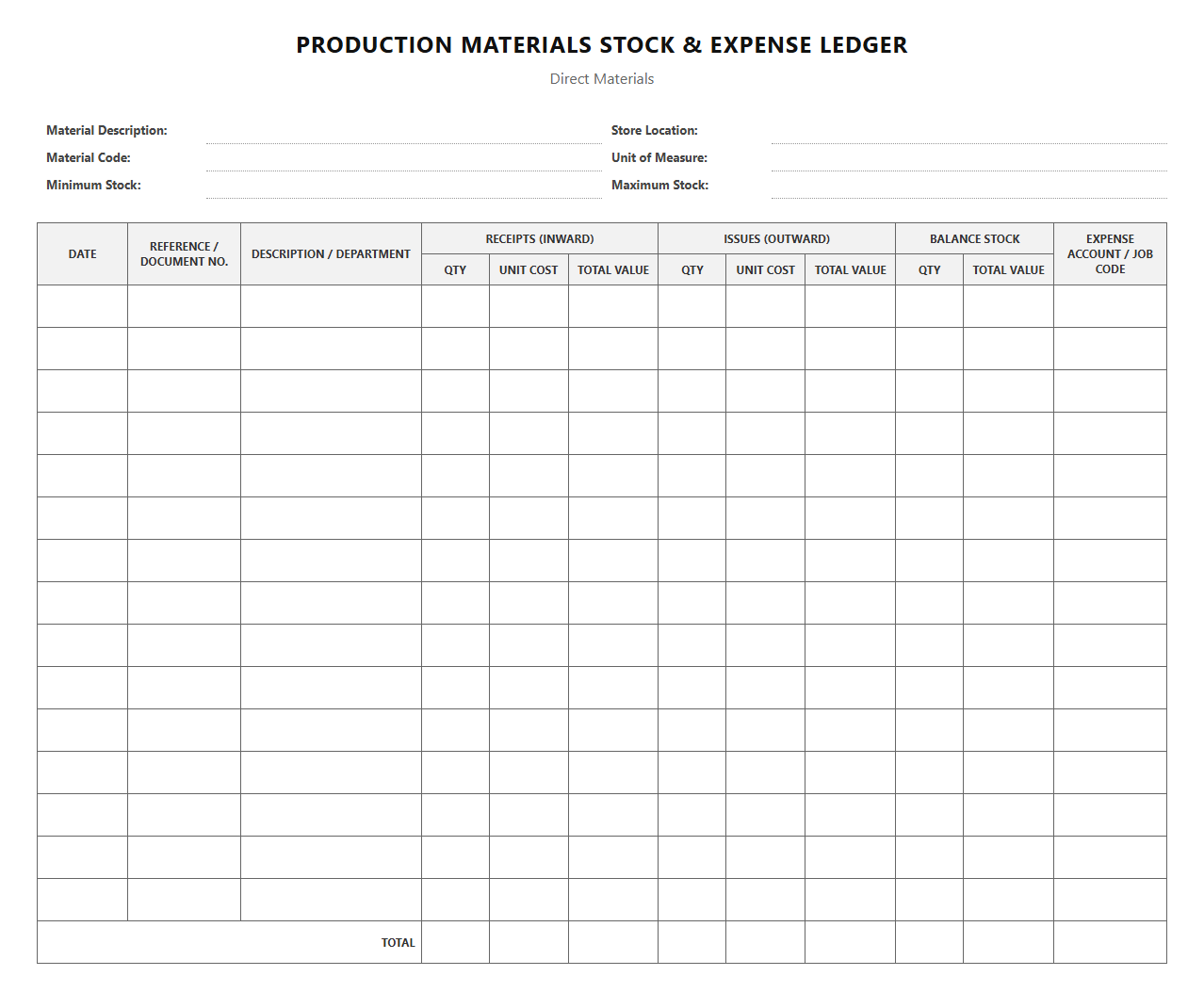

Production Materials Stock and Expense Ledger

Download: .PDF

Download: .PDF

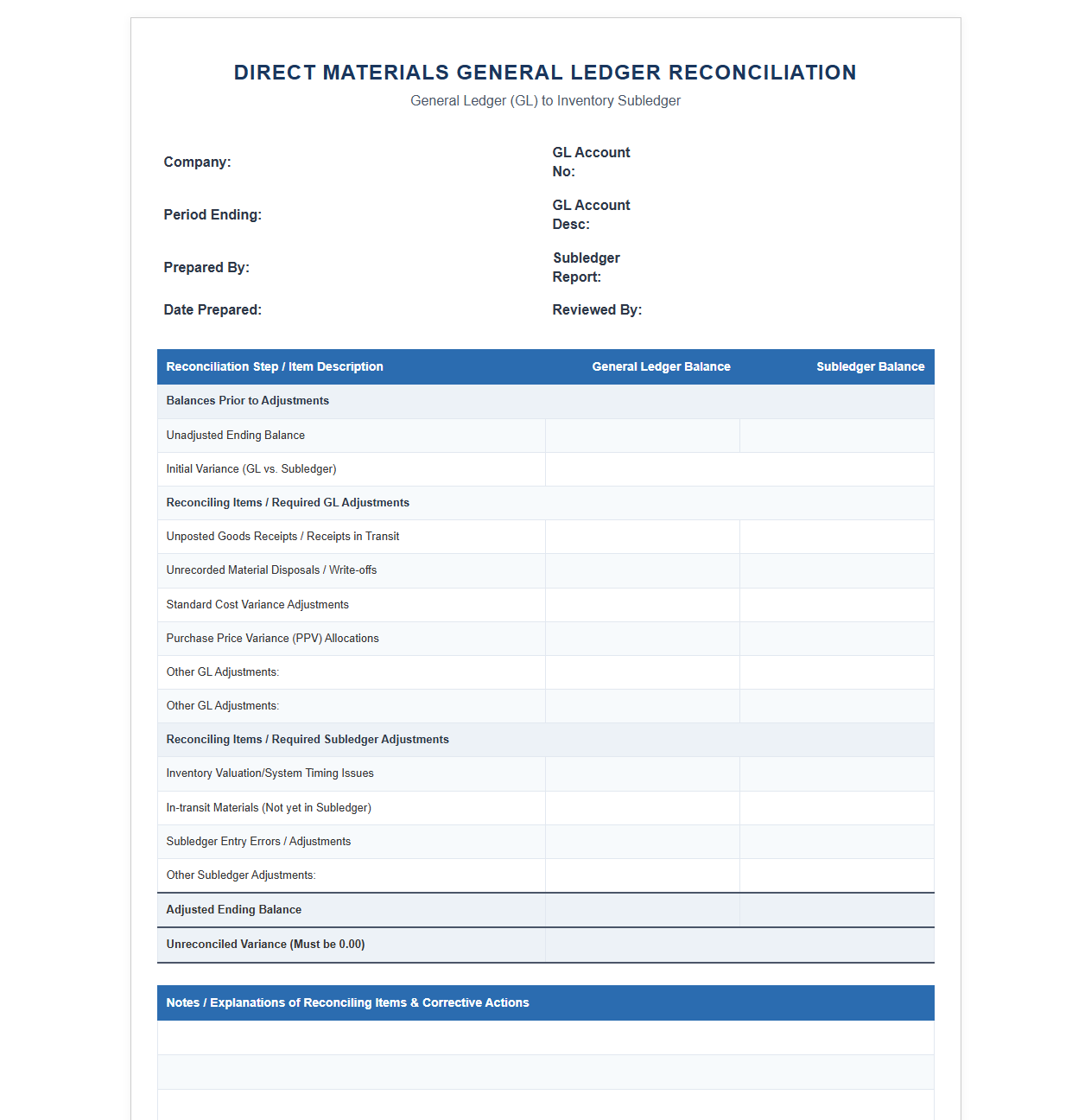

Direct Materials General Ledger Reconciliation Template

Download: .PDF

Download: .PDF

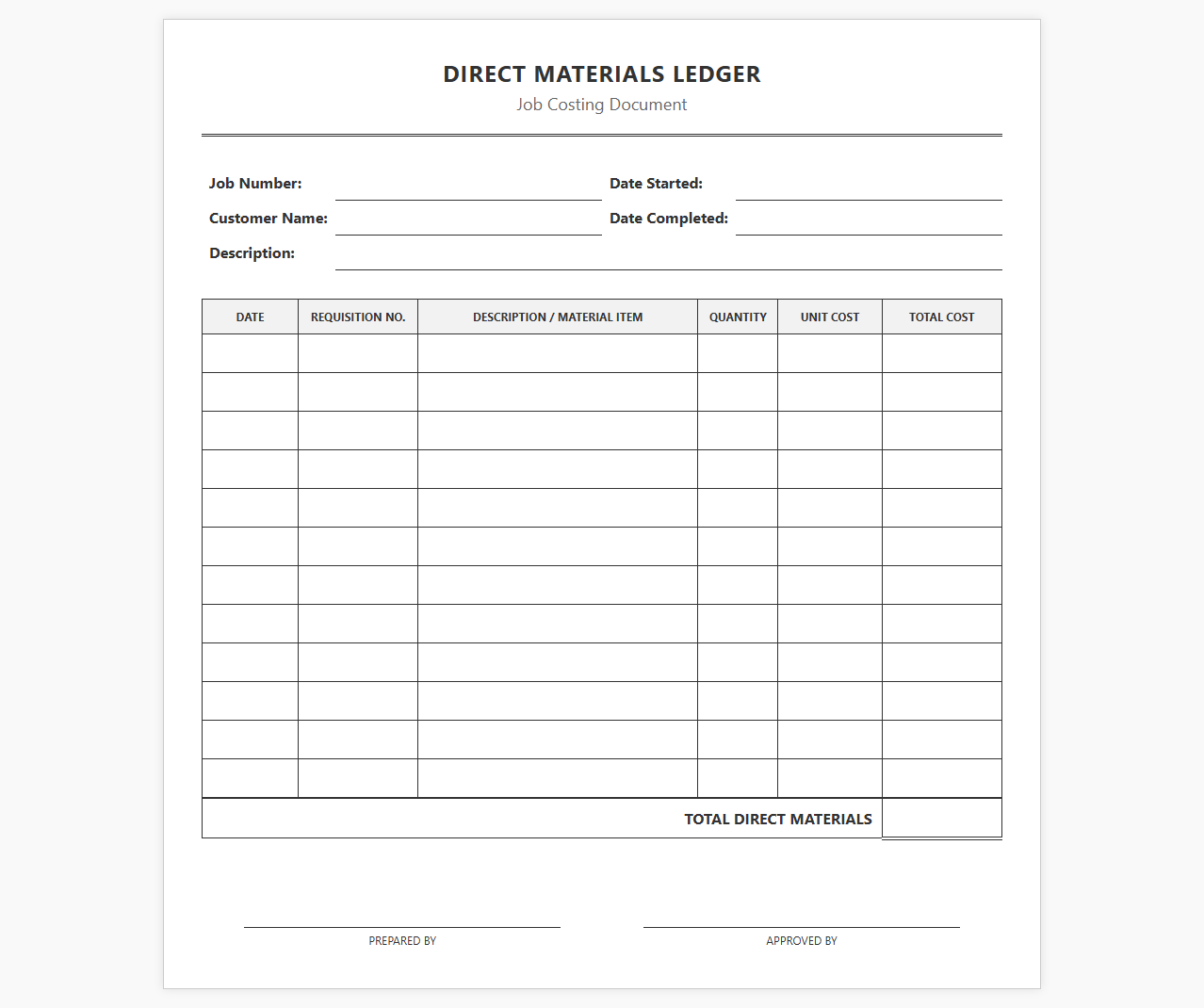

Job Costing Direct Materials Ledger Document

Download: .PDF

Download: .PDF

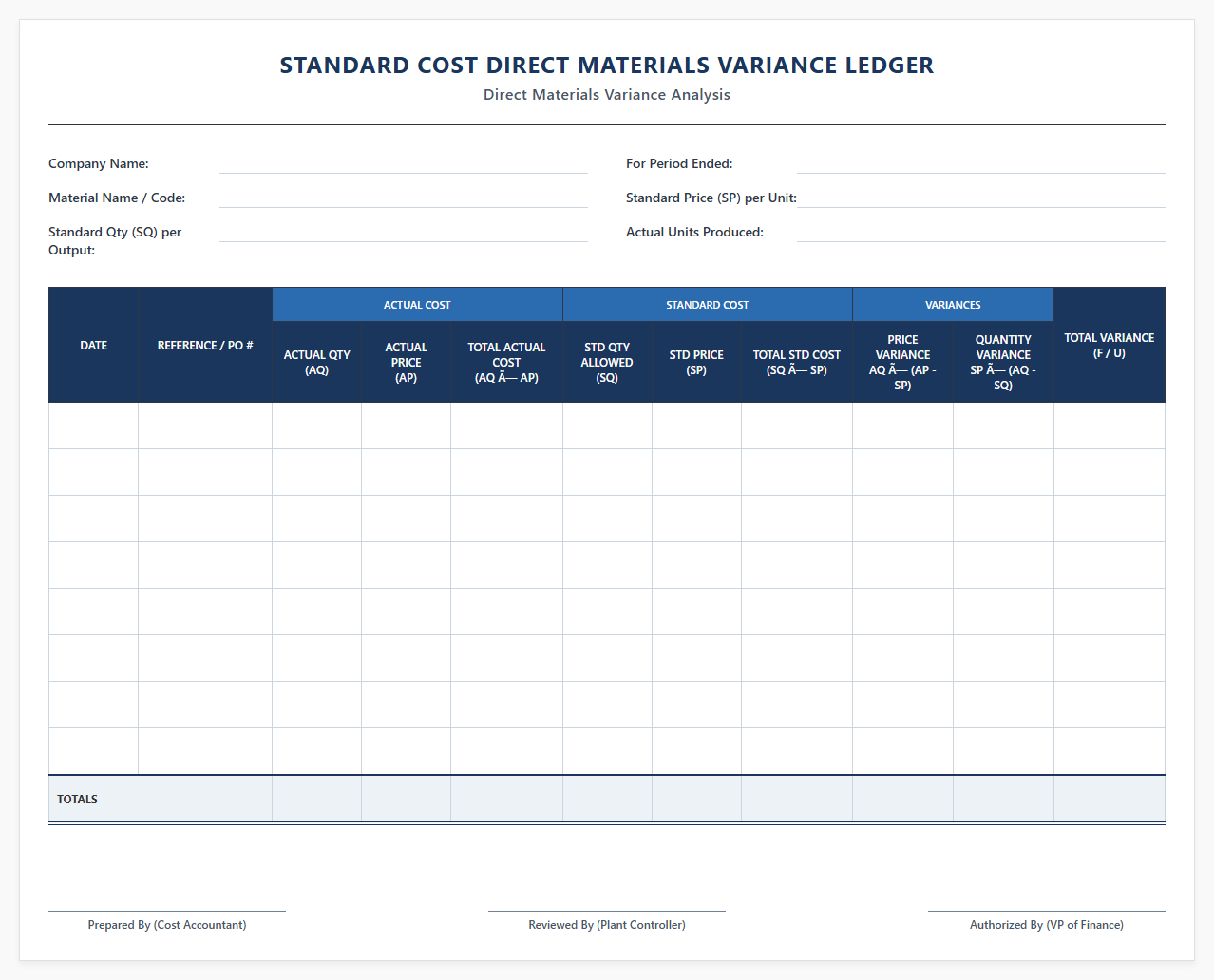

Standard Cost Direct Materials Variance Ledger

Download: .PDF

Download: .PDF

Introduction to Direct Materials Ledgers

In manufacturing, maintaining control over raw materials is the cornerstone of profitability. A direct materials ledger acts as the single source of truth for tracking every physical component that enters the production line. By establishing clear baselines for raw material costs, this ledger serves as the absolute foundation for standardizing production costs across all manufacturing runs.

The High Cost of Unstandardized Material Tracking

Without a standardized approach to tracking raw materials, manufacturing plants quickly fall victim to operational chaos. Financial risks multiply as price fluctuations go unnoticed, while inventory discrepancies lead to either costly stockouts or bloated warehouse overhead. When material tracking is fragmented, identifying the root cause of production waste becomes nearly impossible.

"Inconsistent record-keeping is the silent killer of manufacturing margins, turning minor scrap variances into major balance sheet losses."

Anatomy of an Effective Ledger Template

To ensure consistency across different shifts and production lines, a standardized ledger template must capture specific data points. A high-performing template relies on several core fields:

- Material ID and Description: Unique identifiers to prevent mix-ups between similar raw inputs.

- Standard Unit Cost: The budgeted cost per unit used to measure purchasing efficiency.

- Actual Unit Cost: The real price paid for the materials during acquisition.

- Standard Quantity: The pre-calculated amount of material required for the specific production volume.

- Actual Quantity Used: The physical amount of raw materials consumed on the shop floor.

- Variance Columns: Auto-calculated fields highlighting both price and usage deviations.

Implementing Templates in Daily Production Workflows

Bridging the gap between accounting and physical production requires structured daily habits. Floor managers and cost accountants must work in tandem to keep ledger data accurate and actionable.

- The accounting team pre-populates the template with the standard material costs before the production run begins.

- Floor managers log physical material withdrawals and actual quantities used at the end of every shift.

- The system automatically calculates differences between standard and actual quantities in real-time.

- Accountants review these daily entries to flag immediate anomalies before they affect the final assembly costs.

Analyzing Variances to Control Cost Overruns

Variance analysis turns raw numbers into actionable business intelligence. By separating material price deviations from quantity usage deviations, management can pinpoint exactly where money is being saved or lost.

| Variance Type | Formula | Primary Cause | Corrective Action |

|---|---|---|---|

| Price Variance | (Actual Price - Standard Price) x Actual Quantity | Supplier price hikes or rush shipping fees | Negotiate bulk contracts or find alternative vendors |

| Quantity Variance | (Actual Quantity - Standard Quantity) x Standard Price | Machine malfunction, low quality raw inputs, or operator error | Calibrate equipment or retrain floor personnel |

Choosing the Right Tool: Spreadsheets vs. Dedicated Software

Small to mid-sized manufacturers often start with Excel or Google Sheets templates because they are highly flexible and require minimal upfront investment. These tools allow rapid changes to formulas and layouts. However, manual data entry in spreadsheets is highly susceptible to human error, and version control issues frequently arise when multiple team members edit the same file.

In contrast, upgrading to an integrated ERP ledger module automates data collection directly from the warehouse and shop floor. While ERP solutions require a larger financial commitment and extensive training, they remove the risk of manual input errors and provide real-time cost visibility that static spreadsheets simply cannot match.

Achieving Long-Term Financial Predictability

Standardizing direct materials ledgers is not a one-time project, but an ongoing operational discipline. To maintain accuracy, companies must perform regular audits of their standard costs to reflect current market realities and update material formulations. Consistent calibration of these ledger metrics ensures that pricing strategies remain accurate and profit margins stay protected against inflationary pressures.

Leave a comment