For many nonprofits and corporate donors, documenting non-cash contributions is a complex administrative hurdle. Minor omissions on an equipment receipt can trigger IRS audits, invalidate deductions, and disrupt corporate asset depreciation schedules. Navigating these stringent regulatory frameworks requires a standardized approach to record-keeping before valuation can even begin.

Implementing a rigorous documentation process grants organizations absolute audit readiness while securing maximum tax advantages for donors. Please note, however, that while a structured template establishes a vital legal paper trail, it must serve as a compliance framework rather than a substitute for professional certified appraisals. This distinction is critical when documenting high-value assets such as enterprise IT servers, specialized medical devices, or heavy machinery.

In this article, we will outline the essential clauses every receipt must contain, examine IRS valuation requirements, and provide a customizable template to streamline your compliance workflow.

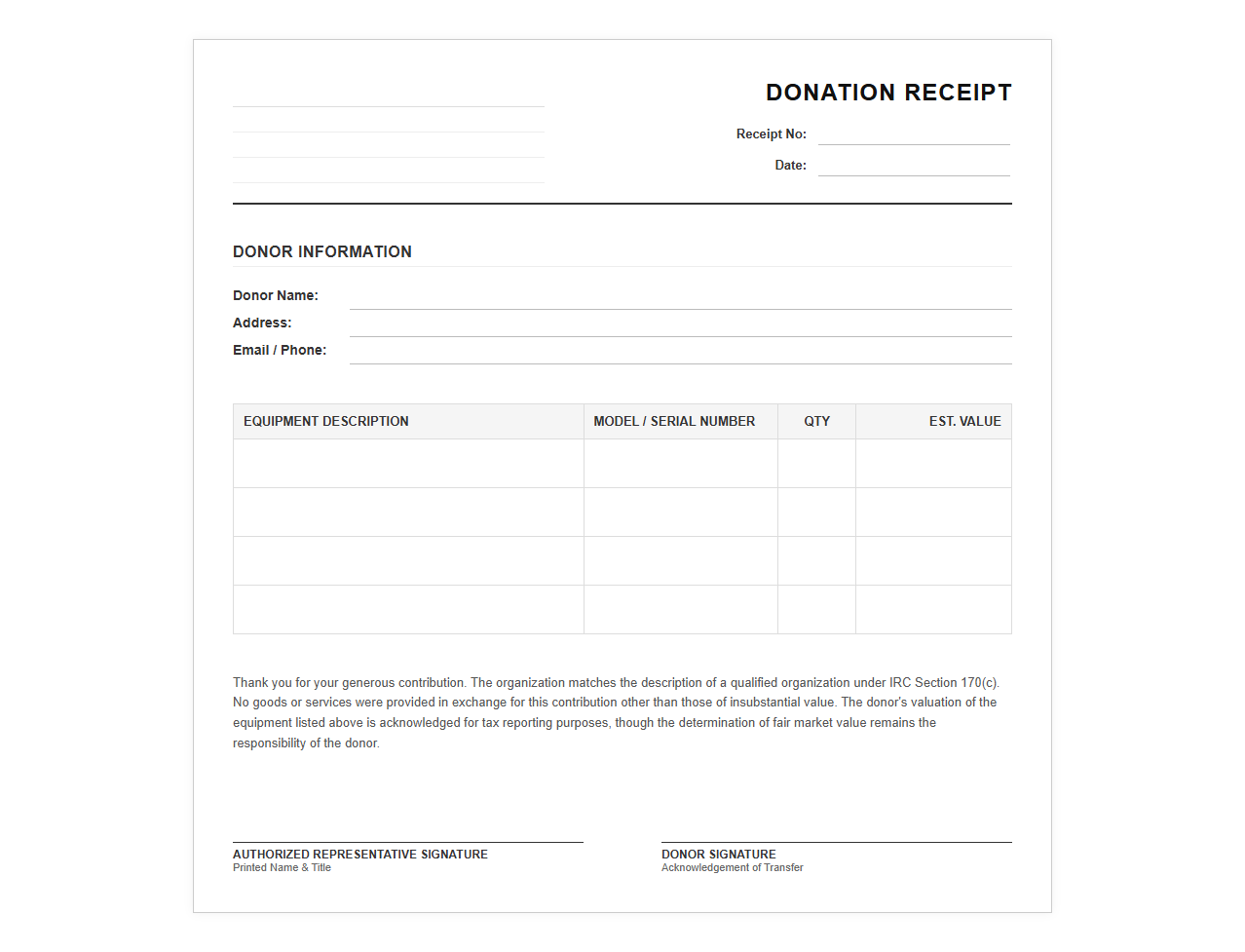

Equipment Donation Receipt Template

Download: .PDF

Download: .PDF

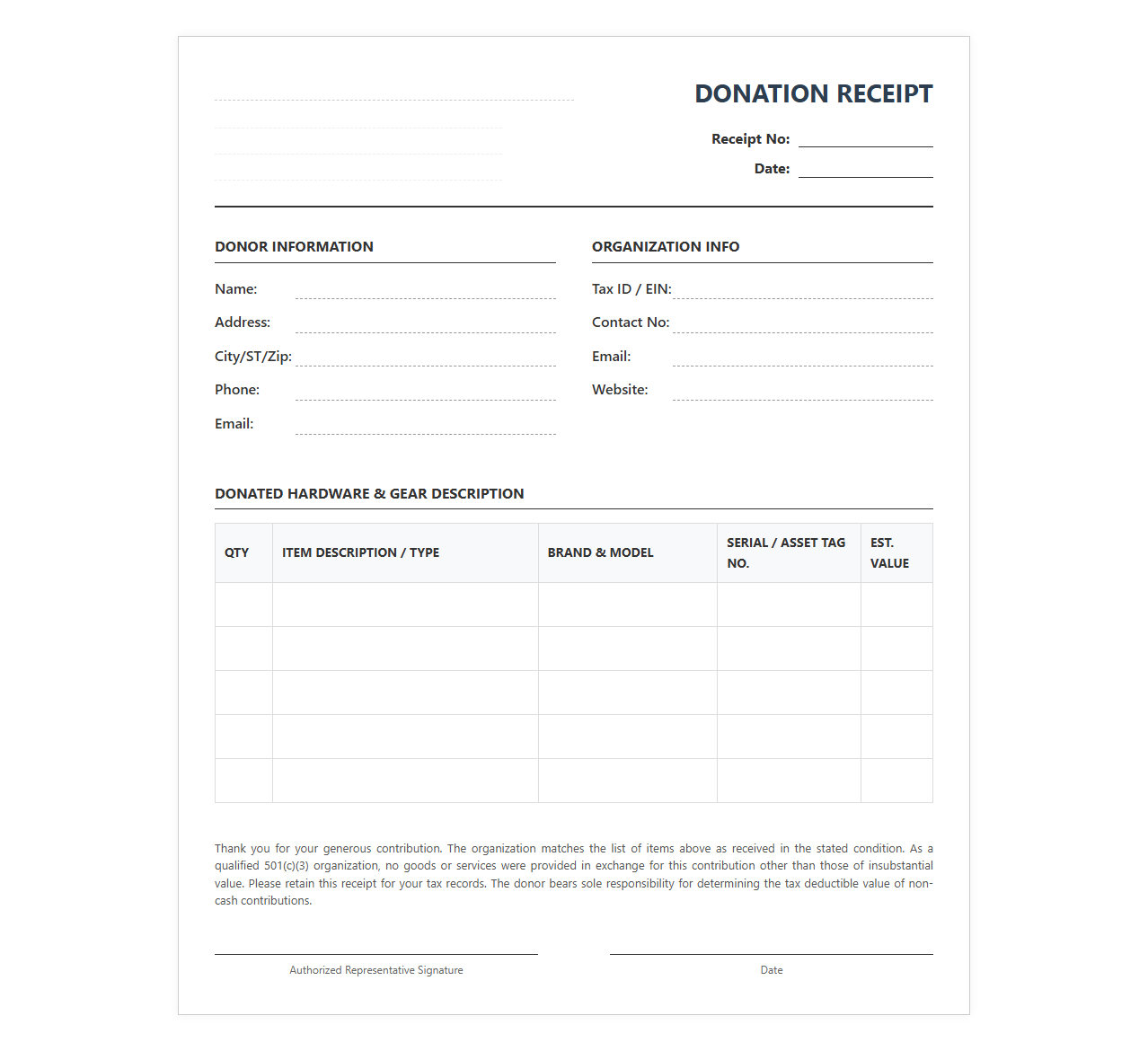

Hardware and Gear Donation Receipt

Download: .PDF

Download: .PDF

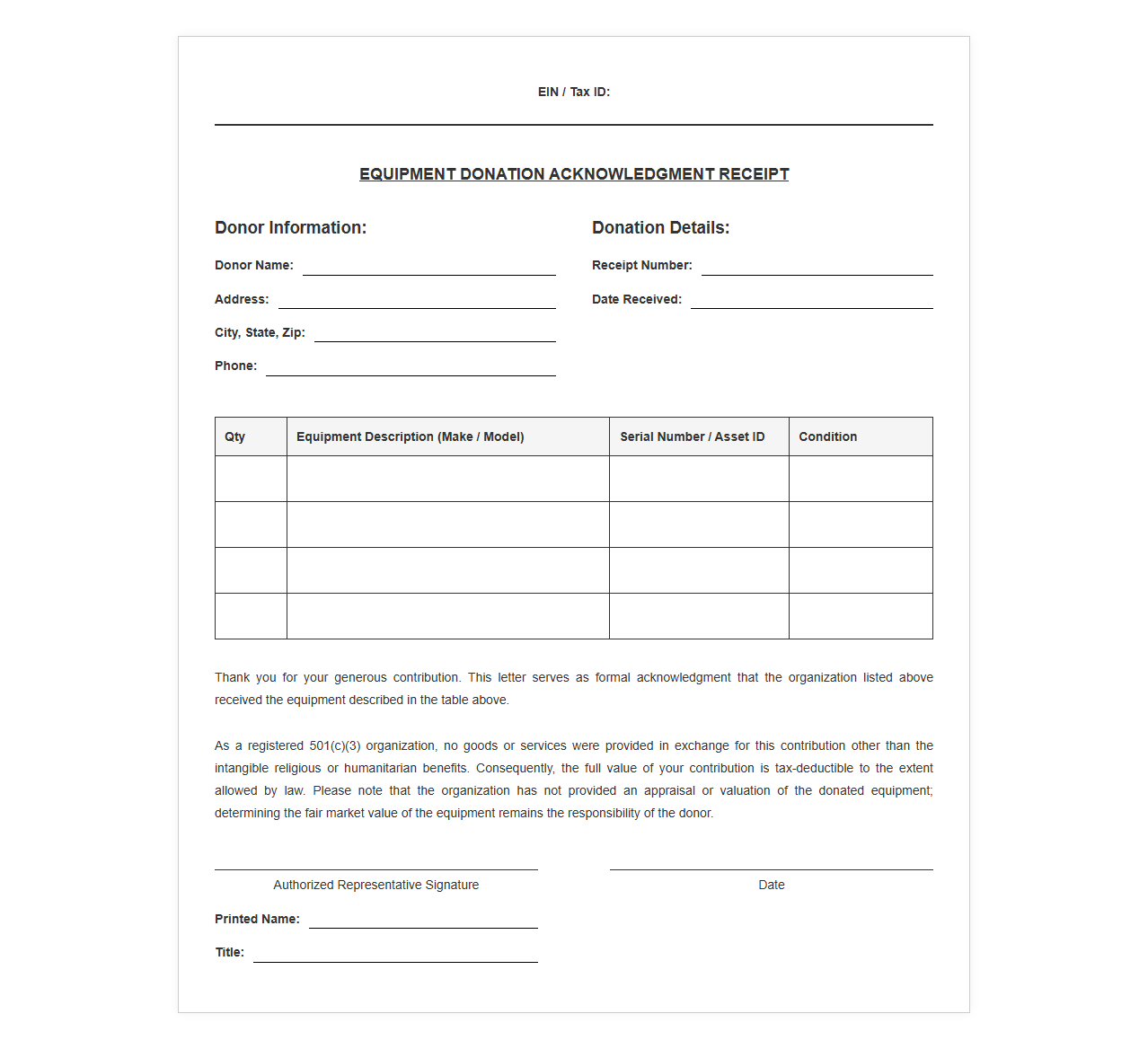

Non-Profit Equipment Gift Acknowledgment Letter

Download: .PDF

Download: .PDF

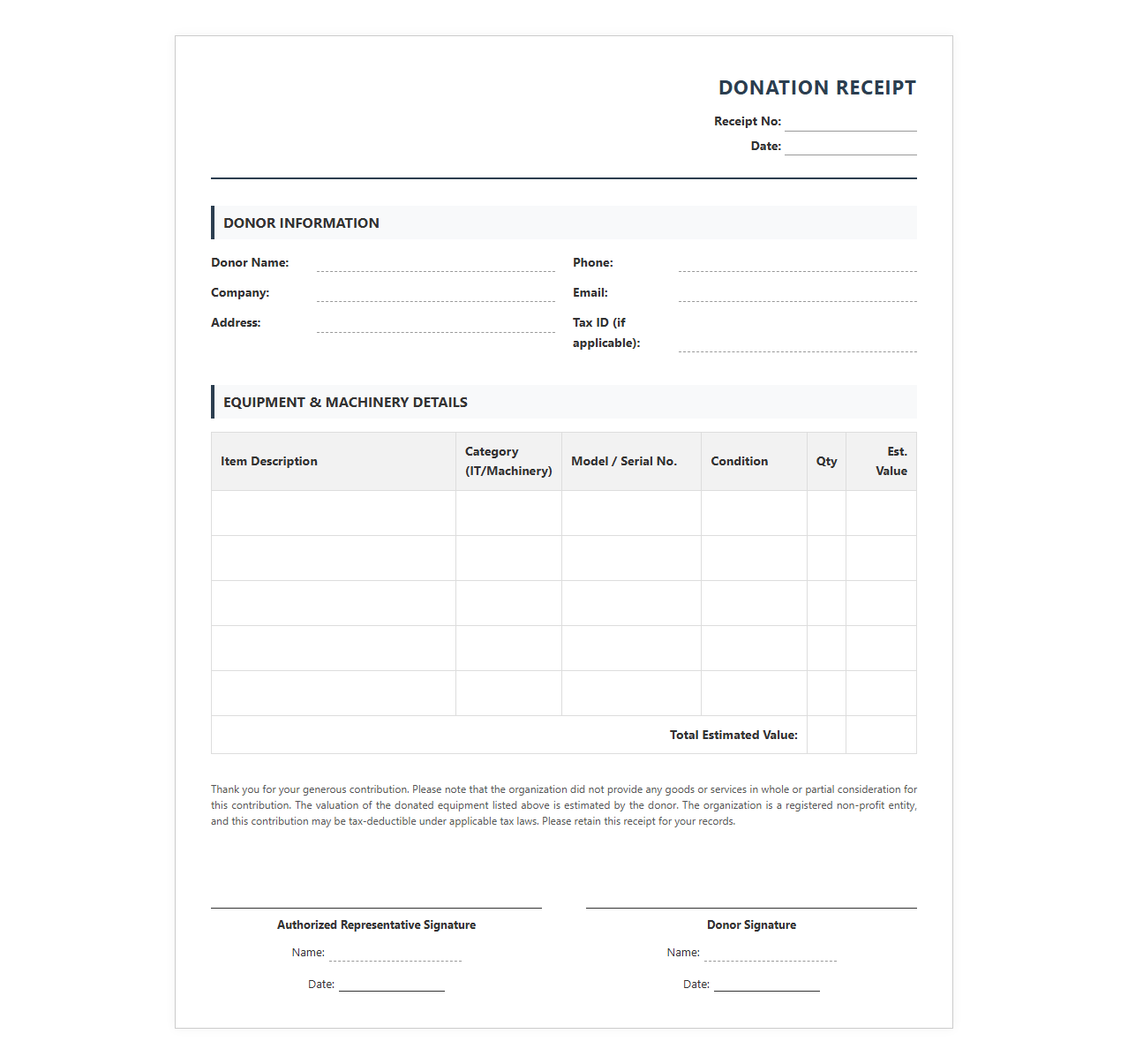

IT and Machinery Donation Receipt Form

Download: .PDF

Download: .PDF

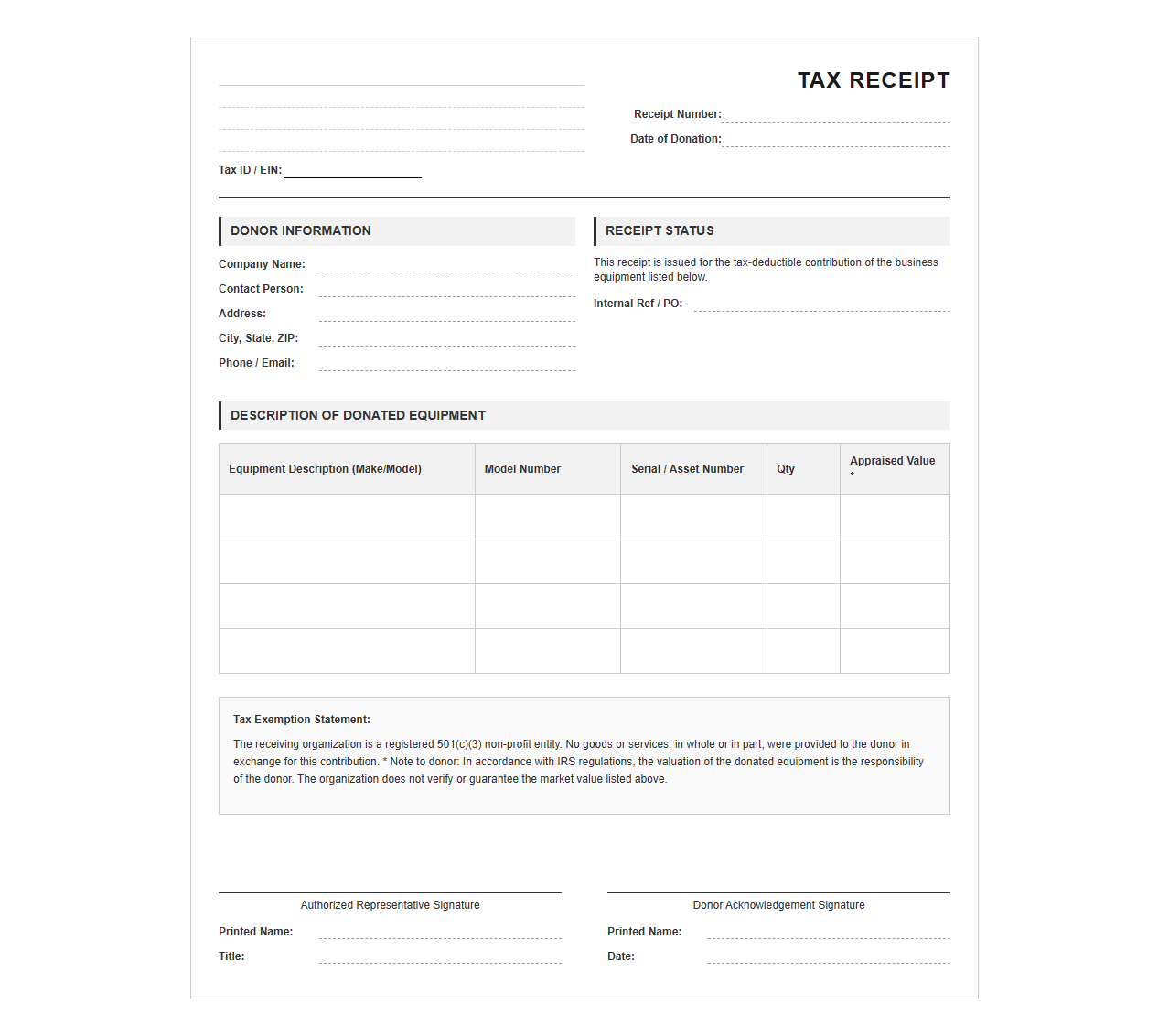

Tax Receipt for Donated Business Equipment

Download: .PDF

Download: .PDF

Charitable Equipment Contribution Receipt Template

Download: .PDF

Download: .PDF

Equipment Gift-in-Kind Donation Receipt

Download: .PDF

Download: .PDF

Official Receipt for Donated Equipment

Download: .PDF

Download: .PDF

Corporate Equipment Donation Acknowledgment Template

Download: .PDF

Download: .PDF

The Foundations of Compliant Equipment Donation Receipts

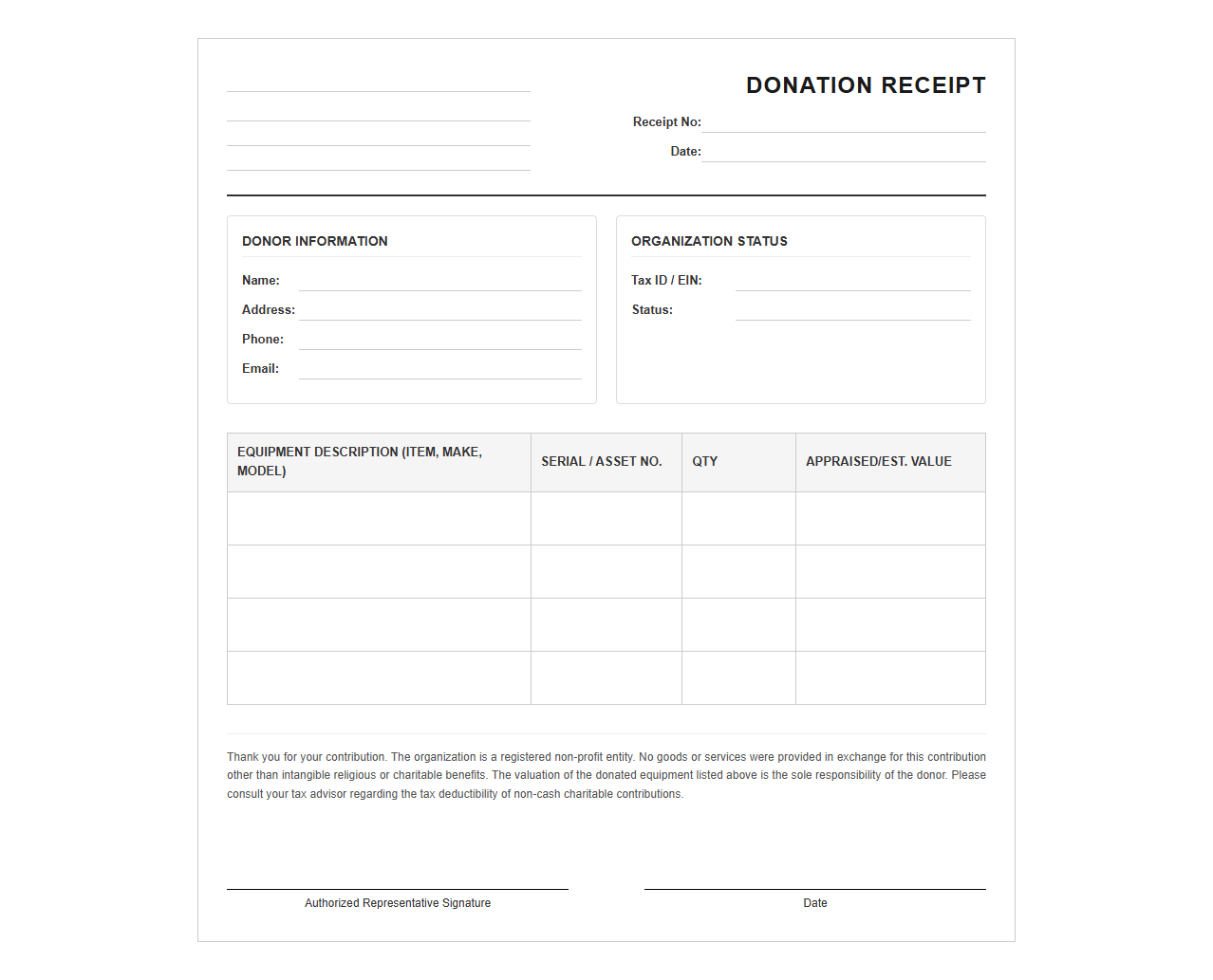

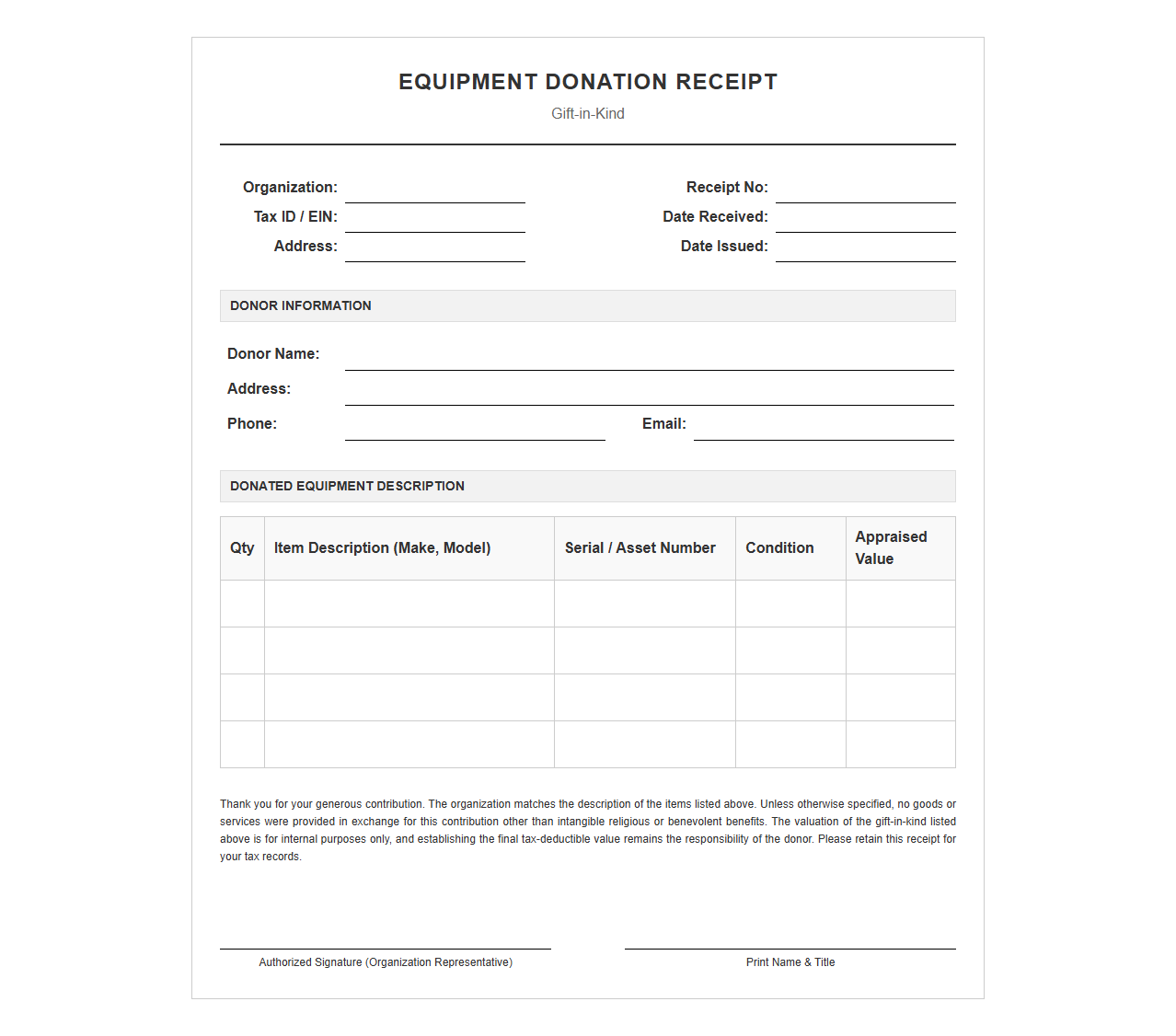

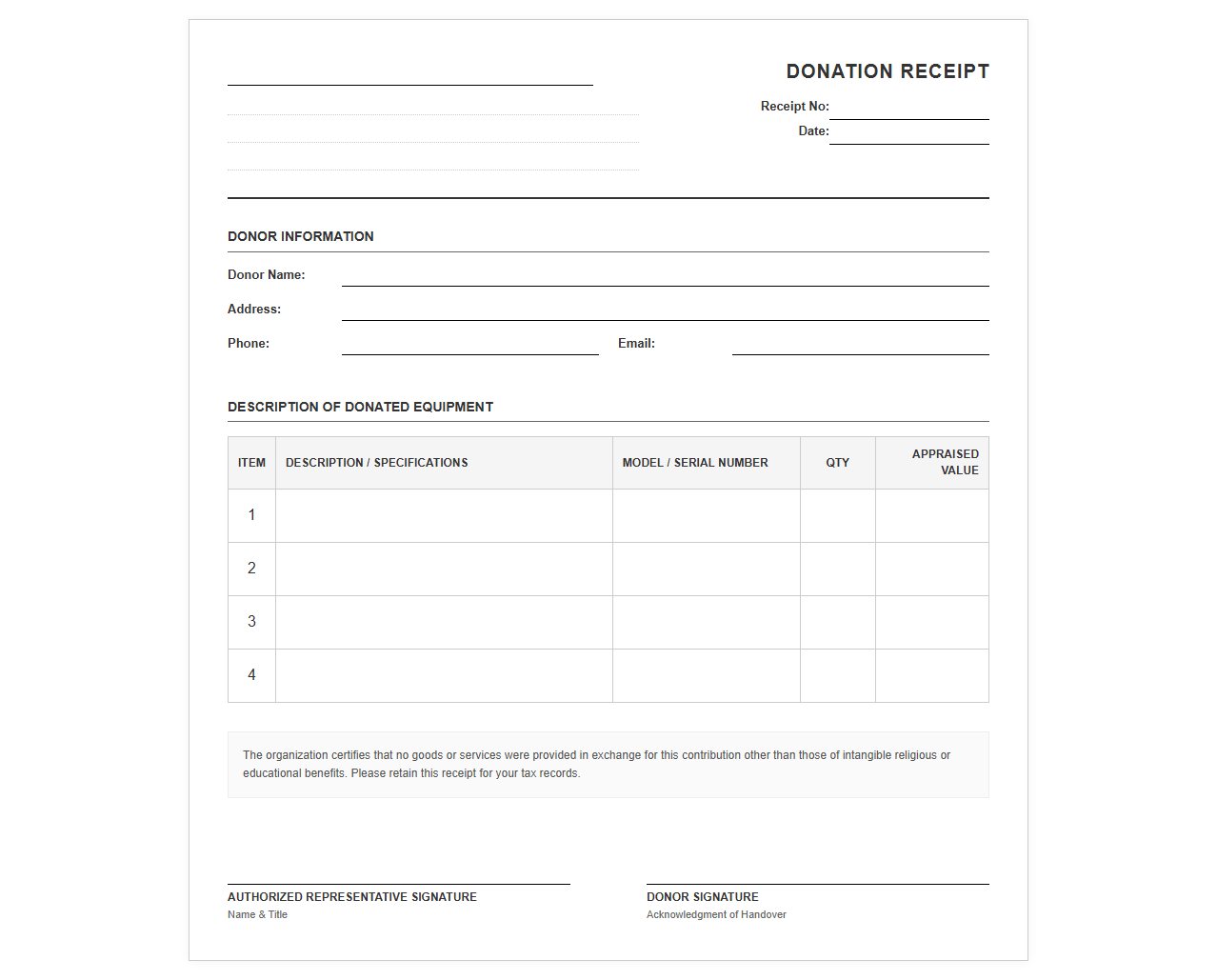

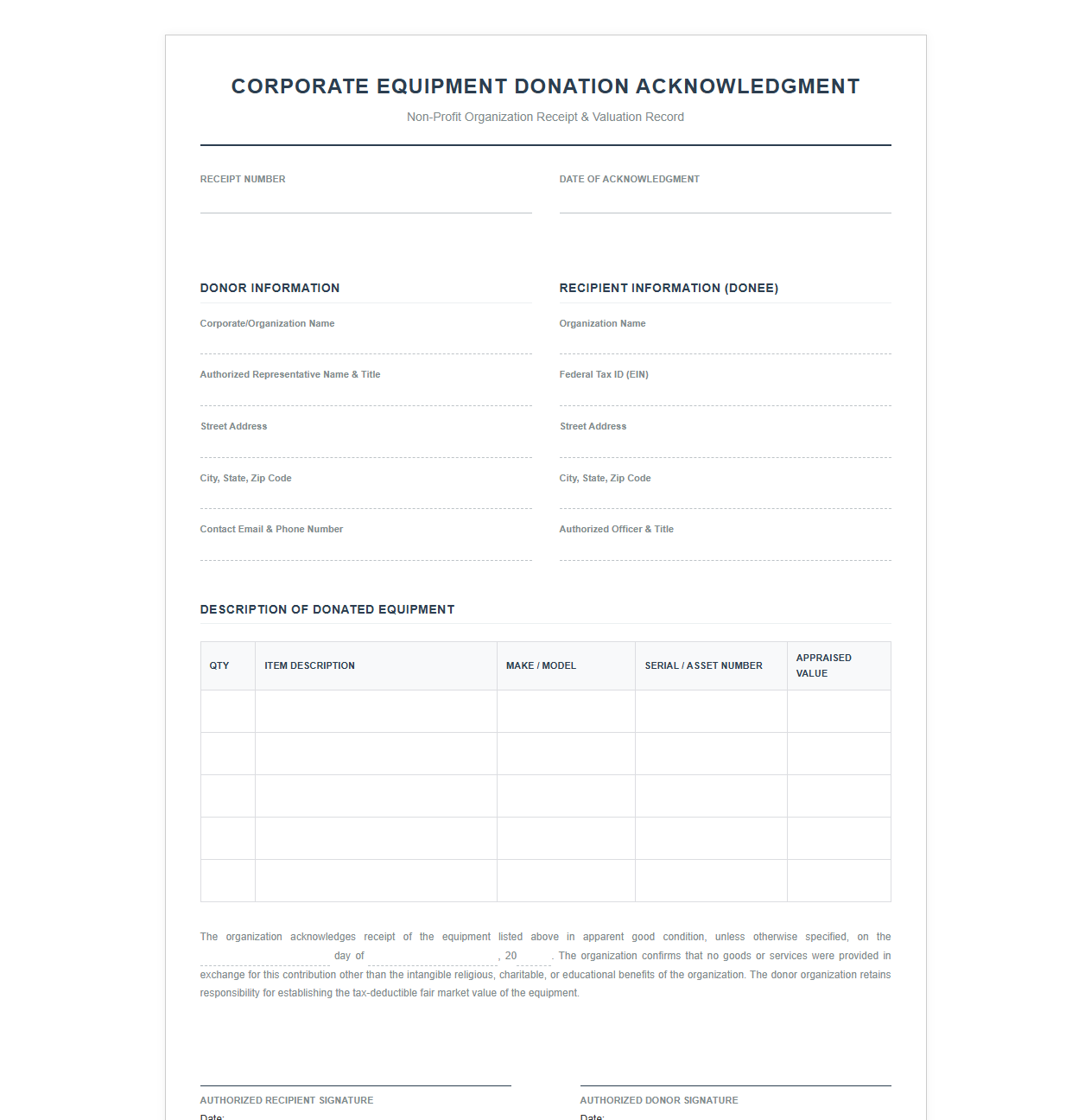

When organizations donate or receive physical assets, utilizing a structured receipt template is a necessity for financial compliance. These documents serve as the primary verification link between corporate stewardship and tax regulation. Ensuring that every transaction is documented accurately allows businesses to claim valid tax deductions while maintaining impeccable internal corporate asset tracking. Correct documentation satisfies both IRS compliance requirements and standard accounting principles (GAAP), protecting both parties during financial audits.

Essential Donor and Organization Identity Fields

To establish an audit-ready paper trail, a donation receipt must clearly identify both the donating entity and the recipient organization. Complete transparency in these identity fields prevents compliance delays and verifies the legitimacy of the tax-exempt transaction.

- Donor's Complete Identity: Full legal corporate name, primary business address, and contact information.

- Recipient Organization Details: Legal name of the nonprofit or institution, mailing address, and phone number.

- Tax-Exempt Status Verification: The recipient's federal Employer Identification Number (EIN) or equivalent tax ID.

Itemized Equipment Description and Condition Reporting

A vague description of donated property can jeopardize tax deductions and complicate asset valuation. Organizations must follow a standardized process to detail the physical assets accurately.

- Record the manufacturer brand name, official model number, and unique serial numbers for each unit.

- Specify the exact quantity of items included in the shipment.

- Provide an objective assessment of the equipment's physical condition, categorizing it as new, refurbished, good, or salvageable.

Determining Asset Valuation and Tax Compliance Rules

Determining the Fair Market Value (FMV) of donated equipment is the responsibility of the donor, but the receipt must reflect the parameters of this valuation. IRS guidelines dictate strict thresholds for reporting non-cash charitable contributions, demanding higher levels of substantiation as the asset value increases.

According to tax regulations, for non-cash donations exceeding $5,000, donors must obtain a qualified appraisal prepared by a qualified appraiser and complete IRS Form 8283 to support their tax deduction claims.

Incorporating Legal Disclaimers and No-Goods-Exchanged Clauses

To satisfy federal tax requirements, the receipt must contain explicit legal language confirming the nature of the transaction. Without this statement, the donor cannot legally claim a tax deduction for the contribution.

The document must clearly state that the recipient organization provided no goods or services in consideration, in whole or in part, for the contributions detailed in the receipt, or otherwise specify the estimated value of any goods or services provided in return.

Designing Authorized Signature and Date Blocks

A receipt is not legally binding without proper authorization. The design must feature dedicated, clear areas for signatures and dates to verify when the physical transfer of assets occurred.

Include distinct signature lines for both the representative of the receiving organization and the delivering agent to confirm receipt of the specific equipment listed.

Digital Archiving and Asset Tracking Integration

Modern compliance demands moving beyond paper receipts into digitized asset ecosystems. Integrating donation records directly into enterprise resource planning (ERP) or fixed asset management software ensures that decommissioned equipment is properly removed from active balance sheets. Digital archiving secures the required audit trails for the necessary seven-year retention period, providing instant accessibility during regulatory reviews.

To learn more about aligning your financial records with federal valuation rules, refer to the established IRS asset valuation standards.

Leave a comment