Chief Financial Officers and risk managers frequently struggle to predict how sudden market volatility will impact liquidity, often relying on lagging indicators that fail to flag impending deficits. Before investing in complex, automated predictive software, organizations must first establish a standardized analytical foundation. Achieving this structural alignment grants finance teams the immediate clarity needed to stress-test liquidity under extreme economic scenarios.

However, we must stipulate that sensitivity templates are strategic frameworks, not crystal balls; their predictive efficacy depends entirely on the precision of your baseline operational assumptions. For example, accurately modeling a 200-basis-point interest rate hike or a 15% spike in supply chain costs requires meticulous, clean historical inputs to yield actionable insights.

In this article, we will examine essential cash flow sensitivity templates, break down critical risk variables, and outline a step-by-step methodology to integrate these tools into your existing financial reporting.

Cash Flow Sensitivity Analysis Report Template

Download: .PDF

Download: .PDF

Sensitivity Analysis Model for Cash Flow Statements

Download: .PDF

Download: .PDF

Cash Flow Scenario Planning and Sensitivity Template

Download: .PDF

Download: .PDF

Cash Flow Stress Test and Sensitivity Statement

Download: .PDF

Download: .PDF

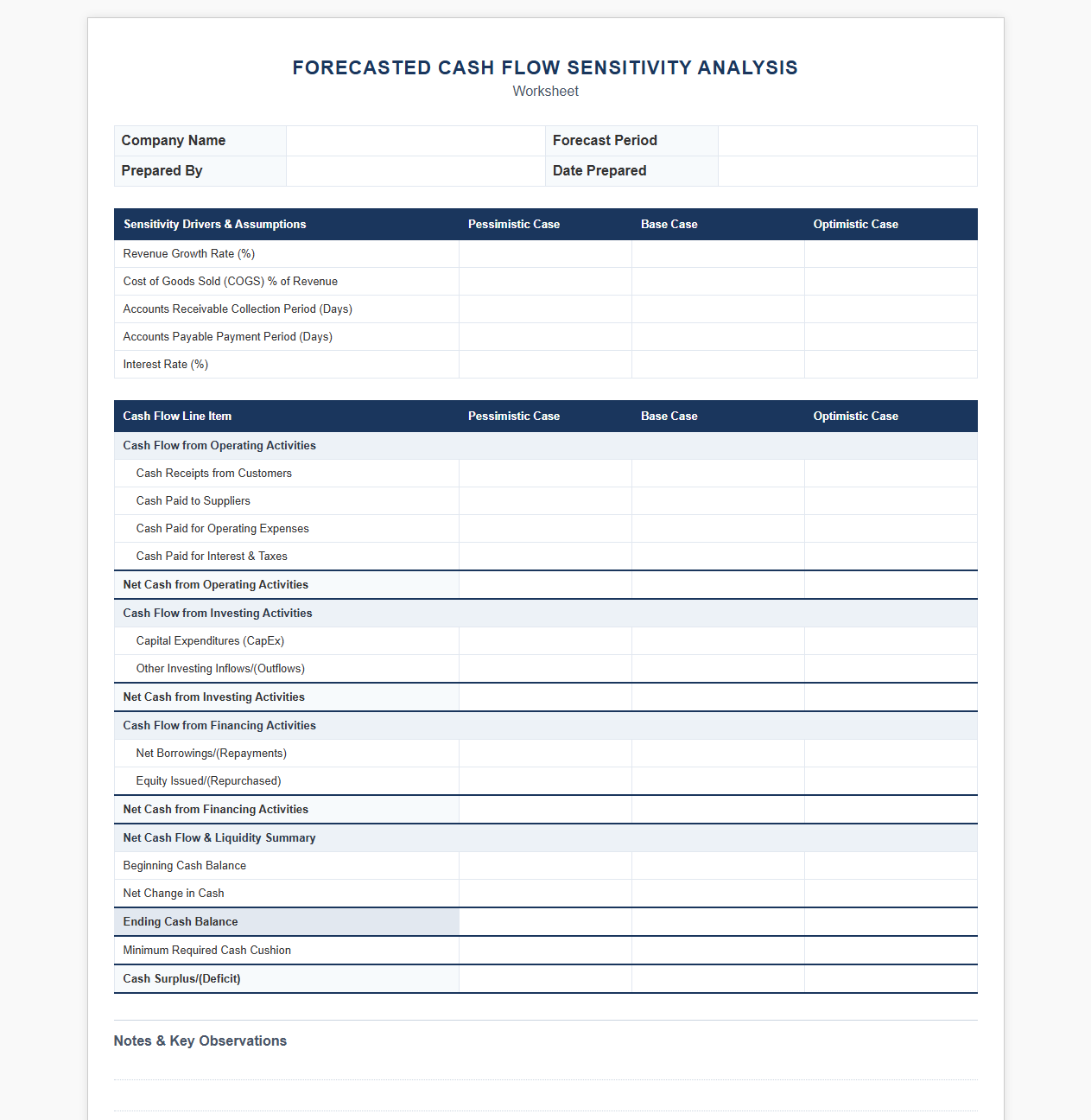

Forecasted Cash Flow Sensitivity Analysis Worksheet

Download: .PDF

Download: .PDF

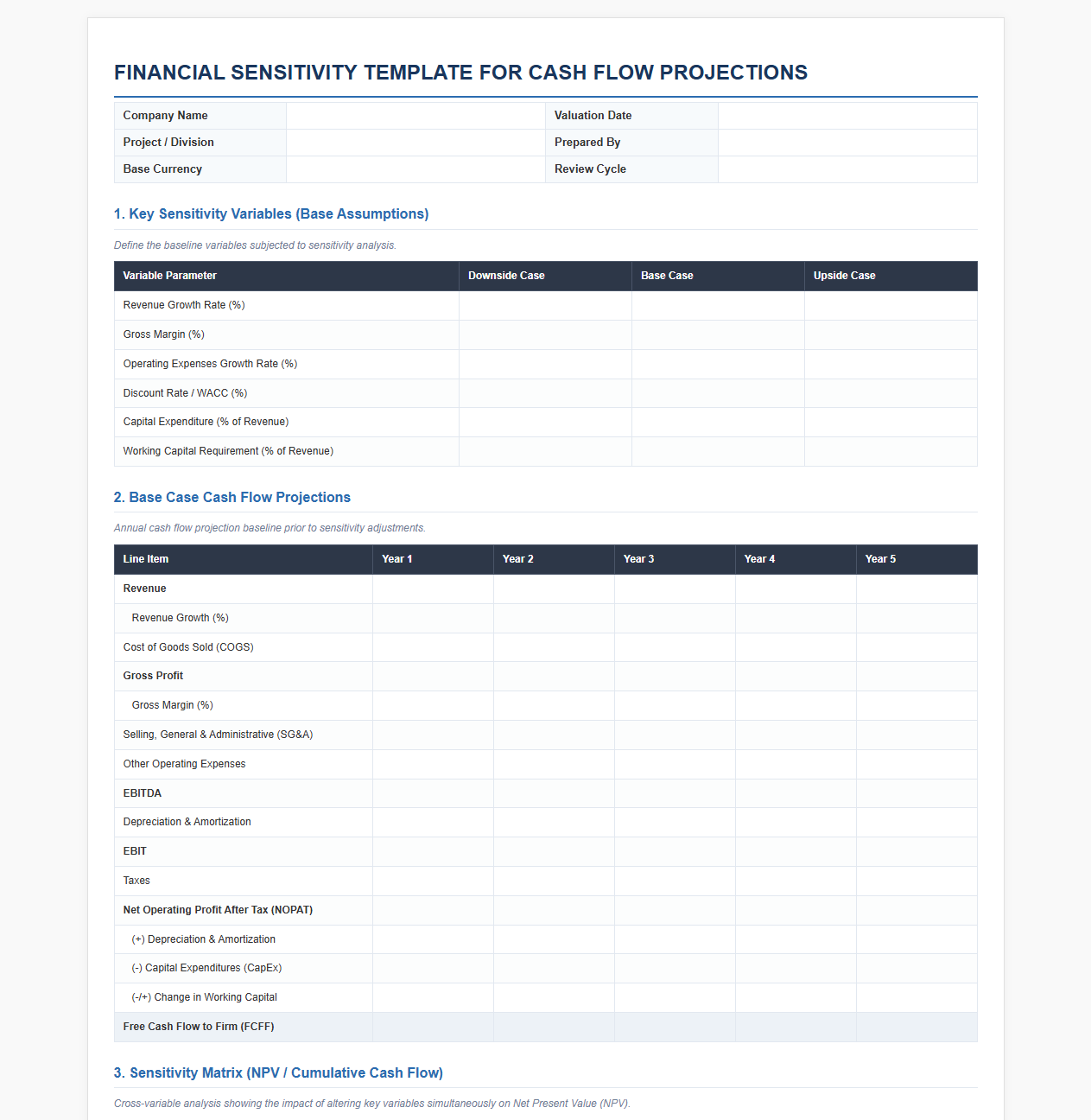

Financial Sensitivity Template for Cash Flow Projections

Download: .PDF

Download: .PDF

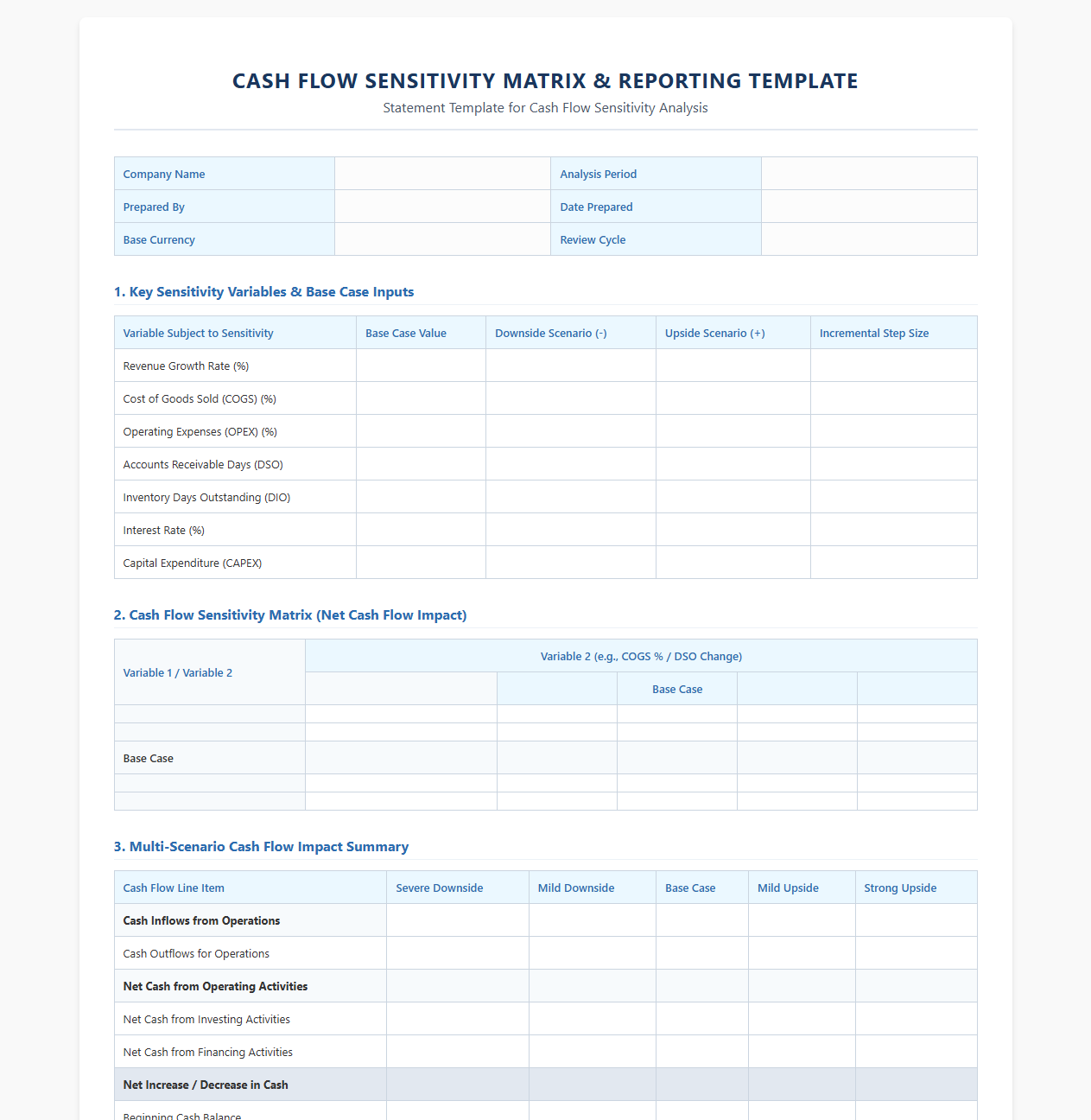

Cash Flow Sensitivity Matrix and Reporting Template

Download: .PDF

Download: .PDF

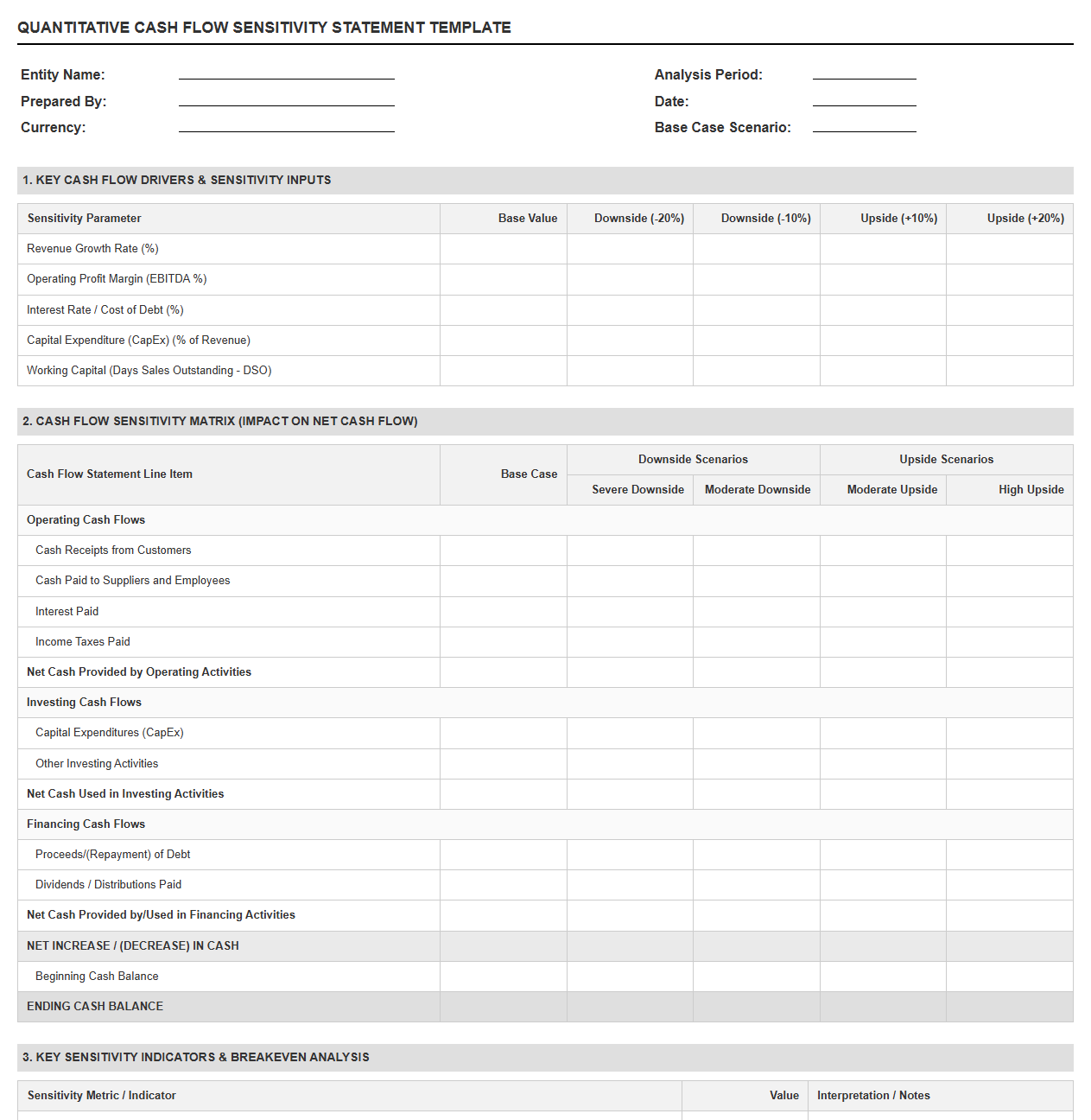

Quantitative Cash Flow Sensitivity Statement Template

Download: .PDF

Download: .PDF

Introduction to Cash Flow Sensitivity in Risk Assessment

In the volatile landscape of modern corporate finance, understanding the dynamics of cash inflows and outflows is paramount. Cash flow sensitivity analysis serves as a foundational pillar in robust financial risk management, allowing organizations to evaluate how changes in underlying operational variables impact overall liquidity. By systematically adjusting key assumptions, treasury departments can quantify the potential variance in cash positions under volatile market conditions.

This analytical framework functions as an indispensable early warning system for impending liquidity crises. Rather than relying on static historical performance, sensitivity modeling projects forward-looking vulnerabilities, highlighting the exact moments when operational disruptions could trigger insolvency. Consequently, management can identify funding gaps and proactively secure revolving credit lines or restructure debt obligations before market pressures limit their options.

Key Variables and Metrics for Sensitivity Modeling

To construct an effective cash flow sensitivity model, analysts must isolate and manipulate the specific operational drivers that exert the greatest influence on liquidity. The following structured variables represent the core inputs required for accurate risk profiling:

- Revenue Growth Rate Variations: Simulating fluctuations in top-line demand directly influences cash collections. The basic formula to determine incremental cash impact is represented as:

\Delta Cash = \Delta Revenue \times (1 - Operating Variable Cost Ratio). - Operating Margin Fluctuations: Changes in raw materials, wages, or overhead costs alter operational efficiency. The adjusted operational cash flow can be modeled using:

OCF = EBIT + Depreciation - Taxes - \Delta NWC. - Interest Rate Shifts: For companies utilizing floating-rate debt instruments, an increase in benchmark rates directly accelerates cash outflows. The sensitivity of interest expense is calculated via:

\Delta Interest = Floating Debt Principal \times \Delta Rate.

Structuring the Cash Flow Sensitivity Matrix Template

A structured sensitivity matrix allows financial managers to visualize the dual-axis impact of changing sales volumes against fluctuating raw material expenses. This grid provides a clear roadmap of profitability and cash sustainability across multiple intersecting operational conditions.

| Sales Volume Change vs. Raw Material Cost Change | Raw Materials +15% | Raw Materials +5% | Raw Materials (Baseline) | Raw Materials -5% |

|---|---|---|---|---|

| Sales Volume -20% | -$250,000 | -$180,000 | -$120,000 | -$80,000 |

| Sales Volume -10% | -$110,000 | -$45,000 | -$10,000 | +$35,000 |

| Sales Volume (Baseline) | +$50,000 | +$115,000 | +$150,000 | +$210,000 |

| Sales Volume +10% | +$180,000 | +$260,000 | +$310,000 | +$380,000 |

Analyzing Multi-Scenario Outcomes

Developing a multi-scenario framework provides clear bounds for corporate planning by establishing realistic optimistic, base, and pessimistic cash pathways. Under the Optimistic Scenario, strong market demand combined with supply chain efficiencies results in robust working capital, keeping the cash balance well above the target safety threshold of $500,000.

The Base Scenario represents the most likely operational pathway, reflecting moderate growth and stable raw material costs. In this state, cash reserves remain secure, comfortably hovering around a steady $250,000 baseline, which allows for scheduled capital expenditures and routine dividend distributions.

Conversely, the Pessimistic Scenario models a severe market contraction paired with rising operational costs. Under these conditions, the corporate cash balance rapidly degrades, crossing the critical liquidity threshold of $50,000 by the end of Q3, signaling an immediate need for emergency financing interventions.

Stress Testing Debt Service Capabilities

A primary objective of sensitivity testing is to verify whether an organization can meet its fixed financial commitments during a downturn. The Debt Service Coverage Ratio (DSCR) measures the cushion a company has to pay its outstanding principal and interest obligations.

"The Borrower shall maintain a Debt Service Coverage Ratio (DSCR) of not less than 1.20x, evaluated on a rolling twelve-month basis at the close of each fiscal quarter."

When operational cash flow falls due to margin compression or declining customer demand, the DSCR drops in tandem. The critical point of failure occurs when the ratio drops below 1.0x, indicating that the business is no longer generating sufficient internal cash to service its debt. Running predictive sensitivity stress tests reveals the exact percentage drop in sales volume that would breach bank covenants, giving management time to negotiate waivers or secure subordinated equity bridges.

Visualizing Breakeven and Liquidity Thresholds

Analytical spreadsheets are highly effective, but visualizing cash trends against fixed operational hurdles translates complex datasets into clear, actionable intelligence for corporate boards.

--- Breakeven Intersection Point ---

The intersection points on such a dashboard illustrate where cumulative inflows fall behind variable and fixed cost lines. By observing the slope of the cash exhaustion line, decision-makers can determine the precise month the business will run out of liquid assets if current market pressures persist without operational adjustments.

Strategic Risk Mitigation and Action Plans

Leveraging the insights gained from sensitivity modeling requires translating numbers into concrete organizational defense strategies. Chief Financial Officers must establish predefined trigger points that automatically initiate cost-containment measures or drawdowns on pre-arranged lines of credit. This disciplined approach eliminates emotional hesitation during high-stress market contractions.

Maintaining balance sheet flexibility remains the most reliable defense against unforeseen operational volatility. By aligning capital expenditure budgets with real-time sensitivity outputs, enterprises can rapidly scale back discretionary cash outflows when indicators shift toward pessimistic thresholds, ensuring long-term corporate viability. Proactive sensitivity modeling is not merely a compliance exercise, but the foundation of resilient corporate survival.

Leave a comment